Important Information

Global X China Cloud Computing ETF

Global X China Clean Energy ETF

Global X China Consumer Brand ETF

Global X China Electric Vehicle and Battery ETF

Global X China Semiconductor ETF

Global X China Robotics and AI ETF

Global X China Biotech ETF

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. There is no guarantee of the repayment of the principal. Investors should note:

- Global X China Cloud Computing ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Companies in the internet sector may face unpredictable changes in growth rates and competition for the services of qualified personnel. The products and services offered by internet companies generally incorporate complex software, which may contain errors, bugs or vulnerabilities.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Clean Energy ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Many clean energy companies are involved in the development and commercialization of new technologies, which may be subject to delays resulting from budget constraints and technological difficulties. Obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants and general economic conditions also significantly affect the clean energy sector.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Consumer Brand ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- The performance of companies in the consumer sector are correlated to the growth rate of the global market, individual income levels and their impact on levels of domestic consumer spending in the global markets, which in turn depend on the worldwide economic conditions, which have recently deteriorated significantly in many countries and regions and may remain depressed for the foreseeable future.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Electric Vehicle and Battery ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Electric vehicle companies invest heavily in research and development which may not necessarily lead to commercially successful products. In addition, the prospects of Electric vehicle companies may significantly be impacted by technological changes, changing governmental regulations and intense competition from competitors.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Semiconductor ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Semiconductor industry may be affected by particular economic or market events, such as domestic and international competition pressures, rapid obsolescence of products, the economic performance of the customers of semiconductor companies and capital equipment expenditures. These companies rely on significant spending on research and development that may cause the value of securities of all companies within this sector of the market to deteriorate.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Robotics and AI ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Robotics and artificial intelligence sector is sensitive to risks including small or limited markets for such securities, changes in business cycles, world economic growth, technological progress, rapid obsolescence, and government regulation. These companies rely on significant spending on research and development and tend to be more volatile than securities of companies that do not rely heavily on technology.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Biotech ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Biotech companies invest heavily in research and development which may not necessarily lead to commercially successful products, and the ability for biotech companies to obtain regulatory approval (for example, product approval) may be long and costly.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

Monthly Commentary on Key Themes – July 2023

Listen

[2845/9845] Global X China EV & Battery ETF

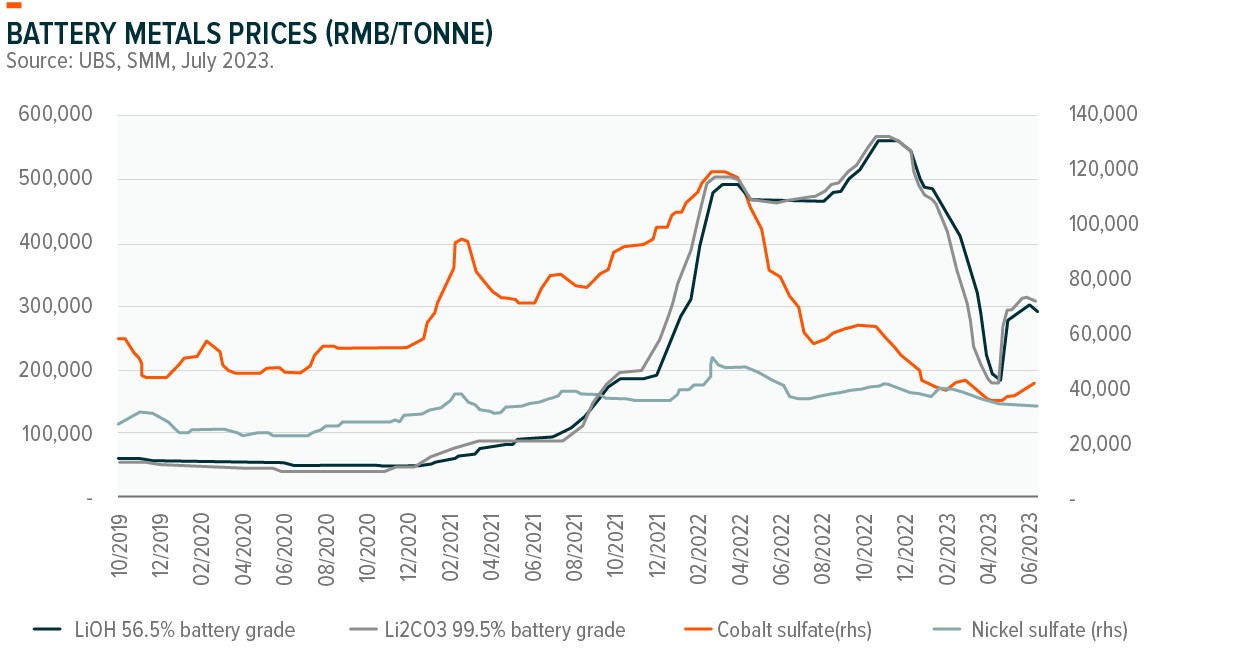

Battery production to grow in June: China’s power battery installation reached 28.2GWh in May 2023, up 12.3% MoM and 52.1% YoY. In the same month, China‘s power battery production reached 56.6GWh, up 20.4% MoM and 59.0% YoY. As per the 3-month average production and installation data, implied months of China power battery inventories were 2.1x in May (vs 1.9x in April) and 1.8x for the 2-year historical average months of power battery inventory.1 According to ICCSINO, a local consultant, production scheduling of major battery materials is forecasted to accelerate in June, partly because May productions fell short of expectations.2

Auto sales recovering while EV penetration stays solid: According to the China Passenger Car Association (CPCA) data, the June China passenger car production volume reached 2.2mn units (+10% mom and flat yoy). China’s new electric vehicle (NEV) (excl. commercial vehicles) wholesale volume increased 33.4% YoY and 12.1% MoM to 761k units. Year-to-June NEV whole sales reached 3.54mn units (+43.7% yoy). The penetration in June was 33.7% (+8ppts yoy). Based on the announcements of individual auto companies, the June wholesale volume data stays solid. BYD, Li Auto, Xpeng, and Nio delivered +6%/+15%/+15%/+16% MoM, respectively.

