Important Information

Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- The investment objective of Global X HSCEI Covered Call Active ETF (the “Funds”) is to generate income by primarily investing in constituent equity securities in the Hang Seng China Enterprises Index (the “Reference Index”) and selling (i.e. “writing”) call options on the Reference Indexes respectively to receive payments of money from the purchaser of call options (i.e. “premium”).

- If the value of the securities relating to the Reference Index held by the Fund declines, the premium that the Fund received for writing the Reference Index Call Option may reduce such loss to some extent. However, the downside of adopting a covered call strategy is that the Fund’s opportunity to profit from an increase in the level of the Reference Index is limited to the strike price of the Reference Index Call Options written, plus the premium received.

- The market value of an Reference Index Call Option may be affected by factors including supply and demand, interest rates. The Fund’s ability to utilise Reference Index Call Options successfully will depend on the ability of the Manager to correctly predict future price fluctuations.If an Reference Index Call Option expires and if there is a decline in the market value of the Reference Index during the option period, the premiums received by the Fund from writing the Reference Index Call Options may not be sufficient to offset the loss realised.

- The Reference Index Call Options in the OTC markets may not be as liquid as exchange-listed options. The Fund may find the terms of counterparties in the OTC markets to be less favorable than the terms available for listed options. Moreover, the SEHK may suspend the trading of options in volatile markets which may casue the Fund unable to write Reference Index Call Options at times

- The use of futures contracts involves market risk, volatility risk, leverage risk and negative roll yields and “contango” risk.

- Investing in Reference Index Futures and writing Reference Index Call Options generally involve the posting of margin. If the Fund is unable to meet its investment objective as a result of margin requirements imposed by the HKFE, the Fund may experience significant losses.

- The Fund employs an actively managed investment strategy. The Fund may fail to meet its objective as a result of the implementation of investment process which may cause the Fund to underperform as compared to direct investments in the constituent equity securities of the Reference Index.

- The Fund is exposed to concentration risk by tracking a specific regions or countries.

- To the extent that the constituent securities of Reference Index are concentrated in securities of a particular sector or market, the investments of it may be similarly concentrated.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X HSI Covered Call Active ETF (the “Funds”) is to generate income by primarily investing in constituent equity securities in the Hang Seng Index (the “Reference Index”) and selling (i.e. “writing”) call options on the Reference Indexes respectively to receive payments of money from the purchaser of call options (i.e. “premium”).

- If the value of the securities relating to the Reference Index held by the Fund declines, the premium that the Fund received for writing the Reference Index Call Option may reduce such loss to some extent. However, the downside of adopting a covered call strategy is that the Fund’s opportunity to profit from an increase in the level of the Reference Index is limited to the strike price of the Reference Index Call Options written, plus the premium received.

- The market value of an Reference Index Call Option may be affected by factors including supply and demand, interest rates. The Fund’s ability to utilise Reference Index Call Options successfully will depend on the ability of the Manager to correctly predict future price fluctuations.If an Reference Index Call Option expires and if there is a decline in the market value of the Reference Index during the option period, the premiums received by the Fund from writing the Reference Index Call Options may not be sufficient to offset the loss realised.

- The Reference Index Call Options in the OTC markets may not be as liquid as exchange-listed options. The Fund may find the terms of counterparties in the OTC markets to be less favorable than the terms available for listed options. Moreover, the SEHK may suspend the trading of options in volatile markets which may casue the Fund unable to write Reference Index Call Options at times

- The use of futures contracts involves market risk, volatility risk, leverage risk and negative roll yields and “contango” risk.

- Investing in Reference Index Futures and writing Reference Index Call Options generally involve the posting of margin. If the Fund is unable to meet its investment objective as a result of margin requirements imposed by the HKFE, the Fund may experience significant losses.

- The Fund employs an actively managed investment strategy. The Fund may fail to meet its objective as a result of the implementation of investment process which may cause the Fund to underperform as compared to direct investments in the constituent equity securities of the Reference Index.

