Important Information

Investors should not base investment decisions on this content alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X HSCEI Components Covered Call Active ETF (the “Fund”) aims to generate income by primarily investing in constituent equity securities in the Hang Seng China Enterprises Index (the “Reference Index” or the “HSCEI”) and selling (i.e. “writing”) call options on the Reference Index to receive payments of money from the purchaser of call options (i.e. “premium”).

- The objective of adopting a covered call strategy is to generate income and reduce potential loss against the downward market. Each time the Fund writes a HSCEI Call Option, the Fund receives a premium. If the value of the securities relating to the Reference Index held by the Fund declines, the premium that the Fund received for writing the HSCEI Call Option may reduce such loss to some extent. However, the downside of adopting a covered call strategy is that the Fund’s opportunity to profit from an increase in the level of the Reference Index is limited to the strike price of the HSCEI Call Options written, plus the premium received.

- The Fund is an ETF which adopts a covered call strategy by (i) investing in constituent equity securities in the Reference Index and the HSCEI ETF and long positions of HSCEI Futures, and (ii) writing call options on the Reference Index. The Fund is one of the first covered call ETFs in Hong Kong. Such novelty makes the Fund riskier than traditional ETFs investing in equity securities.

- The Fund employs an actively managed investment strategy. In addition to seeking to obtain exposure to the constituent equity securities in the Reference Index in substantially the same weightings as these securities have in the Reference Index through investing directly in constituent equity securities of the Reference Index and HSCEI ETF and long positions of HSCEI Futures, the Fund also writes call options on the Reference Index. The Fund may fail to meet its objective as a result of the implementation of investment process which may cause the Fund to underperform as compared to direct investments in the constituent equity securities of the Reference Index.

- The market value of a HSCEI Call Option may be affected by an array of factors including but not limited to supply and demand, interest rates, the current market price of the Reference Index in relation to the strike price of the HSCEI Call Options, the actual or perceived volatility of the Reference Index and the time remaining until the expiration date. The Fund’s ability to utilise HSCEI Call Options successfully will depend on the ability of the Manager to correctly predict future price fluctuations, which cannot be assured and are subject to market behaviour or unexpected events.

- If a HSCEI Call Option expires and if there is a decline in the market value of the Reference Index during the option period, the premiums received by the Fund from writing the HSCEI Call Options may not be sufficient to offset the loss realised.

- The Fund may write HSCEI Call Options over an exchange or in the OTC market. The HSCEI Call Options in the OTC markets may not be as liquid as exchange-listed options. There may be a limited number of counterparties which are willing to enter into HSCEI Call Options as purchasers or the Fund may find the terms of such counterparties to be less favorable than the terms available for listed options. Moreover, the SEHK may suspend the trading of options in volatile markets. If trading is suspended, the Fund may not be able to write HSCEI Call Options at times that may be desirable or advantageous to do so.

- The use of futures contracts involves risks that are potentially greater than the risks of investing directly in securities and other more traditional assets. The risks include but not limited to market risk, volatility risk, leverage risk and negative roll yields and “contango” risk.

- Investing in HSCEI Futures and writing HSCEI Call Options generally involve the posting of margin. Additional funds may need to be posted as margin to meet margin calls based upon daily marking to market of the HSCEI Futures and the HSCEI Call Options. Increases in the amount of margin or similar payments may result in the need for the Fund to liquidate its investments at unfavourable prices in order to meet margin calls. If the Fund is unable to meet its investment objective as a result of margin requirements imposed by the HKFE, the Fund may experience significant losses.

- HSCEI Futures and HSCEI Call Options are registered, cleared and guaranteed by the HKFE Clearing Corporation. In the event of the bankruptcy of the clearing house, the Fund could be exposed to a risk of loss with respect to its assets that are posted as margin.

- The Fund is subject to concentration risk as a result of tracking the performance of a single geographical region or country (Mainland China). The Fund may likely be more volatile than a broad-based fund, such as a global equity fund, as it is more susceptible to fluctuations resulting from adverse conditions in Mainland China. In addition, to the extent that the constituent securities of the Reference Index are concentrated in Hong Kong listed Mainland securities of a particular sector or market, the investments of the Fund may be similarly concentrated. The value of the Fund may be more volatile than that of a fund having a more diverse portfolio of investments. The value of the Fund may be more susceptible to adverse conditions in such particular market/sector.

