Important Information

Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

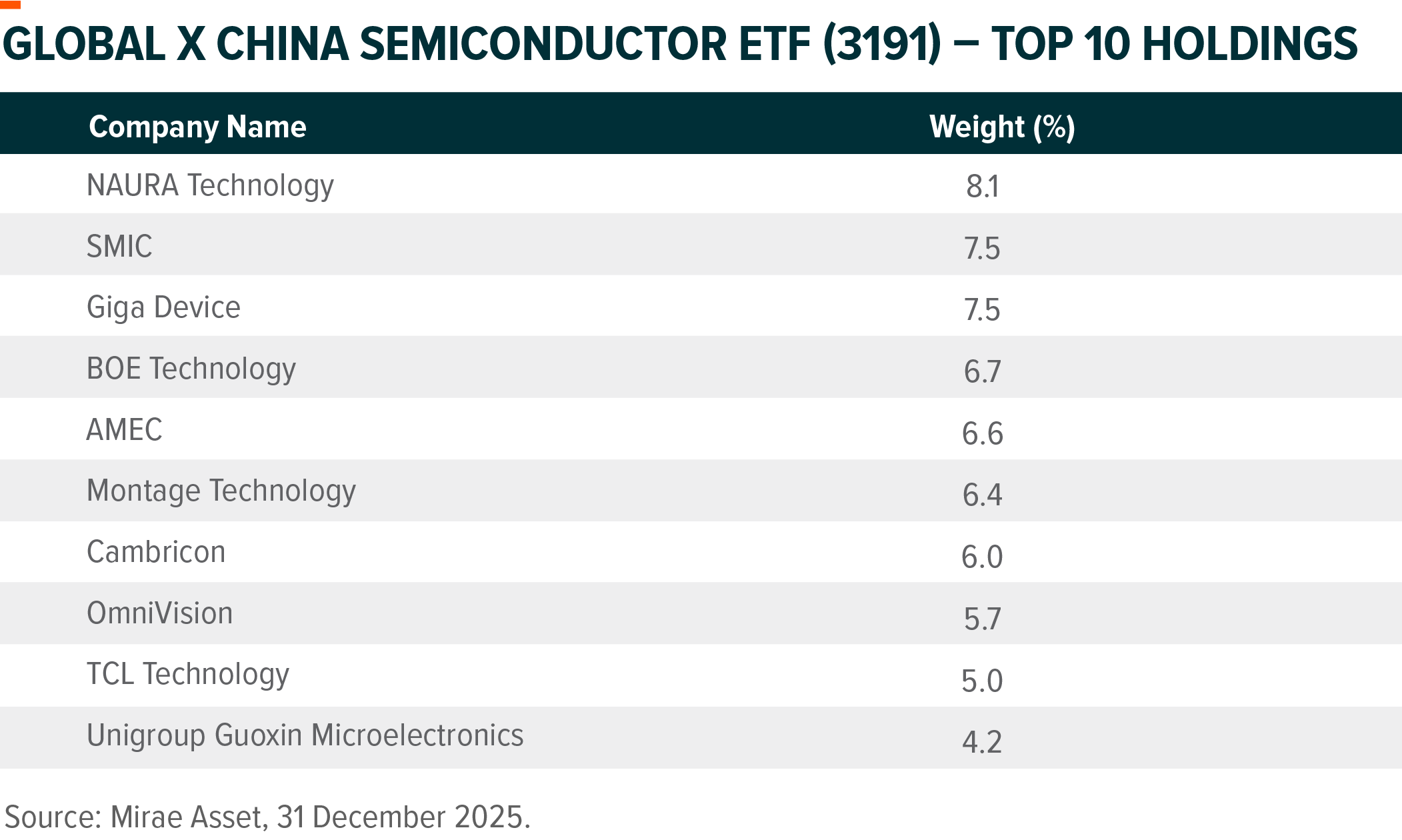

- The investment objective of Global X China Semiconductor ETF’s (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the FactSet China Semiconductor Index.