- To the extent that the constituent securities of Reference Index are concentrated in securities of a particular sector or market, the investments of it may be similarly concentrated.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X Hang Seng TECH Covered Call Active ETF (the “Funds”) is to generate income by primarily investing in constituent equity securities in the Hang Seng TECH Index (the “Reference Index”) and selling (i.e. “writing”) call options on the Reference Indexes respectively to receive payments of money from the purchaser of call options (i.e. “premium”).

- If the value of the securities relating to the Reference Index held by the Fund declines, the premium that the Fund received for writing the Reference Index Call Option may reduce such loss to some extent. However, the downside of adopting a covered call strategy is that the Fund’s opportunity to profit from an increase in the level of the Reference Index is limited to the strike price of the Reference Index Call Options written, plus the premium received.

- The market value of an Reference Index Call Option may be affected by factors including supply and demand, interest rates. The Fund’s ability to utilise Reference Index Call Options successfully will depend on the ability of the Manager to correctly predict future price fluctuations.If an Reference Index Call Option expires and if there is a decline in the market value of the Reference Index during the option period, the premiums received by the Fund from writing the Reference Index Call Options may not be sufficient to offset the loss realised.

- The Reference Index Call Options in the OTC markets may not be as liquid as exchange-listed options. The Fund may find the terms of counterparties in the OTC markets to be less favorable than the terms available for listed options. Moreover, the SEHK may suspend the trading of options in volatile markets which may casue the Fund unable to write Reference Index Call Options at times

- The use of futures contracts involves market risk, volatility risk, leverage risk and negative roll yields and “contango” risk.

- Investing in Reference Index Futures and writing Reference Index Call Options generally involve the posting of margin. If the Fund is unable to meet its investment objective as a result of margin requirements imposed by the HKFE, the Fund may experience significant losses.

- The Fund employs an actively managed investment strategy. The Fund may fail to meet its objective as a result of the implementation of investment process which may cause the Fund to underperform as compared to direct investments in the constituent equity securities of the Reference Index.

- The Fund is exposed to concentration risk by tracking a specific regions or countries.

- To the extent that the constituent securities of Reference Index are concentrated in securities of a particular sector or market, the investments of it may be similarly concentrated.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X Hang Seng High Dividend Yield ETF (the “Fund”) is to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Hang Seng High Dividend Yield Index.

- Whether or not distributions will be made by the Fund is at the discretion of the Manager taking into account various factors and its own distribution policy. There can be no assurance that the distribution yield of the Fund is the same as that of the Index.

- The Fund may invest in mid-sized companies, which may have lower liquidity and their prices are more volatile to adverse economic developments.

- The Fund invests in the emerging markets which may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risks, currency risks/control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X US Treasury 3-5 Year ETF (the “Fund”) is to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Mirae Asset US Treasury 3-5 Year Index (the “Underlying Index”).

- The Fund is exposed to the Credit/Default risk of issuers of the debt securities that the Fund may invest in; the Credit Rating risk that the credit ratings assigned by rating agencies are subject to limitations and do not guarantee the creditworthiness of the security and/or issuer at all times; the Downgrading risk that the Manager may or may not be able to dispose of the debt securities that are being downgraded; the Interest rate risk that the prices of debt securities rise when interest rates fall, whilst their prices fall when interest rates rise; the Policy risk that the changes in macro-economic policies in the US may have an influence over the US’ capital markets and affect the pricing of the bonds in the Fund’s portfolio, which may in turn adversely affect the return of the Fund; the Sovereign debt risk that the Fund’s investment in US Treasury securities may be exposed to political, social and economic risks that the Fund may suffer significant losses when there is a default of the US Treasury; the valuation risk that the valuation of the Fund’s instruments may involve uncertainties and judgmental determinations. If such valuation turns out to be incorrect, this may affect the Net Asset Value calculation of the Fund.

- The Underlying Index is a new index. The Underlying Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Underlying Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history.

- The Underlying Index is subject to concentration risk as a result of tracking the performance of a single geographical region, namely the US, and is concentrated in debt securities of a single issuer, namely the US Treasury. The Fund’s value may be more volatile than that of a fund having a more diverse portfolio and may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the US market.