- The borrower may fail to return the securities in a timely manner or at all. The Fund may as a result suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests. As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund.

- The base currency of the Fund is HKD but the class currencies of the Shares are in HKD, RMB and USD. The Net Asset Value of the Fund and its performance may be affected unfavourably by fluctuations in the exchange rates between these currencies and the base currency and by changes in exchange rate controls.

- Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Share of the Fund and will reduce the capital available for future investment.

- The trading price of the Fund unit (the “Unit”) on the SEHK is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- Global X HSI Components Covered Call Active ETF (the “Fund”) aims to generate income by primarily investing in constituent equity securities in the Hang Seng Index (the “Reference Index” or the “HSI”) and selling (i.e. “writing”) call options on the Reference Index to receive payments of money from the purchaser of call options (i.e. “premium”).

- The objective of adopting a covered call strategy is to generate income and reduce potential loss against the downward market. Each time the Fund writes a HSI Call Option, the Fund receives a premium. If the value of the securities relating to the Reference Index held by the Fund declines, the premium that the Fund received for writing the HSI Call Option may reduce such loss to some extent. However, the downside of adopting a covered call strategy is that the Fund’s opportunity to profit from an increase in the level of the Reference Index is limited to the strike price of the HSI Call Options written, plus the premium received.

- The Fund is an ETF which adopts a covered call strategy by (i) investing in constituent equity securities in the Reference Index and the HSI ETF and long positions of HSI Futures, and (ii) writing call options on the Reference Index. The Fund is one of the first covered call ETFs in Hong Kong. Such novelty makes the Fund riskier than traditional ETFs investing in equity securities.

- The Fund employs an actively managed investment strategy. In addition to seeking to obtain exposure to the constituent equity securities in the Reference Index in substantially the same weightings as these securities have in the Reference Index through investing directly in constituent equity securities of the Reference Index and HSI ETF and long positions of HSI Futures, the Fund also writes call options on the Reference Index. The Fund may fail to meet its objective as a result of the implementation of investment process which may cause the Fund to underperform as compared to direct investments in the constituent equity securities of the Reference Index.

- The market value of a HSI Call Option may be affected by an array of factors including but not limited to supply and demand, interest rates, the current market price of the Reference Index in relation to the strike price of the HSI Call Options, the actual or perceived volatility of the Reference Index and the time remaining until the expiration date. The Fund’s ability to utilise HSI Call Options successfully will depend on the ability of the Manager to correctly predict future price fluctuations, which cannot be assured and are subject to market behaviour or unexpected events.

- If a HSI Call Option expires and if there is a decline in the market value of the Reference Index during the option period, the premiums received by the Fund from writing the HSI Call Options may not be sufficient to offset the loss realised.

- The Fund may write HSI Call Options over an exchange or in the OTC market. The HSI Call Options in the OTC markets may not be as liquid as exchange-listed options. There may be a limited number of counterparties which are willing to enter into HSI Call Options as purchasers or the Fund may find the terms of such counterparties to be less favorable than the terms available for listed options. Moreover, the SEHK may suspend the trading of options in volatile markets. If trading is suspended, the Fund may not be able to write HSI Call Options at times that may be desirable or advantageous to do so.

- The use of futures contracts involves risks that are potentially greater than the risks of investing directly in securities and other more traditional assets. The risks include but not limited to market risk, volatility risk, leverage risk and negative roll yields and “contango” risk.

- Investing in HSI Futures and writing HSI Call Options generally involve the posting of margin. Additional funds may need to be posted as margin to meet margin calls based upon daily marking to market of the HSI Futures and the HSI Call Options. Increases in the amount of margin or similar payments may result in the need for the Fund to liquidate its investments at unfavourable prices in order to meet margin calls. If the Fund is unable to meet its investment objective as a result of margin requirements imposed by the HKFE, the Fund may experience significant losses.

- HSI Futures and HSI Call Options are registered, cleared and guaranteed by the HKFE Clearing Corporation. In the event of the bankruptcy of the clearing house, the Fund could be exposed to a risk of loss with respect to its assets that are posted as margin.

- To the extent that the constituent securities of the Reference Index are concentrated in Hong Kong listed securities of a particular sector or market, the investments of the Fund may be similarly concentrated. The value of the Fund may be more volatile than that of a fund having a more diverse portfolio of investments. The value of the Fund may be more susceptible to adverse conditions in such particular market/sector.