Supportive policy continues: On 21 June, China unveiled a RMB 520 billion package to boost sales of electric vehicles and other green cars over the next four years to prop up softening auto demand. New energy vehicles purchased in 2024 and 2025 will be exempted from purchase tax amounting to as much as RMB 30,000 per vehicle, with the exemption halving for purchases made in 2026 and 2027, the Ministry of Finance said in a statement. The move is an extension of the current policy under which NEVs (which include all-battery electric vehicles, plug-in petrol-electric hybrids, and hydrogen fuel-cell vehicles) are exempt from purchase tax until the end of 2023. Wednesday’s announcement is the fourth extension. The tax break was announced in 2014 and extended in 2017, 2020, and 2022.

Positive progress in overseas expansion: On 13 June, the Biden administration allowed Chinese electric vehicle battery company Gotion to move forward with the construction of a facility in Michigan after a months-long national security review. Earlier this year, Gotion voluntarily paused its development plans and requested the federal review amid intense scrutiny about its ties to China. In October 2022, Democratic Michigan Gov. Gretchen Whitmer announced that Gotion would invest USD 2.4 billion to construct two 550,000 square foot production plants along with other supporting facilities spanning 260 acres in northern Michigan. She applauded the proposal, saying it would shore up Michigan’s status as the “global hub of mobility and electrification”. And in a 10-9 vote in April, the Michigan State Senate Appropriations Committee gave the final stamp of approval for granting Gotion USD 175 million in direct taxpayer funding to help build the facility.

Battery material costs have stabilized: China lithium carbonate stabilized at around RMB 300-310k/tonne in June (+30% MoM on average) and trended slightly weaker towards the end of the month. Momentum for restocking slowed as the recovery remains moderate. Cobalt sulfate prices have slightly recovered and reached a level close to RMB 42k/tonne.

[2806/9806] Global X China Consumer Brand ETF

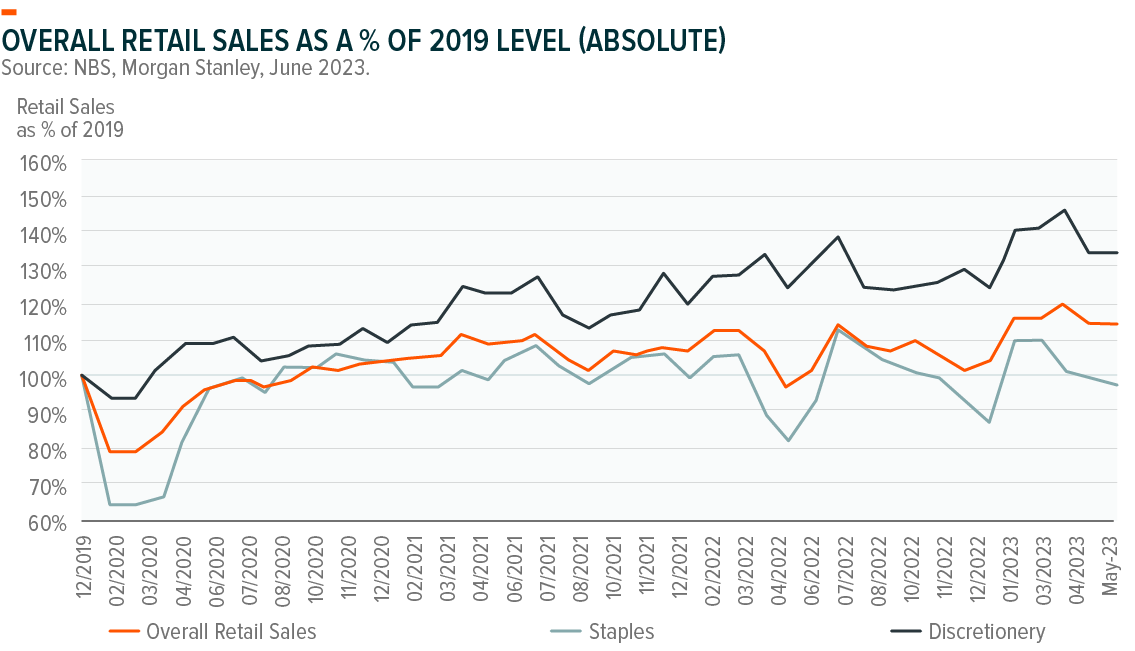

China’s consumption recovery pace remains somewhat sluggish. May retail sales growth came in at +12.7% YoY, decelerating from April’s +18.4% YoY growth. This implies that May retail sales reached 115% of 2019, similar to April’s at 114% of 2019. Consumer staples recovered to 135% of 2019 levels in May, while consumer discretionary sales remained slightly below pre-Covid levels at 98% of 2019.

Results from the 618 online shopping festivals were largely in-line with expectations. Alibaba reported positive gross merchandise value (GMV), user, and merchant growth as they focused more on user engagement and participation than mere GMV growth. JD also shared that its 618 performance surpassed all growth expectations, with strong performance coming in particular from apparel, beauty, and home appliances. Other platforms like PDD and Douyin also seemed to have robust growth this year as PDD adjusted the value of subsidies during the period, and Douyin benefited from continuous strong momentum in live streaming growth.

