Important Information

Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- The investment objective of Global X China Semiconductor ETF’s (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the FactSet China Semiconductor Index.

- The Fund is exposed to concentration risk by tracking a single region or country.

- The Index constituents may be concentrated in a specific industry or sector, which may potentially more volatile than a fund with a diversified portfolio.

- Semiconductor industry may be affected by particular economic or market events, such as domestic and international competition pressures, rapid obsolescence of products, the economic performance of the customers of semiconductor companies and capital equipment expenditures.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy may invest up to 50% of its net asset value in financial derivative instruments (“FDIs”), which may expose the Fund to counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. The Fund may suffer losses from its usage of FDIs.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

Why OpenClaw is a Prime Catalyst for China Semiconductor?

OpenClaw, a leading AI agent, has recently gained significant popularity across China. While the global proliferation of AI agents is a major technological shift, it holds particular significance for Global X China Semiconductor ETF (3191).

The reason lies in how AI agents differ from existing chatbots. While chatbots are passive, AI agents are constantly thinking, planning, and interacting with other software, which requires a vast amount of computing power. In the era of AI agents, the number of tokens a single person uses daily is expected to skyrocket by at least 10 to 20 times compared to the chatbot era.

This represents an even greater opportunity for the China semiconductor industry specifically for two key reasons:

- The Cost-Effectiveness of Chinese LLMs

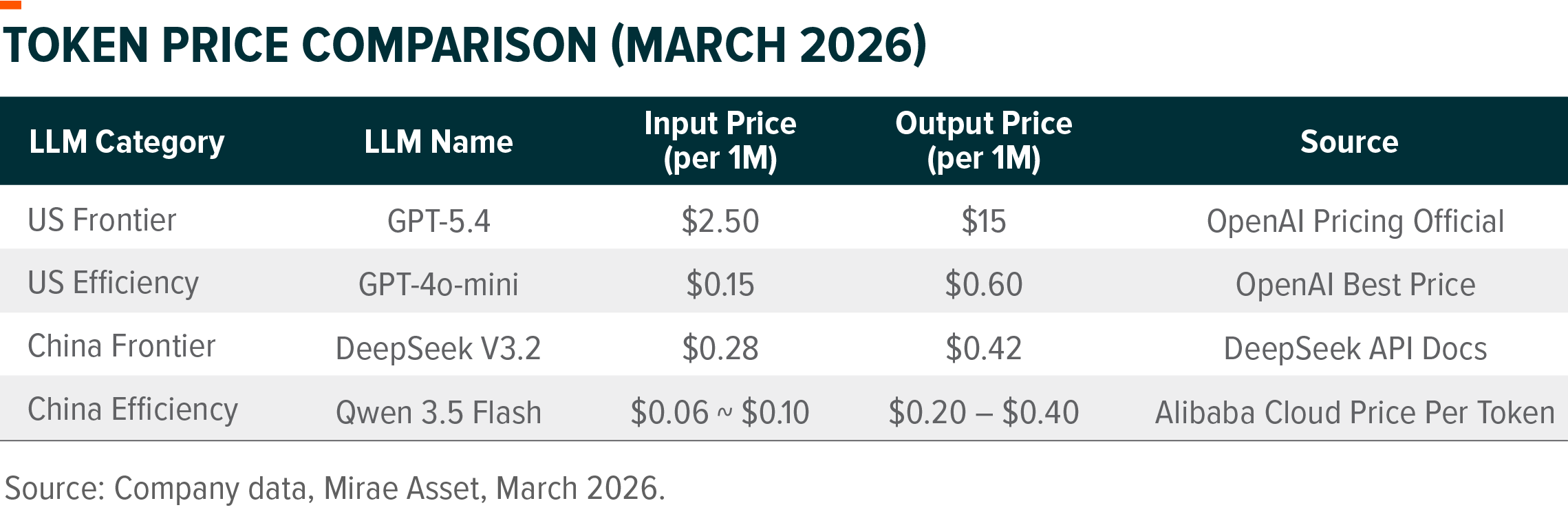

In the era of AI agents, the price of tokens has become a critical economic factor. Chinese Large Language Models (LLMs) are currently highly affordable, positioning them as the preferred choice for powering these agents.

