Important Information

Investors should not base investment decisions on this content alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X China Electric Vehicle and Battery ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Electric vehicle companies invest heavily in research and development which may not necessarily lead to commercially successful products. In addition, the prospects of Electric vehicle companies may significantly be impacted by technological changes, changing governmental regulations and intense competition from competitors.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X Hang Seng TECH ETF (the “Fund”) seeks to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Hang Seng TECH Index (the “Index”).

- The Fund’s investments are concentrated in companies with a technology theme. Technology companies are often characterised by relatively higher volatility in price performance. Companies in the technology sector also face intense competition, and there may also be substantial government intervention, which may have an adverse effect on profit margins. These companies are also subject to the risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences.

- The Fund’s investments are concentrated in securities listed on the Stock Exchange of Hong Kong (the “SEHK”) of companies that are active in technology sector may result in greater volatility in the value of the Fund than more diverse portfolios which comprise broad-based global investments. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the technology sector.

- The Index is subject to concentration risk as a result of tracking the performance of securities incorporated in, or with majority of revenue derived from, or with a principal place of business in, the Greater China region. The Fund’s NAV is therefore likely to be more volatile than a broad-based fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- The trading price of the Fund unit (the “Unit”) on the SEHK is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- Dividends may be paid from capital or effectively out of capital of the Fund, which may amount to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment and result in an immediate reduction in the Net Asset Value per Unit of the Fund.

- Global X China Clean Energy ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Many clean energy companies are involved in the development and commercialization of new technologies, which may be subject to delays resulting from budget constraints and technological difficulties. Obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants and general economic conditions also significantly affect the clean energy sector.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Consumer Brand ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- The performance of companies in the consumer sector are correlated to the growth rate of the global market, individual income levels and their impact on levels of domestic consumer spending in the global markets, which in turn depend on the worldwide economic conditions, which have recently deteriorated significantly in many countries and regions and may remain depressed for the foreseeable future.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Robotics and AI ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Robotics and artificial intelligence sector is sensitive to risks including small or limited markets for such securities, changes in business cycles, world economic growth, technological progress, rapid obsolescence, and government regulation. These companies rely on significant spending on research and development and tend to be more volatile than securities of companies that do not rely heavily on technology.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Cloud Computing ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Companies in the internet sector may face unpredictable changes in growth rates and competition for the services of qualified personnel. The products and services offered by internet companies generally incorporate complex software, which may contain errors, bugs or vulnerabilities.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Little Giant ETF’s (the “Fund’s”) objective is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive China Little Giant Index (the “Index”).

- The Index is a new index. The Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history.

- The Fund may invest in small and/or mid-capitalisation companies which may have lower liquidity and their prices are more volatile to adverse economic developments than those of larger capitalisation companies in general.

- The Fund’s investments are concentrated in companies which are characterised by relatively higher volatility in price performance. The Sub-Fund may be exposed to risks associated with different sectors and themes including semiconductor, industrial, pharmaceutical, energy and technology. Fluctuations in the business for companies in these sectors or themes will have an adverse impact on the net asset value of the Sub-Fund.

- Some of the companies classified as the Little Giants have a relatively short operating history. Such companies also face intense competition and rapid changes could render the products and services offered by these companies obsolete, which may have an adverse effect on profit margins.

- They may be more susceptible to risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences affecting those companies.

- The Mainland China is an emerging market. The Fund invests in Mainland Chinese companies which

- may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risk, currency risks or control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk and the likelihood of a high degree of volatility.

- Securities exchanges in the Mainland Chinese markets typically have the right to suspend or limit trading in any security traded on the relevant exchange. The government or the regulators may also implement policies that may affect the financial markets. All these may have a negative impact on the Fund.

- Listed companies on the ChiNext market and/or STAR Board are subject to higher fluctuation on stock prices and liquidity risk, over-valuation risk, less stringent regulation risk, delisting risk and concentration risk.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Fund.

- The trading price of the Shares on the SEHK is driven by market factors such as the demand and supply of the Shares. Therefore, the Shares may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Share of the Fund and will reduce the capital available for future investment.