- The Fund is exposed to concentration risk by tracking a single region or country.

- The Index constituents may be concentrated in a specific industry or sector, which may potentially more volatile than a fund with a diversified portfolio.

- Semiconductor industry may be affected by particular economic or market events, such as domestic and international competition pressures, rapid obsolescence of products, the economic performance of the customers of semiconductor companies and capital equipment expenditures.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy may invest up to 50% of its net asset value in financial derivative instruments (“FDIs”), which may expose the Fund to counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. The Fund may suffer losses from its usage of FDIs.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

Why is the success of Huawei Ascend 950 important to the GX China semiconductor ETF (3191)?

With the daily influx of news related to Chinese semiconductors, it’s difficult to discern what is key issue. In that case, it’s worth paying attention to Huawei’s “Ascend 950” project, scheduled for release in 2026.

The success of Huawei’s new AI chip, the Ascend 950, is crucial. If successful, it will open up a huge market for Chinese semiconductor companies.

The Significance of the Ascend 950

The reason China semiconductor industry is betting on the Ascend 950 is clear.

Unlike “AI training,” which requires extreme computational performance, “AI inference,” the actual service implementation stage, can achieve outstanding performance even with a 7nm process, not a 3nm process.

AI training and AI inference are fundamentally different. AI training requires high-precision computational power, as it involves constantly modifying hundreds of billions of parameters until the right answer is found. AI Inference, on the other hand, involves inputting data and deriving results from an existing AI model, and does not require extreme computational power. This means that Huawei’s (or Cambricon’s) 7nm chip is fully capable of entering the AI inference chip market.

From a commercial perspective, AI inference chips are even more important, as the AI chip market leadership is likely to shift from AI training chips to AI inference chips. While AI training chips accounted for the majority of the AI chip market until 2025, this is expected to completely shift by 2030, with inference chips expected to account for nearly 80% of global AI chip sales.

Furthermore, the Ascend 950’s economic advantages are clear. Let’s look at its price-to-performance ratio. The NVIDIA H100 is approximately 1.3 times more powerful than the Ascend 950, but its price is estimated to be 3-5 times higher than the Huawei chip. For enterprise customers, the Ascend 950 is attractive when considering its “data throughput” relative to its budget.