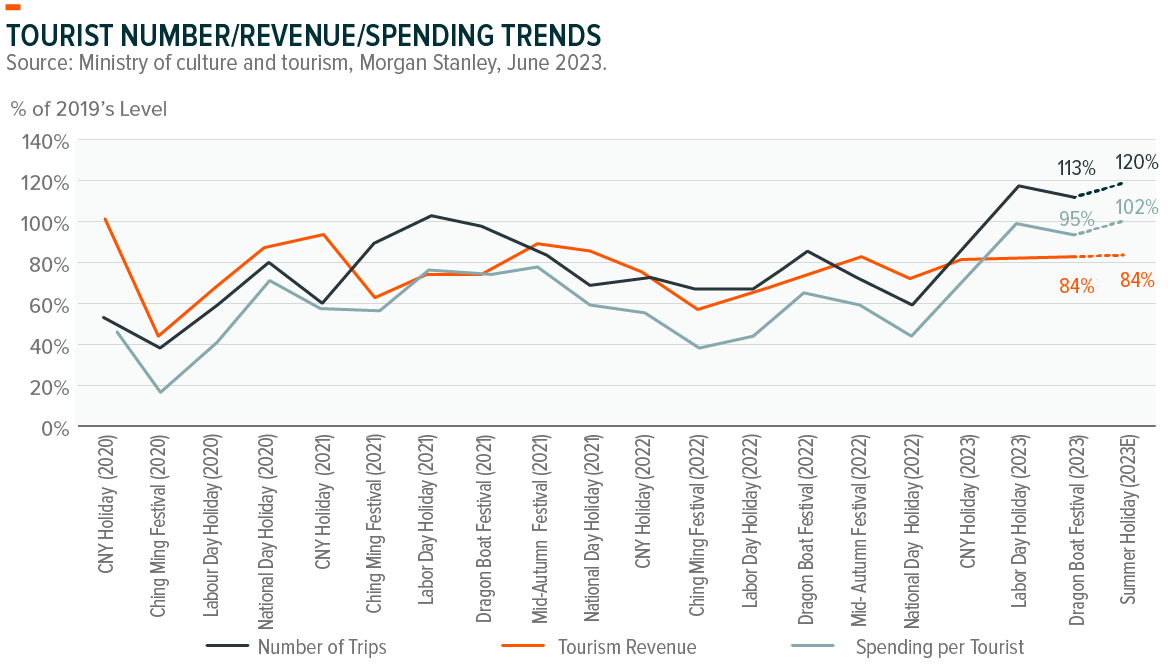

This year’s dragon boat festival also showed a similar trend to the previous holiday season. During the three days from 22nd to 24th June, the number of domestic tourists surpassed pre-Covid levels, reaching 113% of 2019. However, overall tourism revenue remained below pre-pandemic reaching 95% of 2019.

While consumer sentiment remains weak, prices of premium baijiu are still holding up well, similar to the strong demand we’ve seen for other luxury goods. While the market does not expect price hikes from Baijiu companies this year, revenue growth will be driven by volume as well as sales mix improvement. The premiumization trend is continuing in the beer industry, with premium beer volume growing faster than that of the value segment. Anta, a leading local sportswear company, also shared that high-end brands have been growing faster than mass-market brands because the middle class are under more stress than high-income or wealthy consumers in China.

That said, we are also seeing a K consumption trend in China, with consumers trading down in some consumer categories. This is part of the reason why PDD’s GMV is growing faster than that of JD or Alibaba. In addition, Eastroc Beverages, an energy drink company with a compelling value proposition, showed robust growth this year. Moreover, leading local cosmetic companies seemed to grow faster than many foreign brands this year as most local brands still largely cater to the masstige or mass markets.

We expect a more gradual consumption recovery this year as we need consumer sentiment to improve for high household savings to translate into consumption in a more meaningful way. We expect economic recovery will lead to wage growth and job market improvement, ultimately leading to consumption growth in the coming quarters.

[2809/9809] Global X China Clean Energy ETF

Solar

We’ve witnessed a dramatic come down in polysilicon prices. Current prices are around RMB 60-70/kg3, much closer to the production cost of some new players or second-tier producers. Feedback from channel checks showed that utilization has fallen, and some polysilicon makers started suspending their repair and maintenance capacity. Newcomers have also delayed project construction. Yet, top polysilicon players, particularly Tongwei, are still on the path of aggressive capacity expansion, which would be a good advantage to consolidate their leading position.

Concerns about oversupply along the solar value chain became the focus after the record-hot SNEC PV Power Expo. More joined in solar cell innovation with TOPCON or HJT products, while existing solar players tried to prevent competition with more aggressive capacity expansion plans.

We believe the deep stock price corrections over the last two months have largely priced in the risk, leading to a sector valuation that is now quite attractive. Additionally, on the bright side, high-efficiency solar cells will be the next tension point for further competition, citing the feedback from SNEC, for which the leading solar players would be the key beneficiaries. Longi introduced their new products with a conversion rate amounting to 26.81%4.