- The base currency of the Fund is USD but the trading currency of the Fund is in HKD. The Net Asset Value of the Fund and its performance may be affected unfavourably by fluctuations in the exchange rates between these currencies and the base currency and by changes in exchange rate controls.

- The borrower may fail to return the securities lent out in a timely manner or at all. The Fund may as a result suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests. As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the collateral, adverse market movements in the collateral value or change of value of securities lent. This may cause significant losses to the Fund.

- The trading price of the Units on the SEHK is driven by market factors such as the demand and supply of the Units. Therefore, the Units may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- Payments of distributions out of capital and/or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions involving payment of distributions out of capital or effectively out of capital of the Fund may result in an immediate reduction in the Net Asset Value per Unit of the Fund and will reduce the capital available for future investment.

Monthly Commentary

Income ETFs – September 2025

Distribution is not guaranteed. Distribution may be made out of capital. Positive yield does not mean positive return. Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Share of the Fund and will reduce the capital available for future investment.

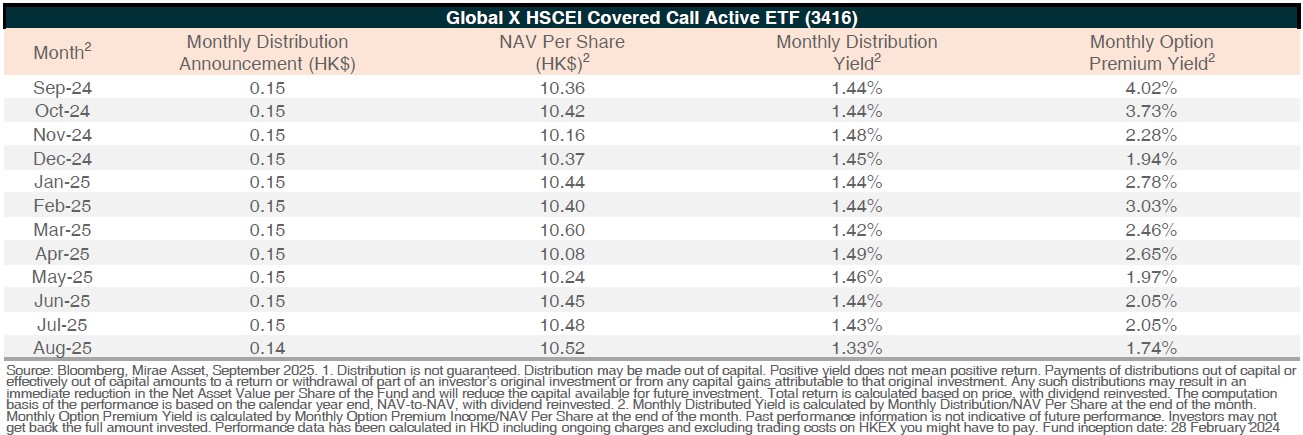

Global X HSCEI Covered Call Active ETF (3416)

- Monthly Distribution Paid in August 2025: The ETF distributed HK$0.15 per share on 6 August 2025.

- Monthly Distribution Announcement in August 2025: The ETF announced monthly distribution of HK$0.14 per share on 14 August 2025, to be distributed on 4 September 2025.

- Premium Earned in August 2025: Premium earned by selling index call options for the HSCEI edged down to 1.74% in August 2025, due to decline in market volatility.

- Total Return: The Year-to-date total return as of 29 August 2025 is 12.52% (including 12.04% distribution return and 0.48% price return).

For further performance information please visit the 3416 product page

Source: Bloomberg, Mirae Asset, September 2025. 3416 inception date: 28 February 2024. Past performance information is not indicative of future performance. Investors may not get back the full amount invested. The computation basis of the performance is based on price, with dividend reinvested. Performance data has been calculated in local currency. Where no past performance is shown there was insufficient data available in that year to provide performance. Where no past performance is shown there was insufficient data available in that year to provide performance. The downside of adopting a covered call strategy is that the Fund’s opportunity to profit from an increase in the level of the Reference Index is limited to the strike price of the Call Options written, plus the premium received. If a Call Option expires and if there is a decline in the market value of the Reference Index during the option period, the premiums received by the Fund from writing the Call Options may not be sufficient to offset the loss realized.