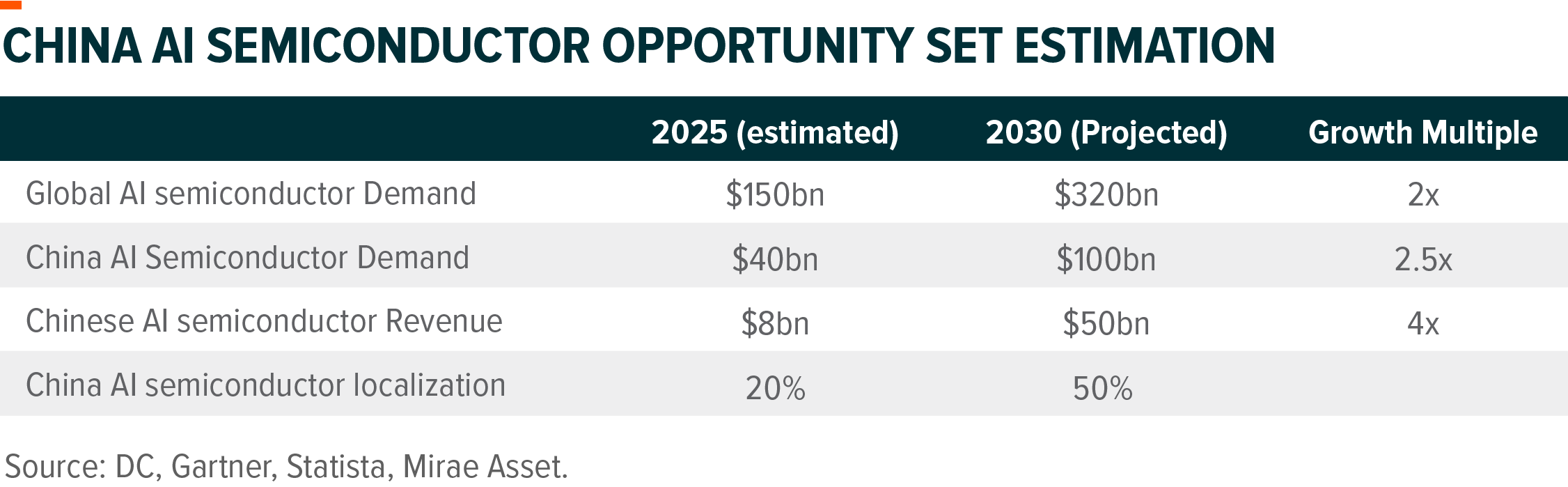

If Ascend 950 is successful, the market size available to Chinese semiconductor companies will expand significantly. China’s domestic demand for AI semiconductors is expected to expand from approximately $40 billion in 2025 to approximately $100 billion in 2030. In 2025, Chinese companies held a 20% market share in local market and generated $8 billion in revenue. If Chinese companies secure a 50% domestic market share by 2030, their revenue is projected to increase 6 times from $8 billion in 2025 to $50 billion in 2030.

Therefore, the success of the Ascend 950 will provide a solid revenue base for the entire Chinese semiconductor supply chain and will also benefit the constituents of Global X China Semiconductor ETF.

Four Challenges for the Huawei Ascend 950

1) Foundry Segment

Unable to import EUV lithography equipment due to US sanctions, China is taking on the extreme challenge of utilizing its predecessor, deep ultraviolet (DUV) lithography. Currently, SMIC is the only company in the world attempting to achieve 5nm-level processing using only DUV equipment. The core of this strategy is multi-patterning, a process that uses DUV lithography equipment to overlap circuits four or more times. This increases the number of process steps by more than three times compared to using EUV equipment, inevitably leading to lower yields.

SMIC is circumventing this issue with a design-process optimization strategy. Huawei’s design team intentionally adjusts chip designs to account for the foundry’s lower process precision. This increases the physical size of the chip somewhat, but ensures a meaningful yield.

2) HBM segment

This aims to achieve self-sufficiency in High Bandwidth Memory (HBM), the import of which is banned due to US sanctions. Huawei is pursuing the establishment of a system to procure HBM3 from domestic companies such as Changxin (CXMT) and Fujian Jinhua (JHICC) for mass production of the Ascend 950.

China’s HBM technology is expected to enter the fourth-generation (HBM3) mass production stage by 2026. A technological gap exists compared to Korean companies that have already entered sixth-generation (HBM4) mass production.

However, HBM3 alone will be sufficient for the development of AI inference chips. CXMT, a leader in China’s DRAM industry, recently announced that it has increased the yield of HBM3 to approximately 50%.

3) Packaging segment

The final hurdle for Ascend 950 production is securing advanced packaging technology, namely CoWoS (Chip on Wafer on Substrate), which combines the GPU and HBM. SiCarrier and Tungfu Micro (TFME) are working together to address this challenge. SiCarrier, a subsidiary of Huawei, developed the interposer exposure and etching solution, a key component of packaging. Tungfu, China’s largest OSAT company, is responsible for final manufacturing based on this solution.

4) Equipment segment

The growth of equipment suppliers such as NAURA, AMEC, and Hwatsing is also a key driving force. NAURA’s etching and deposition equipment has become an essential component of China’s semiconductor production lines.

Building a Self-Reliant Ecosystem by 2026

The successful launch of the Huawei Ascend 950 in 2026 will be more than just a new product announcement. It symbolizes the establishment of China’s high-end semiconductor supply chain, spanning SMIC (manufacturing), CXMT (memory), Tongfu (packaging), and NAURA, AMEC (equipment). This ecosystem will not only facilitate the shared growth of companies within the Huawei alliance but also serve as a catalyst for all chip design companies like Cambricon.