Previously, users prioritized performance over price, because typical consumer usage rarely exceeded one million tokens per month. To put this in perspective, one million tokens are sufficient to draft approximately 100 emails daily. At this volume, even using premium models like OpenAI cost only a few dollars monthly—a manageable expense for most users.

However, the shift to AI agents has fundamentally changed this dynamic. These agents consume at least 10 to 20 times more tokens than standard chatbot interactions. In this high-volume environment, users and developers must prioritize cost-effectiveness.

Chinese models currently offer a distinct competitive advantage in this area; for instance, the token price of leading Chinese LLMs like DeepSeek or Qwen is roughly 10% of the cost of comparable American models. As these cost-efficient Chinese models gain wider global adoption, the Chinese semiconductor industry is receiving a significant and sustained boost in demand.

The Shift Toward AI Inference chip

AI agents primarily drive demand for “inference” chips rather than “training” hardware. While investors often group all kinds of AI chips together, the processes of AI training and AI inference differ significantly in their technical requirements.

During the AI training stage, hundreds of billions of parameters must be constantly modified. This is an exhaustive, repetitive process of “matching values” until a model achieves accuracy, requiring immense computational power and high-end hardware.

AI Inference, on the other hand, is the act of inputting data into a model that has already completed its training to generate results. Inference does not require the same level of raw brute-force computing as training.

If the AI agent craze were driven by “AI training” semiconductors, Nvidia would likely capture the lion’s share of the benefits, regardless of how well China’s LLMs performed. However, the economic story is different for AI inference semiconductors.

After years of painstaking effort, China has achieved strong domestic competitiveness in this specific field. While this once seemed an impossible goal, persistent dedication has allowed the Chinese semiconductor industry to reach a stable, mass-production phase for 7-nanometer (nm) process technology. Had China failed to master the 7nm node, it would have been fundamentally unequipped to seize the massive hardware opportunities presented by the current AI agent era.

In conclusion, the recent and rapid proliferation of AI agents in China, supported by a growing ecosystem of domestic LLMs, is emerging as a powerful engine for China semiconductor industry.

Industry analysts have consistently forecasted dramatic growth for China’s AI chip sector in years to come. Frost & Sullivan indicate that AI chip production in China are expected to grow at a compound annual rate of 32% from 2025 to 2029.

However, with the recent surge of AI agents, these growth figures may prove conservative.

The China semiconductor industry will likely remain one of the most remarkable growth area globally for the foreseeable future.