Monthly Option Premium and Distribution History (Past 12 Months)1

Calendar Year Performance

Source: Mirae Asset; September 2025.

| Year | 2024 | 2023 | 2022 | 2021 | 2020 |

|---|---|---|---|---|---|

| Fund | — | — | — | — | — |

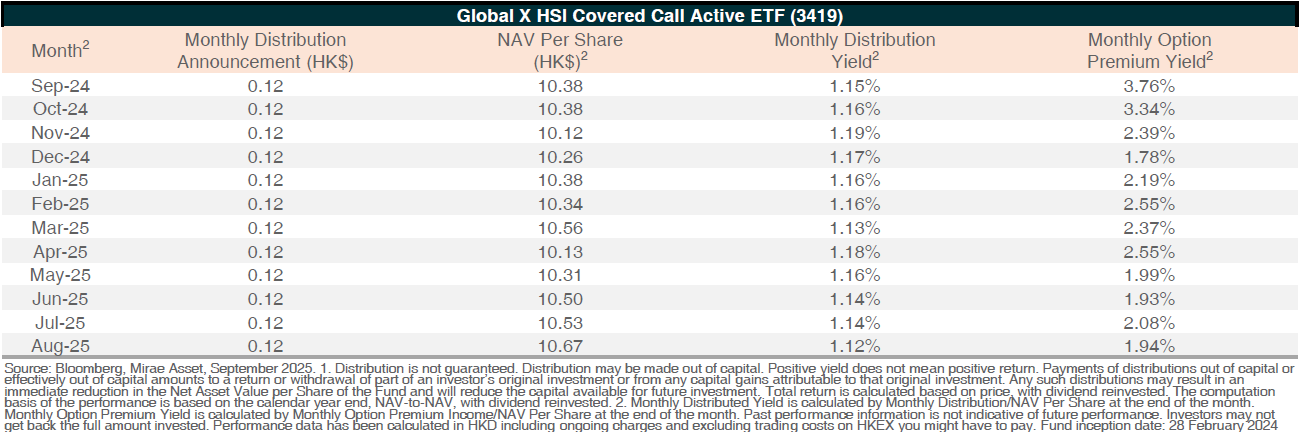

Global X HSI Components Covered Call Active ETF (3419)

- Monthly Distribution Paid in August 2025: The ETF distributed HK$0.12 per share on 6 August 2025.

- Monthly Distribution Announcement in August 2025: The ETF announced monthly distribution of HK$0.12 per share on 14 August 2025, to be distributed on 4 September 2025.

- Premium Earned in August 2025: Premium earned by selling index call options for the HSI edged down to 1.94% in August 2025, due to decline in market volatility.

- Total Return: The Year-to-date total return as of 29 August 2025 is 12.71% (including 9.83% distribution return and 2.88% price return).

For further performance information please visit the 3419 product page

Source: Bloomberg, Mirae Asset, September 2025. 3419 inception date: 28 February 2024. Past performance information is not indicative of future performance. Investors may not get back the full amount invested. The computation basis of the performance is based on price, with dividend reinvested. Performance data has been calculated in local currency. Where no past performance is shown there was insufficient data available in that year to provide performance. Where no past performance is shown there was insufficient data available in that year to provide performance. The downside of adopting a covered call strategy is that the Fund’s opportunity to profit from an increase in the level of the Reference Index is limited to the strike price of the Call Options written, plus the premium received. If a Call Option expires and if there is a decline in the market value of the Reference Index during the option period, the premiums received by the Fund from writing the Call Options may not be sufficient to offset the loss realized.