Wind

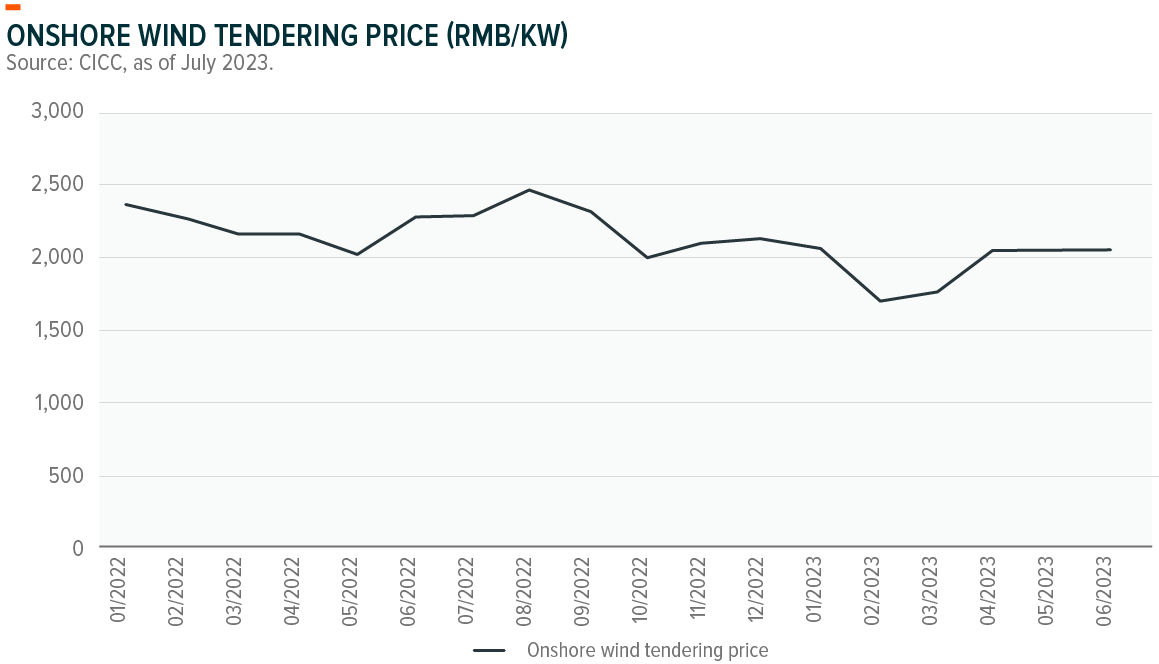

The latest monthly data points indicate that onshore wind tendering procurement pricing has stabilized at around RMB 2000/kW in June, similar to May and April levels but higher than the 1Q average of RMB 1844/kW. Wind turbine installations slowed down sequentially in May to just 200MW vs. March and April but is still up 74% YoY. Year-to-May wind installations grew by 51% and reached 16GW, falling below the tendering volume last year of 91GW. Some experts attribute that to the local province or city-level leadership changes during 2Q. The China open market wind tendering volume rebounded in June. Year-to-June tendering volume reached 34GW.5

According to Windmango’s news on 31 May 2023, the Guangdong Provincial Development and Reform Commission recently announced the 2023 offshore wind competitive bidding work plan, with a remarkable capacity of 7GW (or 15 projects) offshore wind farms located in provincial-jurisdiction areas and 16GW (or 15 projects) in national-jurisdiction areas. The competitive bidding will start in early June, with the final bidding results to be announced by the end of August. This is a positive update to support a growing offshore wind capacity in China.

Old wind farm upgrading policy: On 13 June, the National Energy Administration (NEA) issued policy measures for managing the reconstruction, upgrade, and decommissioning of legacy wind turbines. Most of the content is largely similar to the draft for consulting version issued on 31 December 2021. Notably, the NEA highlights that it will strictly forbid any cheating on the collection of national renewable energy subsidies, likely implying a tighter auditing process on subsidy payments.

Siemens Energy’s design error is just a standalone issue: Siemens Energy on 23 June announced that it is withdrawing its profit guidance for the year, as its subsidiary, Siemens Gamesa, found that there was a quality issue with the wind turbine generator business. Based on the follow-up calls and meetings, the issue lies mostly in the design and assembly rather than parts manufacturing quality. We think there is limited impact on wind turbine makers outside of Siemens Energy. Chinese components and turbine players won’t be affected. But the pace of installation for new overseas wind turbines could be stalled for a while.

[2807/9807] Global X China Robotics & AI ETF

The latest monthly data points released by the National Bureau of Statistics reported on 15 June that China industrial robot production volumes were +4% YoY in May (+5% MoM vs April production volumes, vs past five years’ seasonality of -5% MoM); China machine tool production volumes were +2% YoY in May (+0% MoM vs April average production volumes, vs past five years’ seasonality of -6% MoM). Manufacturing fixed asset investment (FAI) was +5% YoY in May (stable vs +5% in April). High-tech manufacturing FAI was +13% YoY in May, moderating vs April’s +15% YoY.