- The borrower may fail to return the securities in a timely manner or at all. The Fund may as a result suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests. As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund.

- The base currency of the Fund is HKD but the class currencies of the Shares are in HKD, RMB and USD. The Net Asset Value of the Fund and its performance may be affected unfavourably by fluctuations in the exchange rates between these currencies and the base currency and by changes in exchange rate controls.

- Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Share of the Fund and will reduce the capital available for future investment.

- The trading price of the Fund unit (the “Unit”) on the SEHK is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- Global X Hang Seng High Dividend Yield ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer specific factors.

- There is no assurance that dividends will be declared and paid in respect of the securities comprising the Hang Seng High Dividend Yield Index (the “Index”). Dividend payment rates in respect of such securities will depend on the performance of the companies or REITs of the constituent securities of the Index as well as factors beyond the control of the Manager including but not limited to, the dividend distribution policy of these companies or REITs.

- Whether or not distributions will be made by the Fund is at the discretion of the Manager taking into account various factors and its own distribution policy. There can be no assurance that the distribution yield of the Fund is the same as that of the Index.

- The Manager may at its discretion pay dividend out of the capital or gross income of the fund. Payment of dividends out of capital to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any distributions involving payment of dividends out of the Fund’s capital may result in an immediate reduction of the Net Asset Value per Unit.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- The investment objective of Global X US Treasury 3-5 Year ETF (the “Fund”) is to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Mirae Asset US Treasury 3-5 Year Index (the “Underlying Index”).

- The Fund is exposed to the Credit/Default risk of issuers of the debt securities that the Fund may invest in; the Credit Rating risk that the credit ratings assigned by rating agencies are subject to limitations and do not guarantee the creditworthiness of the security and/or issuer at all times; the Downgrading risk that the Manager may or may not be able to dispose of the debt securities that are being downgraded; the Interest rate risk that the prices of debt securities rise when interest rates fall, whilst their prices fall when interest rates rise; the Policy risk that the changes in macro-economic policies in the US may have an influence over the US’ capital markets and affect the pricing of the bonds in the Fund’s portfolio, which may in turn adversely affect the return of the Fund; the Sovereign debt risk that the Fund’s investment in US Treasury securities may be exposed to political, social and economic risks that the Fund may suffer significant losses when there is a default of the US Treasury; the valuation risk that the valuation of the Fund’s instruments may involve uncertainties and judgmental determinations. If such valuation turns out to be incorrect, this may affect the Net Asset Value calculation of the Fund.

- The Underlying Index is a new index. The Underlying Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Underlying Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history.

- The Underlying Index is subject to concentration risk as a result of tracking the performance of a single geographical region, namely the US, and is concentrated in debt securities of a single issuer, namely the US Treasury. The Fund’s value may be more volatile than that of a fund having a more diverse portfolio and may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the US market.

- The base currency of the Fund is USD but the trading currency of the Fund is in HKD. The Net Asset Value of the Fund and its performance may be affected unfavourably by fluctuations in the exchange rates between these currencies and the base currency and by changes in exchange rate controls.

- The borrower may fail to return the securities lent out in a timely manner or at all. The Fund may as a result suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests. As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the collateral, adverse market movements in the collateral value or change of value of securities lent. This may cause significant losses to the Fund.

- The trading price of the Units on the SEHK is driven by market factors such as the demand and supply of the Units. Therefore, the Units may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- Payments of distributions out of capital and/or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions involving payment of distributions out of capital or effectively out of capital of the Fund may result in an immediate reduction in the Net Asset Value per Unit of the Fund and will reduce the capital available for future investment.

- Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X Bloomberg MSCI Asia Ex Japan Green Bond ETF (the “Fund”) aims to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Bloomberg MSCI Asia ex Japan USD Green Bond Index (the “Underlying Index”).

- The Fund’s investments maybe concentrated in Green Bonds. The value of the Fund may be more volatile than that of a fund having a more diverse portfolio of investments. The use of the GBP-based selection criteria in the construction of the Index and the adoption of the Green Bond investment strategy of the Sub-Fund may result in the Sub-Fund foregoing opportunities to buy certain securities when it might otherwise be advantageous to do so, and/or selling securities when it might be disadvantageous to do so. This may adversely affect the Sub-Fund’s investment performance and, as such, the Sub-Fund may perform differently compared to similar funds that do not use such criteria.