Monthly Option Premium and Distribution History (Past 12 Months)1

Calendar Year Performance

Source: Mirae Asset; September 2025.

| Year | 2024 | 2023 | 2022 | 2021 | 2020 |

|---|---|---|---|---|---|

| Fund | — | — | — | — | — |

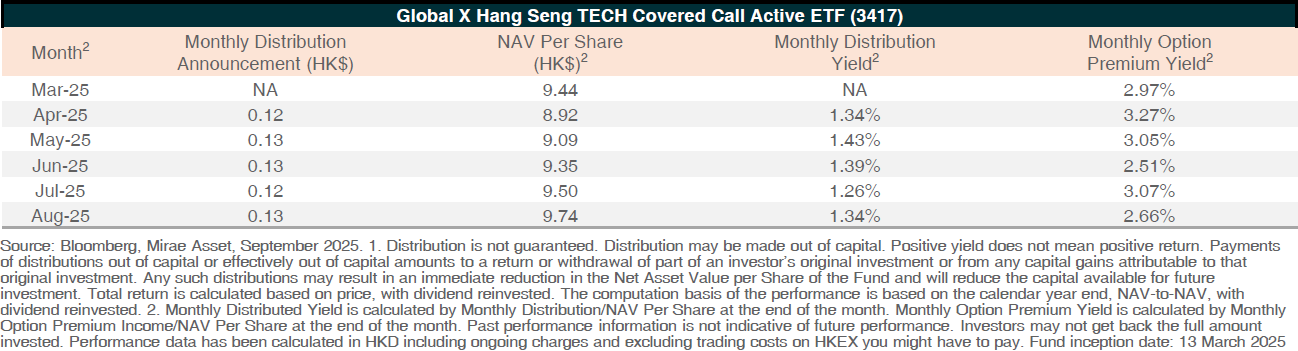

Hang Seng TECH Components Covered Call Active ETF (3417)

- Monthly Distribution Paid in August 2025: The ETF distributed HK$0.12 per share on 6 August 2025.

- Monthly Distribution Announcement in August 2025: The ETF announced monthly distribution of HK$0.13 per share on 14 August 2025, to be distributed on 4 September 2025.

- Premium Earned in August 2025: Premium earned by selling index call options for the Hang Seng TECH edged down to 2.66% in August 2025.

For further information please visit the 3417 product page

Monthly Option Premium and Distribution History (Past 12 Months)1

Source: Bloomberg, Mirae Asset, September 2025. 3417 inception date: 13 March 2025. Past performance information is not indicative of future performance. Investors may not get back the full amount invested. The computation basis of the performance is based on price, with dividend reinvested. Performance data has been calculated in local currency. Where no past performance is shown there was insufficient data available in that year to provide performance. Where no past performance is shown there was insufficient data available in that year to provide performance. The downside of adopting a covered call strategy is that the Fund’s opportunity to profit from an increase in the level of the Reference Index is limited to the strike price of the Call Options written, plus the premium received. If a Call Option expires and if there is a decline in the market value of the Reference Index during the option period, the premiums received by the Fund from writing the Call Options may not be sufficient to offset the loss realized.

Global X Hang Seng High Dividend Yield ETF(3110)

Market Update

Hang Seng High Dividend Yield Index recorded flat return in August 2025. An extended US-China tariff negotiation deadline, rising expectations for Fed’s rate cut, abundant onshore liquidity going into equities, and solid southbound inflows, defied weak macro data and normal seasonal weakness in August. We believe high dividend strategy should remain attractive thanks to solid dividend yields and lower volatility. PBOC’s buyback relending program should drive an increase in corporate share repurchase and enhance overall shareholder returns. In addition, there are potential incremental fund flows from household savings currently deposited in the bank to seek higher yield, as savings rates in onshore China remains at a low level.