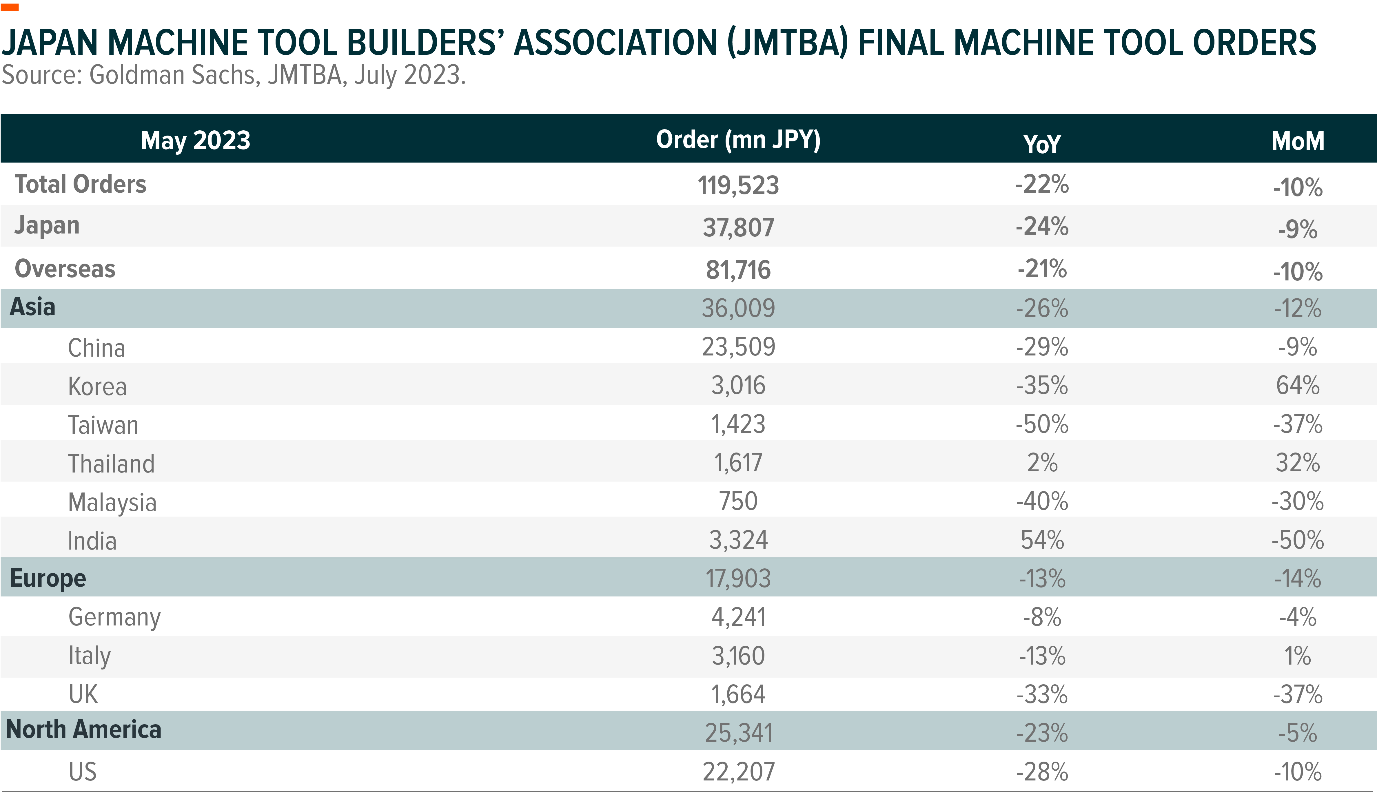

Weak global automation cycle, signs of bottoming out: Machine tool orders in May 2023 totalled ¥119.5 billion (-22% YoY, -10% MoM), including a further decline in domestic orders to ¥37.8 billion (-24% YoY, -9% MoM) and a sharp contraction in overseas orders to ¥81.7 billion (-21% YoY, -10% MoM). May data pointed to weakness across all regions, with few positive signs. However, Europe-related commentary from the JMTBA remained upbeat, suggesting that orders have largely bottomed out. Overall, we noted further signs of worsening momentum across all regions other than Europe and got the impression that a major bottom is approaching.

China automation data are showing weakness: May data appeared to confirm a clear slowdown in momentum. While EV investment remains the main driver, the data strongly suggest a gradual decline in the scale of orders per project. Some association members also noted signs of a peak in EV-related investment.

Newly released supportive policy framework: On 15 June, the Shanghai government released a three-year action plan (2023-2025) to intensify high-quality development in the manufacturing space, calling for enterprise digitization ratio to reach 80%+ and industrial robots density to reach 360 units per 10k people. On 28 June, the Beijing government also launched the Beijing robotics industry innovation and development action plan 2023-25. The plan aims, by 2025, to cultivate 100 high-value-added robotics products, with 100 nationwide applications to benchmark against leading international humanoid robot products, boosting the city’s robotics revenue to over RMB 30 billion.

[2826/9826] Global X China Cloud Computing ETF

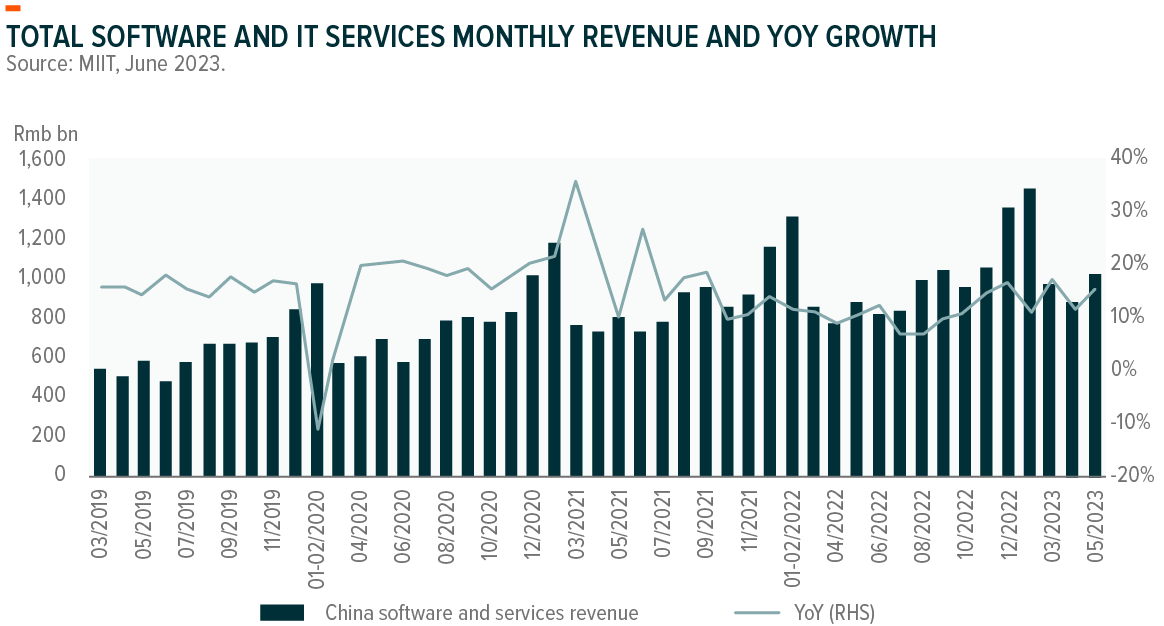

China’s Software industry May revenues grew +15% YoY to RMB 1.0 trillion (USD 125 billion), accelerating from April (+11% YoY), leading 5M23 revenues to increase by 13% YoY, according to MIIT. We see a software industry recovery in May post the slowdown in April. Into 2H23, the pace of recovery should be mostly gradual mainly because of a sustained fluid macroeconomic condition. Therefore, IT spending by private enterprises, SOEs, and local governments will not expect a meaningful rebound. Moreover, small / mid-scale enterprises could take longer time to recover than large enterprises.

The emergence of AIGC (AI-generated content) also brings new functions to software, enhancing human-machine interaction, which could expand the potential user base. AI also reduces software development costs, driving productivity efficiency for software companies.

China’s telco revenue grew only 5.0% YoY in May, the lowest since 2021. Mobile revenue grew 11.9% YoY due to a low base last year. Industrial internet grew only 11.6%,6 which has slowed for four consecutive months, driven partly by slowing cloud computing revenue growth. Despite a continuous slowdown, telecom operator’s cloud revenue growth still outpaced that of internet platforms, implying a market share gain, attributable to telco operators’ competitive edge in private cloud. For telco operators, industrial internet project revenues could be lumpy as implementation takes time. Therefore, growth could re-accelerate into 2H23 as project implementation is completed.