- There is no assurance that dividends will be declared and paid in respect of the securities comprising the Underlying Index.

- Whether or not distributions will be made by the Fund is at the discretion of the Manager, taking into account various factors and its own distribution policy. There can be no assurance that the distribution yield of the Fund is the same as that of the Underlying Index.

- Dividends may be paid from capital or effectively out of capital of the Fund, which may amount to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment and result in an immediate reduction in the Net Asset Value per Unit of the Fund.

- The Underlying Index is a new index. It has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Underlying Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history.

- The Fund invests in emerging markets which may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risk, currency risks/control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk and the likelihood of a high degree of volatility.

- The trading price of the Fund unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

Monthly Commentary

Income ETFs – Nov 2024

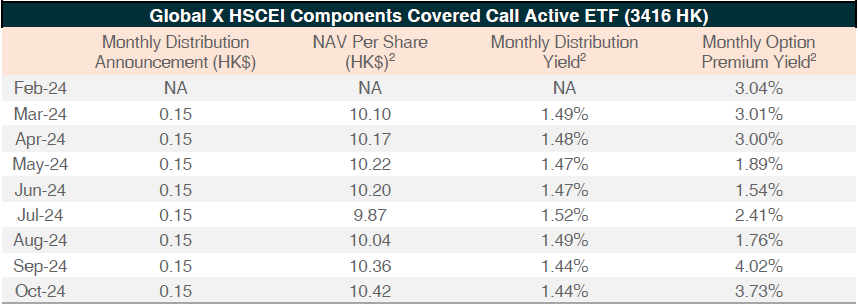

Global X HSCEI Components Covered Call Active ETF

(3416 HK)

- Monthly Distribution Paid in Oct: The ETF distributed HK$0.15 per share on 7 October.

- Monthly Distribution Announcement in Oct: The ETF announced monthly distribution of HK$0.15 per share on 16 October, to be distributed on 6 November.

- Premium Earned in Oct: Premium earned by selling index call options for the HSCEI remained high at 3.73% in Oct, as bolstered by the increased market volatility on the back of strong policy stimulus since the end of Sep.

- Total Return: The total return at the end of Oct (assuming buying this ETF on its launch date of 29 February 2024) would be 19.4% (including 13.0% distribution return and 6.4% capital appreciation), as of 31 Oct.1

Monthly Option Premium and Distribution History1

Global X HSI Components Covered Call Active ETF

(3419 HK)

Update

- Monthly Distribution Paid in Oct: The ETF distributed HK$0.12 per share on 7 October.

- Monthly Distribution Announcement in Oct: The ETF announced monthly distribution of HK$0.12 per share on 16 October, to be distributed on 6 November.

- Premium Earned in Oct: Premium earned by selling index call options for the HSI remained high at 3.34% in Oct, as bolstered by the increased market volatility on the back of strong policy stimulus since the end of Sep.

- Total Return: The total return at the end of Oct (assuming buying this ETF on its launch date of 29 February 2024) would be 14.9% (including 10.3% distribution return and 4.6% capital appreciation), as of 31 Oct.1

Monthly Option Premium and Distribution History1

Global X Hang Seng High Dividend Yield ETF

(3110 HK)

Market Update

Hang Seng High Dividend Yield Index recorded -1% return in October. As market enter into a volatile period amid a series of volatile political and economic events, we believe high dividend strategy should remain attractive thanks to solid dividend yields and lower volatility. PBOC’s recently announced Rmb300bn relending program should drive an increase in corporate share repurchase and enhance overall shareholder returns. In addition, there are potential incremental fund flows from household savings currently deposited in the bank to seek higher yield, as savings rates are falling. For financial sector, PBOC committed to lower deposit rates to keep Banks’ net interest margins stable, and Brokers could also benefit from improved capital market activities as high-quality M&A are encouraged by regulators.

Stock Comments

CNOOC recorded 6% loss in October, a detractor to the ETF. The company reported in-line Q3 results. Q3 Net profit was Rmb37bn, +9% YoY and -8% QoQ due to sequentially lower oil prices and production dampened by typhoons. Despite typhoon impacts, CNOOC achieved above-guidance production growth of c.7% yoy in 3Q, higher than its full-year guidance of 3-6% yoy. Company maintains 2024 production guidance and aims to complete the upper-end of guidance.