Stock Comments

- China Hongqiao (1378 HK) gained 22% in the month, a key contributor to the ETF. The company reported better than expected 1H25 results, with recurring NP of Rmb14.5bn, +31% YoY and above market consensus. Company did not pay interim dividend in 1H25, but guaranteed that the full-year dividend payout ratio for Hongqiao for 2025 will be no lower than that in 2024, which was ~63%. Hongqiao also announced a new share repurchase plan of > HK$3bn. Potentially accelerating US fed rate cut could benefit commodity price, and attractive dividend yield could gain more fund flows. (Company data, August 2025)

- Yue Yuen (551 HK) gained 11% in the month. 2Q25 results were largely in-line, with Net profit higher than expectation due to lower tax rate and fair value gains on financial instruments. Though growth uncertainty prevails, current undemanding valuation still leads to attractive dividend yield. (Company data, August 2025)

- Hang Lung Properties (101 HK): Hang Lung announced HK$0.12 dividend per share in 1H25, flat YoY. Management anticipates its PRC tenant sales to narrow further or turn positive in 2H25 esp. against a low base in 3Q24, if no further significant deuteriation in consumer and business sentiments. New project completion should enhance recurring income resilience, supporting the dividend payment. LTM dividend yield for Hang Lung is 6.6%. (Company data, August 2025)

- COSCO Shipping (1919 HK): COSCO Shipping announced RMB0.56 dividend per share in 1H25 based on unchanged payout of 49%, +7.7% YoY. LTM dividend yield for COSCO Shipping is 12%. (Company data, August 2025)

- Hysan Development (14 HK): Hysan announced HK$0.27 dividend per share in 1H25, flat YoY. Management reaffirmed its target to stable dividend distribution policy going forward, and has no plan to issue scrip dividend in avoidance of potential shareholding dilution. LTM dividend yield for Hysan is 7.4%. (Company data, August 2025)

- Orient Overseas (316 HK): Orient Overseas announced US$0.72 dividend per share in 1H25, +14% YoY. LTM dividend yield for Orient Overseas is 12%. (Company data, August 2025)

Preview

Hang Seng High Dividend Yield ETF is well positioned to benefit from increasing allocation from global investors in a global rate cutting cycle. Notably, the Hang Seng High Dividend Yield Index consists of over 50% (Bloomberg, July 2025) of its constituents in State Owned Enterprises. Supportive policies across consumption, property, and technology sectors, as well as the ongoing capital market reforms are key drivers for market rebound. The concept of the Valuation System with Chinese Characteristics (“VCC”) is back in the spotlight again in light of recent developments. The primary objective of VCC is to enhance the quality and investment value of listed companies, especially SOEs. By investing in the Hang Seng High Dividend Yield Index, investors can gain exposure to high dividend-paying and low-volatility companies while also benefiting from the accelerated implementation of VCC.

Global X US Treasury 3-5 Year ETF(3450)

Market Update

Intermediate-term U.S. Treasuries saw modest capital appreciation in August 2025, supported by significant downward revisions to May and June payroll figures, which strengthened expectations for Fed rate cuts. Chair Powell’s speech further reinforced expectations for a September cut, stating that “downside risks to employment are rising” and that “a reasonable base case is that the effects will be relatively short-lived.” He concluded that “with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance”, making his most dovish remarks since May 2025. By the end of August, yields on 3–5 year US Treasuries declined to 3.63%, delivering a 1.36% monthly return for the Mirae Asset US Treasury 3–5 Year Index. (Mirae Asset, Bloomberg, August 2025)

The August employment report intensified concerns over labor market softening, triggering a broad rally as markets priced in heightened downside risks and the likelihood of decisive Fed action. Nonfarm payrolls rose by just 22k, significantly below the consensus estimate of 75k. The four-month rolling average now stands at 27k—a sharp deceleration from the 150k average recorded between May 2024 and April 2025. Private sector job growth averaged only 39k over the past four months, marking the weakest period since the pandemic. Unemployment and wage metrics further supported the case for rate cuts. The unemployment rate held at 4.3%, matching expectations but reaching the highest level since 2021. Wage growth also moderated, with average hourly earnings rising 0.28% month-over-month in August, below the 0.32% average observed in the four months preceding last September’s rate cut.

Preview

Looking ahead, the August jobs report likely clears the final major hurdle for the FOMC to deliver a 25bp rate cut at its mid-September meeting. The Global X US Treasury 3–5 Year ETF is well positioned to benefit from the resulting capital appreciation. We continue to favor intermediate-duration Treasuries over longer maturities, as concerns around Fed independence and upside inflation risks are exerting bearish pressure on the long end of the curve.