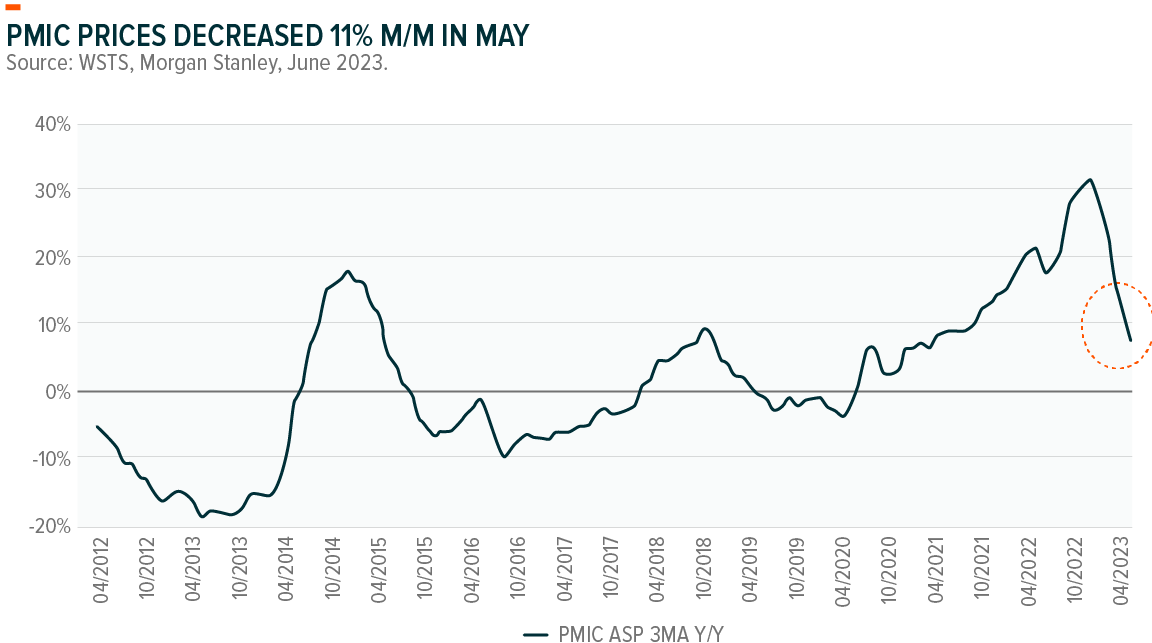

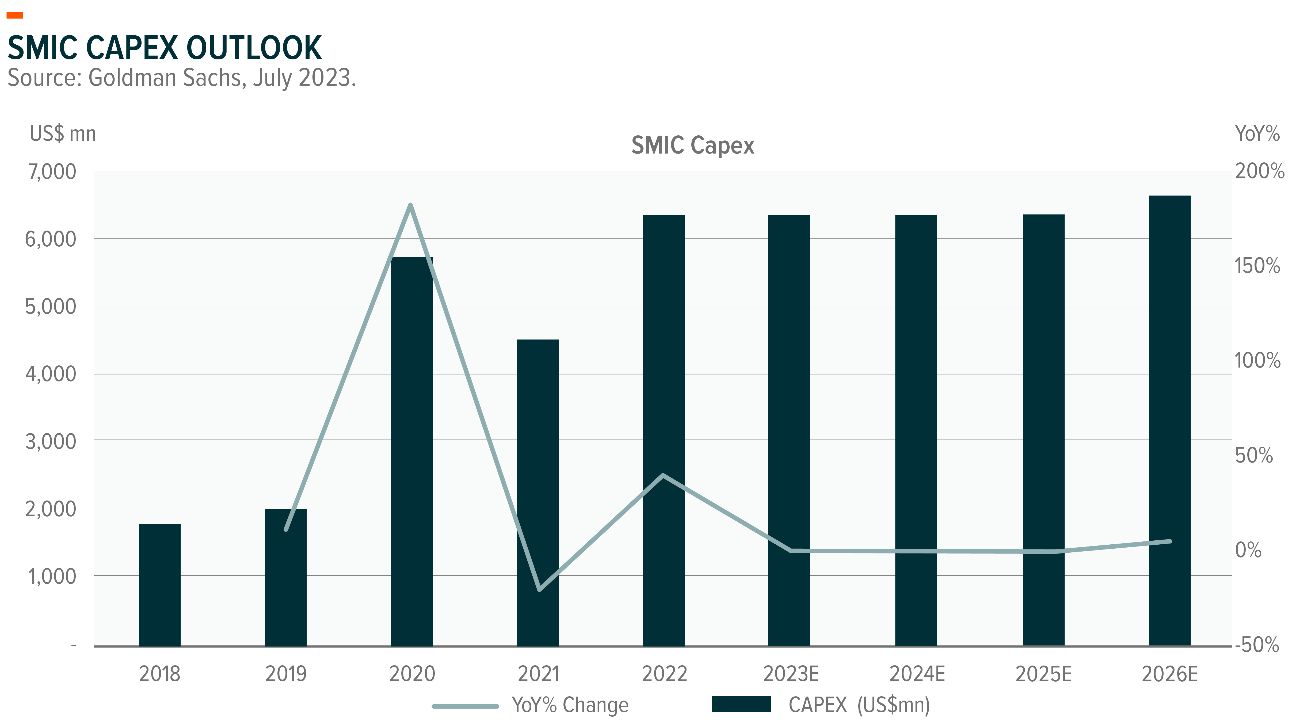

[3191/9191] Global X China Semiconductor ETF

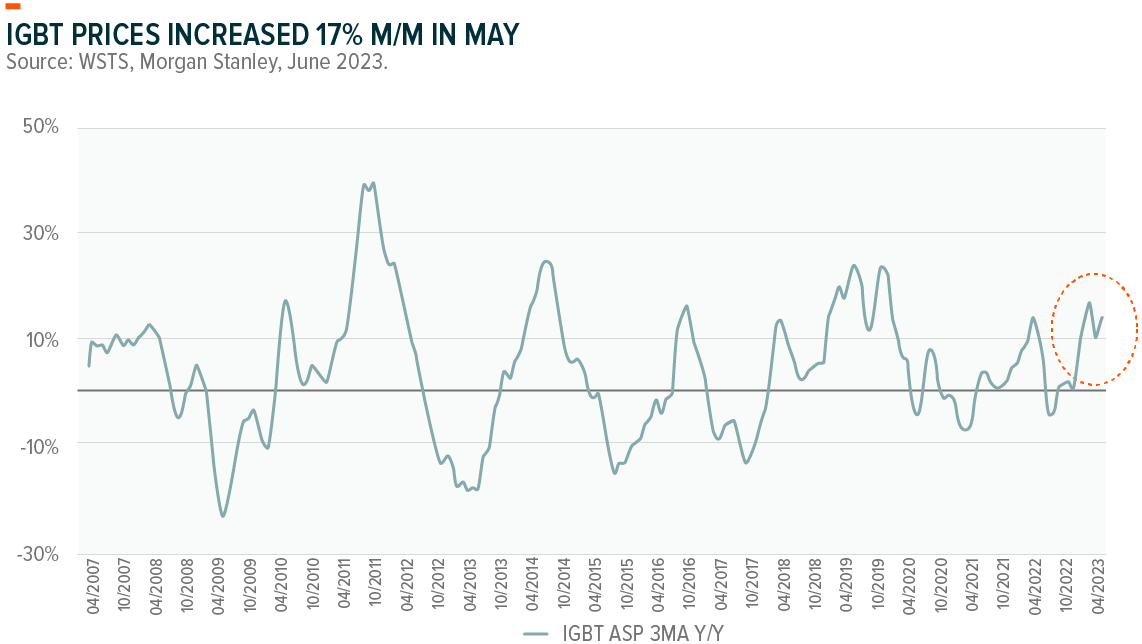

China IGBT price remains resilient while MOSFET and PMIC prices trend weaker: China’s IGBT market supply/demand and high voltage power discrete (IGBT, SiC) remains healthier than other power semis (MOSFET, PMIC). Producer and distributor inventory levels remain normal for IGBT, combined with resilient demand from new energy applications supporting the pricing.

Commitment to high CAPEX from top foundries in China supports domestic equipment makers: SMIC and Hua Hong plan to sustain high CAPEX levels, providing support to the domestic semiconductor equipment makers. SMIC guided flattish capex in 2023 for long-term growth. Hua Hong targets to expand Wuxi fab capacity from 65k wafers/month currently to 95k wafers/month by end-2023. The company is also planning the second 12” fab at Wuxi, targeting to start production in 2024.