China Telecom recorded 0.5% loss in October, roughly in line with the ETF. China Telecom reported in-line 3Q24 results with service revenue of Rmb117bn (+2.5% YoY), and EBITDA of Rmb34.2bn (+6% YoY), both outgrowing peers. China Telecom is on track to achieve high-single-digit percentage full year earnings growth guidance. For FY2024, company maintains unchanged guidance of net profit growth higher than revenue growth, with dividend payout reaching 75%+ of net profit within 3 years from 2024.

Preview

Hang Seng High Dividend Yield Index is well positioned to benefit from increasing allocation from global investors amid global market volatility, and the potential dividend tax removal for southbound investors. Notably, this Index consists of over 55%3 of its constituents in State Owned Enterprises. Supportive policies across consumption, property, and technology sectors, as well as the ongoing capital market reforms are key drivers for market rebound. The concept of the Valuation System with Chinese Characteristics (“VCC”) is back in the spotlight again in light of recent developments. The primary objective of VCC is to enhance the quality and investment value of listed companies, especially SOEs. By investing in the Hang Seng High Dividend Yield Index, investors can gain exposure to high dividend-paying and low-volatility companies while also benefiting from the accelerated implementation of VCC

Global X US Treasury 3-5 Year ETF

(3450 HK)

Market Update

The 3-5 year US Treasury yield rose for 4 consecutive weeks on the month of October, following the release of a series of stronger-than-expected domestic data. Non-farm payrolls rose 254k in September, far exceeding the consensus expectation of 150k. Inflation and consumption also showed upside surprises: CPI rose 0.3% (consensus:0.2%) and retail sales rose 0.4% (consensus:0.3%). By the end of the month, UST 3-5y yields rose by 30 to 35 bps compared to September levels. This rise in yields dragged the performance of the Mirae Asset US Treasury 3-5 Year Index, which recorded a loss of 1.81%.

Preview

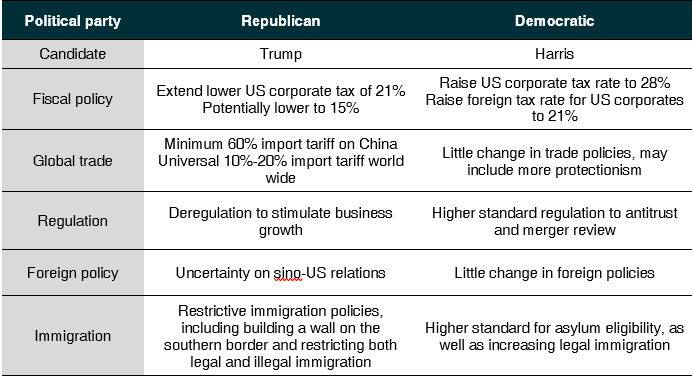

Looking ahead, the US election will be one of the key drivers of US treasury yields for the coming weeks. While the divided government is expected to have limited impact on bond yield, a blue or red sweep would have diverged implications for Treasury market. Below table summarises two candidates’ policy highlights. Trump’s victory may encourage a higher UST yield and stronger USD, driven by lower corporate tax, broad-based tariff and tougher immigration policies. On the other hand, if Harris wins the presidency, since her agenda proposed a potential tax rate hike, market would expect Fed to continue easing.

With Treasury yield continued higher and the post FOMC bearish steepening extended further, the bond market has shifted towards a red sweep. If Trump win the presidency this time, the additional selloff would be limited. Under other scenarios like divided government and democratic sweep, we would expect some room for yield to decline after the election, especially for the belly which underperformed significantly over the last few weeks.