Monthly Commentary on China Thematic ETFs – Sep 2024

Global X China Electric Vehicle and Battery ETF (2845 HK)

Industry Update

- Strong August EV Sales; NEV penetration exceeded 50%: According to CPCA estimate, August passenger NEV wholesale volume reached 1.05mn, +32% YoY.1 By individual brands, BYD reported August NEV sales of 373k units, +36% YoY, with PHEV continuing to record strong growth. Overseas sales grew by 5% MoM to 31.4k.2 Li Auto delivered 48k units in August, +38% YoY. Nio (+4% YoY) and Xpeng (+3% YoY) recorded weaker sales momentum in August. Xiaomi SU7 delivery exceeded 10k units in August, marking the third consecutive months over 10k deliveries after its launches in March. (for reference only, abovementioned stocks are not necessarily in the constituent list of the ETF). Based on insurance registration, new energy vehicle (NEV) penetration was 52% in the last week of August.3

- Tariff: European Commission announced a new draft decision on final countervailing duties on BEV imports from China, which are marginally lower than those disclosed in early July. Notably, tariff on China-made Tesla would be cut to 9% from previously planned 20.8% (on top of the 10% existing tariff). In addition, Canada says it will impose a 100% tariff on imports of China-made EVs.4

- Auto trade-in program upgraded: The trade-in stimulus has been doubled to Rmb20k (from Rmb10k) per NEV, and Rmb15k (from Rmb7k) per eligible ICEV,5 following central government’s indication that long-term government bonds could be used to fund consumer goods trade-in.6

- Battery material costs further declined: China’s spot lithium carbonate price declined by 8% MoM to around RMB 81 k/t at early August.7 Battery materials prices have decreased by over 80% from its peak in 2022, supporting the continued cost optimization for battery makers and EV manufacturers.

Stock Comments

- BYD’s stock price was up 1% in August, a positive contributor to the ETF. BYD reported in-line 2Q24 and 1H24 results on 28 August. 24Q2 net profit came in at Rmb9.1bn, up 98% q/q and 33% y/y with 63% q/q and 45% y/y volume growth.8 Management believed 4mn units of sales target is achievable this year, and looked for 5mn unit target in 2025, with upside coming from overseas and high-end sales.9 BYD launched the Song L DM-i and Song Plus DM-i in July, followed by the launch of the new Seal EV and Seal 07 DM-i in early August, adopting LiDAR for the first time.

- Li Auto’s stock price was down 3% in August. Li Auto reported 2Q24 results on 28 August, while overall results and guidance was solid and in-line with expectation, its share price dropped over 15% overnight, which should be attributable to non-fundamental reasons and fragile investor sentiments.10 Outlook for Li Auto remains positive due to solid 3Q guidance, improving market pricing environment, and undemanding valuations.

Preview

We remain positive on the long term growth potential for EV and battery value chain, along with the upward EV penetration trajectory. Domestic old car replacement demand, as stimulated by scaled-up auto trade-in program, together with export sales, should support China’s resilient auto momentum and benefit leading domestic brands. We expect the China auto market to stay competitive in 2024 with strong new product line-up and technology innovations from leading EV and battery brands, and new entrants such as Xiaomi. Geopolitical tensions remain the key risks, but China EV models will still remain competitive under new tariff landscape thanks to its cost advantages. Localized production will be the longer term solution for Chinese brands.

Global X Hang Seng TECH ETF (2837 HK)

Industry Update

Hang Seng TECH Index recorded a mild growth of 1% in August 2024. Major tech companies reported divergent 2Q results, with companies like Xiaomi and Meituan beating market expectation thanks to robust new business growth and improving outlook, while companies like Kuaishou and NetEase fell short of market expectation amid intensified competition. Weak domestic consumption sentiments also weigh on performance of consumption brand and advertising platform.