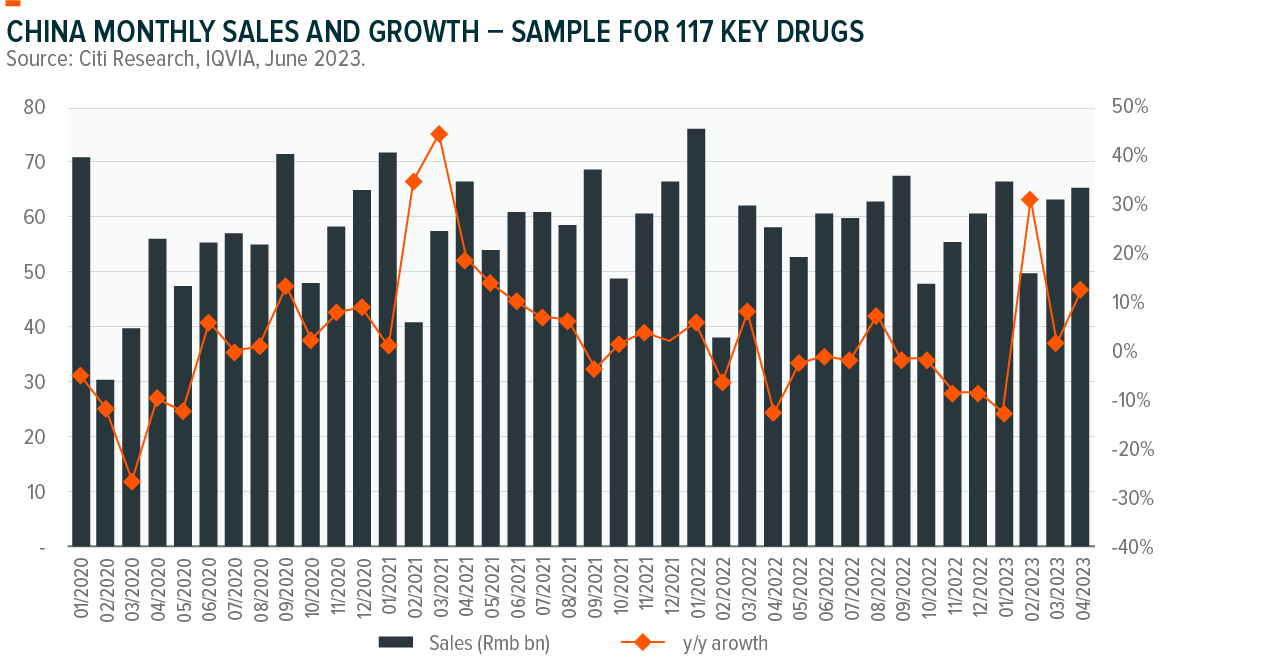

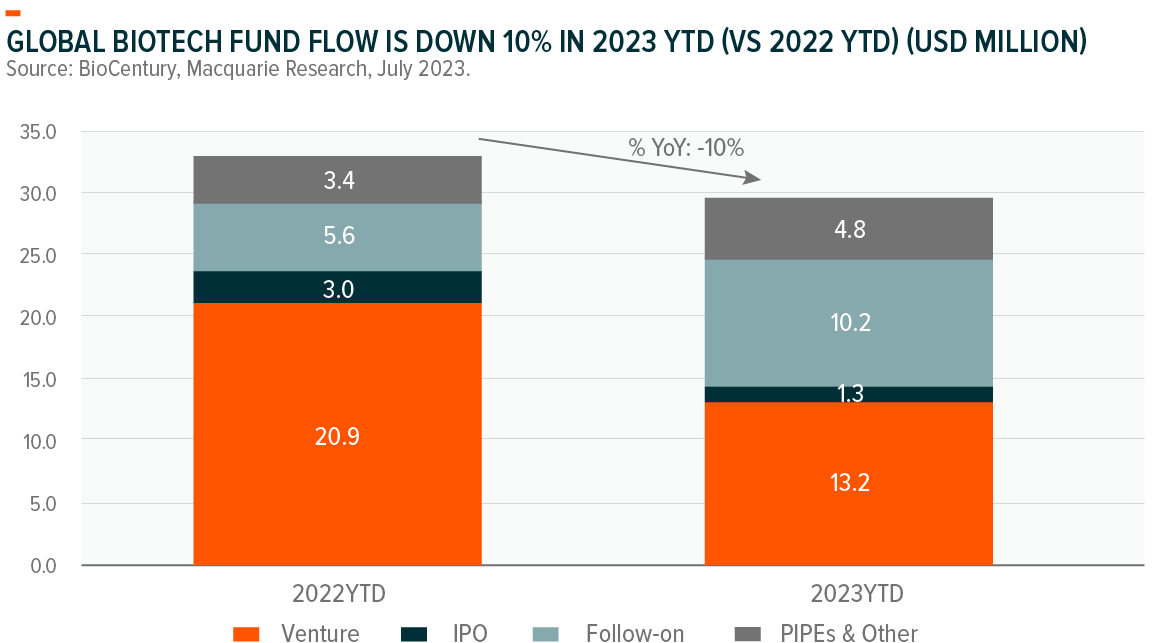

[2820/9820] Global X China Biotech ETF

Overcapacity in CMOs (Contract Manufacturing Organizations) concerns overdone: Sartorius (a manufacturer of lab products and bioprocess systems, deriving ~25% EBITDA from CDMO companies while the rest from biopharma companies) has cut its guidance for 2023. This caused the market to worry about overcapacity in the CMO industry (including China). However, comments from Sartorius’ management suggest its guidance cut is mainly driven by destocking. Hence, we believe that the primary demand for CMO business continues to be healthy.

Pricing environment in CDMO continues to be healthy: Samsung Biologics management has denied any price cut move to fill its large new capacity in plant 4. The company expects plant 5 to start production in April 2025. Fujifilm also