Global X Bloomberg MSCI Asia Ex Japan Green Bond ETF

(3059 HK)

Market Update

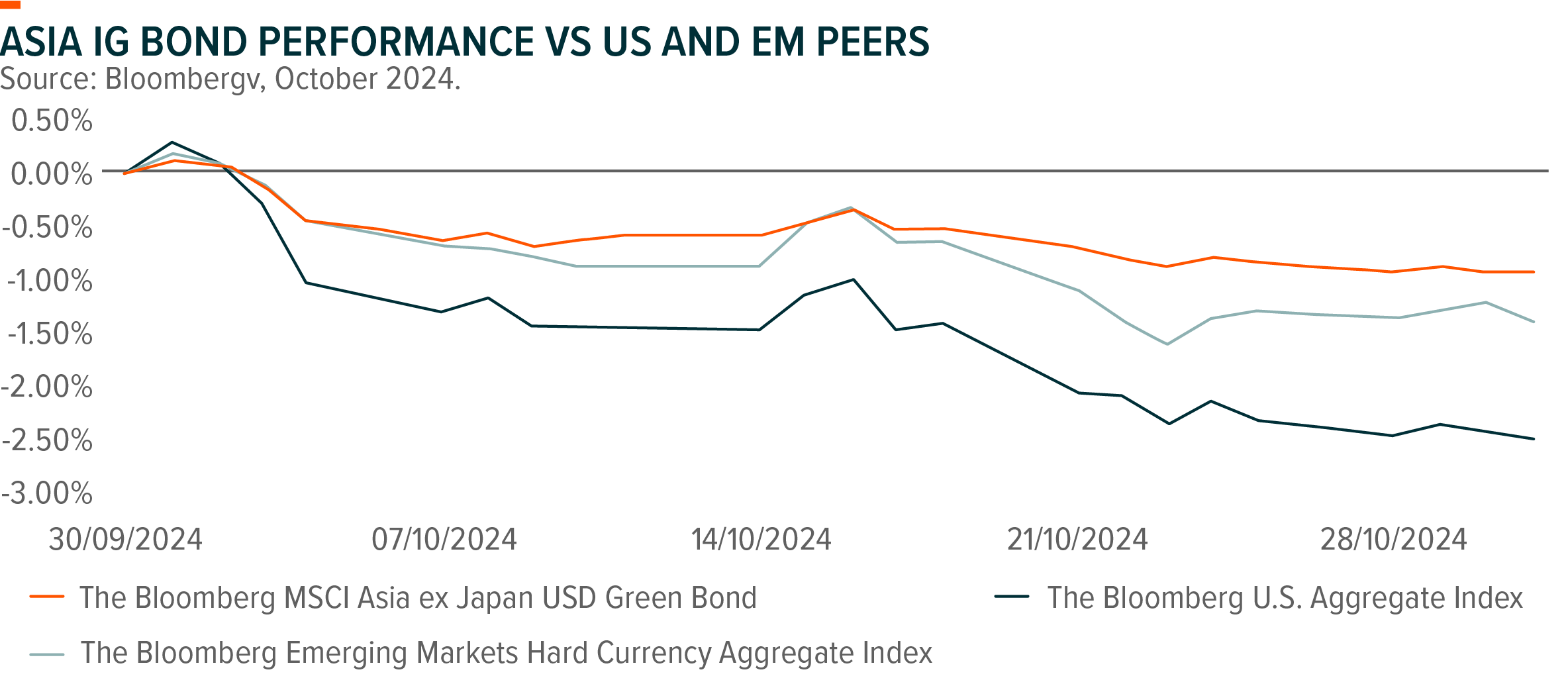

Global X Bloomberg MSCI Asia Ex Japan Green Bond ETF recorded a loss of 0.91% in October, outperformed it’s US IG and EM IG peers against the backdrop of post FOMC bearish steepening. Low beta countries/regions exhibited better returns, with Singapore 0.36%, China -0.23% and South Korea -0.95%.

Preview

Looking ahead, the US election will be one of the key drivers of bond performance for the coming weeks. As the presidential polls remain uncertain in key swing states, Global X Bloomberg MSCI Asia Ex Japan Green Bond ETF is well positioned for funds seeking lower portfolio beta and defensiveness. Asia IG bonds have a history of being less volatile than EM IG peers; they have also tended to offer more downside protection when US IG credit has generated negative annual total return.4 Notably, the index consists of 24.79% Korea bonds, 20.72% Hong Kong bonds and 34.66% China bonds, which show less correlation with US IG and IG in other regions.

Moreover, no matter which party wins the election, the new government will face significant fiscal challenges. The ongoing wide budget deficit would result in higher term premium, limiting the performance of long duration bonds. As of Oct 2024, Global X Bloomberg MSCI Asia Ex Japan Green Bond ETF has the duration of 3.26, providing clients with exposure to mid-term duration bonds.