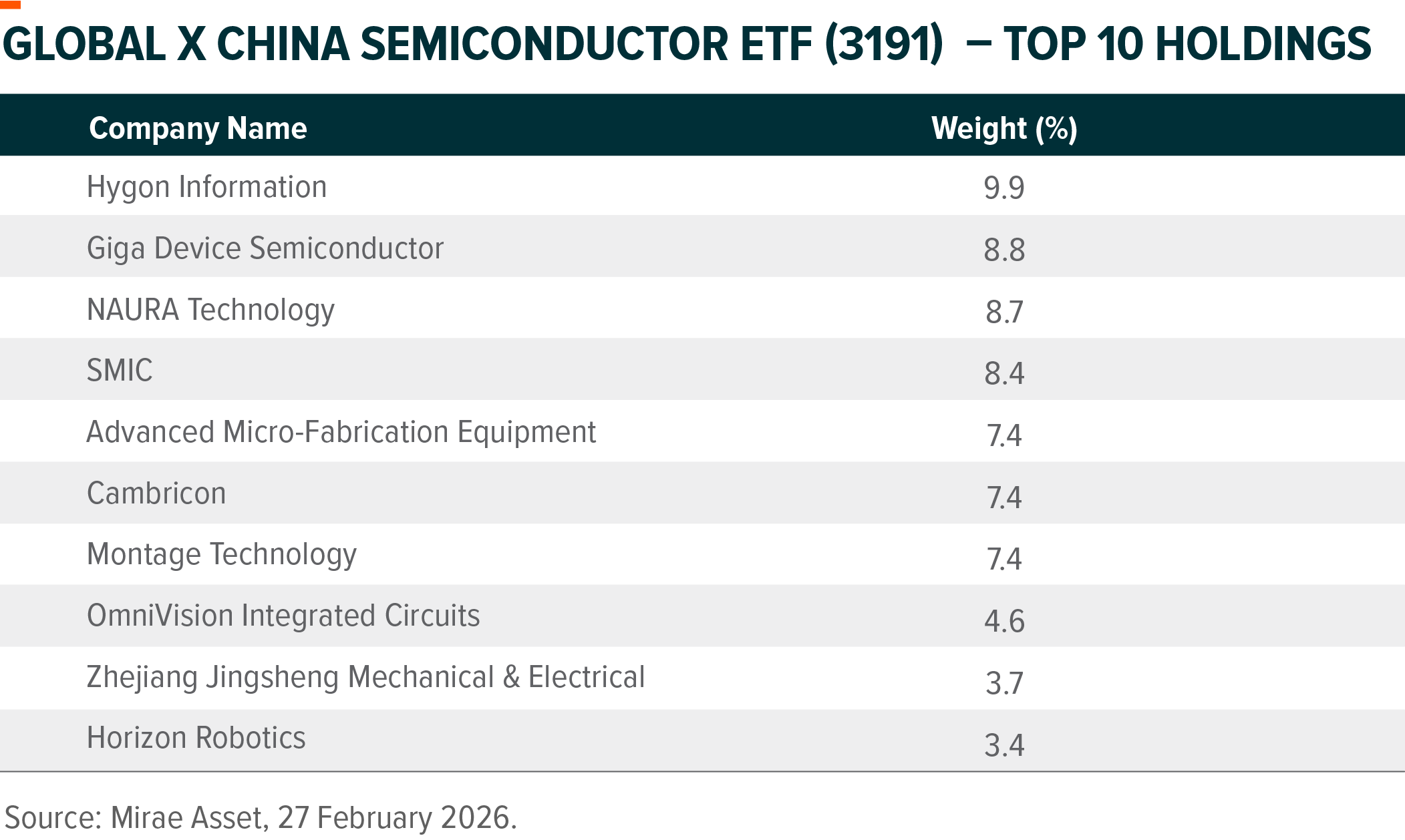

Key ETF Constituents Capitalizing on China’s AI demand Boom

The proliferation of AI agents has directly benefited several key constituents of the Global X China Semiconductor ETF (3191).

SMIC

- As China’s leading chip foundry, SMIC has successfully established mass production of 7nm AI chips.

- Faced with a massive backlog of orders, it is working to double its 7nm capacity by the end of 2026, from the current 20k per month.

Hygon

- Its x86-based architecture provides high compatibility for banking and government infrastructure, securing its role as a leading domestic supplier to replace foreign chips for SOE and governments.

- Hygon officially projected a 63~75% YoY increase for the first quarter of 2026.

Gigadevice

- Its full-year 2025 revenue reached 6.5 billion yuan, a staggering 453% year-on-year increase driven by soaring demand for its AI inference chips.

- Now a dominant force in domestic AI chips alongside Huawei, Cambricon announced its plan to triple its AI chip output in 2026.

Cambricon

- Its full-year 2025 revenue reached 6.5 billion yuan, a staggering 453% year-on-year increase driven by soaring demand for its AI inference chips.

- Now a dominant force in domestic AI chips alongside Huawei, Cambricon plans to triple its output in 2026.

Montage

- Montage is the world’s largest supplier of memory interconnect chips, commanding approximately 36.8% of the global market share by revenue in 2024.

- Montage specializes in “middleware” chips that accelerate data flow between processors and memory, a critical bottleneck in AI training and inference.

For further information on Global X China Semiconductor ETF (3191), please visit our website.