commented that they had not witnessed price competition. The Japanese CDMOs still hope to pass on their cost increase to clients. The CMOs may be able to tolerate excess capacity. The breakeven capacity utilization rate is 30-40% for Samsung Bio and 40-45% for Wuxi Bio. This should be positive for China-based CDMOs who have a cost advantage over global peers.

Biotech funding environment continues to be subdued globally

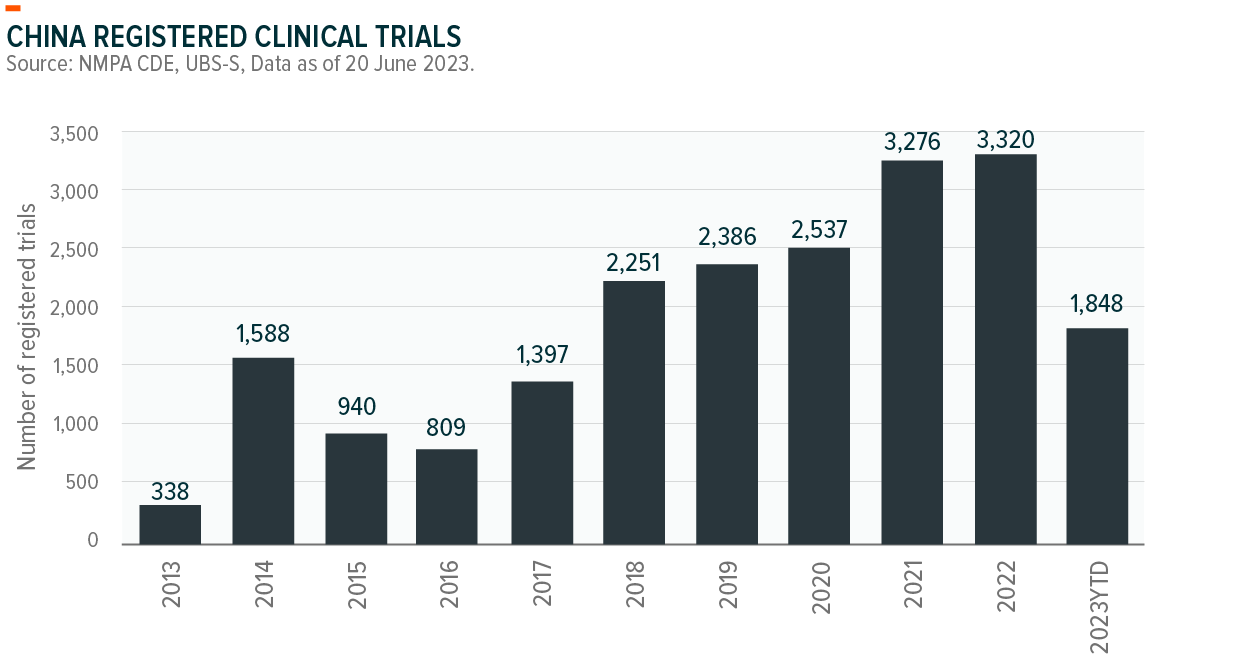

Underlying R&D effort in China continues to be healthy: The number of registered clinical trials YTD 2023 is higher, and at this run rate, overall 2023 filings could surpass the 2022 peak.

China prescriptions data: Hospital prescription sales in Jan-Apr 2023 recorded +4.4% YoY and volume +6.7% YoY, dragged by the pandemic. Meanwhile, hospital prescription sales in April 2023 rose 12.4% YoY and volume increased 17.4% YoY.