Stock Comments

- Tencent recorded return of 5% in August, a positive contributor to the ETF. Tencent reported solid 2Q24 results on 14 August, with Revenue and Adj. Operating Profit largely in-line with consensus expectation. Adj. Net Profit beat consensus by a large margin driven by share of profits from JV and Associates. Online games revenue recorded solid growth driven by strong performance of new games such as DnF mobile and rejuvenation of legacy titles including HoK and PKE. Game revenue growth should further accelerate in 2H24 as gross receipts outpaced revenue growth in past quarters for both domestic and international game business. Macro headwinds and consumption weakness weighed on advertising and payment business. Nevertheless, Tencent continue to deliver faster than peer advertising revenue growth (+19% YoY) thanks to Video Accounts monetization warp up and enhanced advertising efficiency through AI adoption.

- Xiaomi recorded return of 16% in August, a positive contributor to the ETF. Xiaomi reported strong 2Q24 results on 21 August, with revenue growing +32% YoY to Rmb 89bn, and adj. Net Profit growing +21% YoY to Rmb 6.2bn. Notably, Xiaomi’s first quarter of EV sales generated Rmb6.4bn in sales in 2Q and a 15.4% gross margin, ahead of the market’s expectation, which is driven by larger-than-expected volume and favourable terms provided by suppliers.11 EV GPM could further increase in 3Q driven by less promotional freebies, further supply chain and cost optimizations, and rising sales of car options

Preview

Though macro uncertainty and consumption softness could weigh on corporate revenue growth, we see unique positioning of Hang Seng Tech thanks to its attractive valuation, ongoing margin expansion, and continued ramp up in shareholder returns. With well-established ecosystem containing large user base and leading technology in place, we see further upside potential for these leading technology companies coming from the rapid development of structural growth themes such as EV and AI in China.

Global X China Clean Energy ETF (2809 HK)

Industry Update

China solar installation ended at 123.5GW as of July 2024, +27%yoy, with five consecutive months YoY growth. Domestic large-scale solar farm projects and solar module exporting to Europe are accelerating despite heat wave, driven by competitive solar panel cost and energy storage cost. China wind installation ended at 29.9GW as of July 2024, +14%yoy, in which July installation was 4.1GW, +23%yoy. We witnessed offshore wind projects tendering accelerating recently. China State Grid also significantly increased the investment in power grids to Rmb600bn in 2024, to better utilize the power generation by renewables.Renewables-related manufacturing players remain suffering from mismatch between supply and demand in the near term. Most of the major players booked poor 1H24 earnings recently. Supply chain prices are still sluggish due to oversupply. Power grid related companies, on the other way around, have better performance due to strong power grid CAPEX.

Stock Comments

- Sungrow Power Supply Co., Ltd. Class A: The company delivered strong Q2 results with energy storage sales much better than feared. Sungrow is a global leader in solar inverter and ESS integration business with great exposure to exporting.

- Ningbo Sanxing Medical Electric Co., Ltd. Class A: The company is a leading power-related equipment manufacturer in China, who benefits from power grid capex accelerating. Similarly, company delivered a strong Q2 result.

- China Three Gorges Renewables (Group) Co., Ltd. Class A: Solar power prices came down due to oversupply in a short period of time. Company still have a strong pipeline of solar installation in the near future which may negatively impact on profitability.

Preview

We remain constructive on the global clean energy growth and the trend of energy transition. However, we also must admit the near-term broad mismatch between supply and demand along solar/wind supply chains, which led to poor earnings for a couple of months or maybe even longer. It takes more time than expected for the small players to exit and demand to catch up, especially when China solar value chain are faced with geopolitical pushback from the United States. On the bright side, we have seen strong demand from some emerging markets like ASEAN, Middle East regions, Africa and South America, but it still needs more time.

Global X China Consumer Brand ETF (2806 HKD)

Industry Update

Following NDRC’s arrangement of Rmb300bn treasury bonds to support equipment upgrade and consumer trade-in in July, several local governments have started to unveil their trade-in details for consumer goods throughout the month. On August 10, Hubei province became the first region to kick off the trade-in program. More regions have followed to disclose their plans, namely Qinghai, Jilin, Ningxia, Hainan, Chongqing, Hunan, Guangdong, Beijing and Shanghai (which announced over Rmb4bn subsidies). We expect policy impact to become more apparent after September with local governments progressively rolling out their programs.

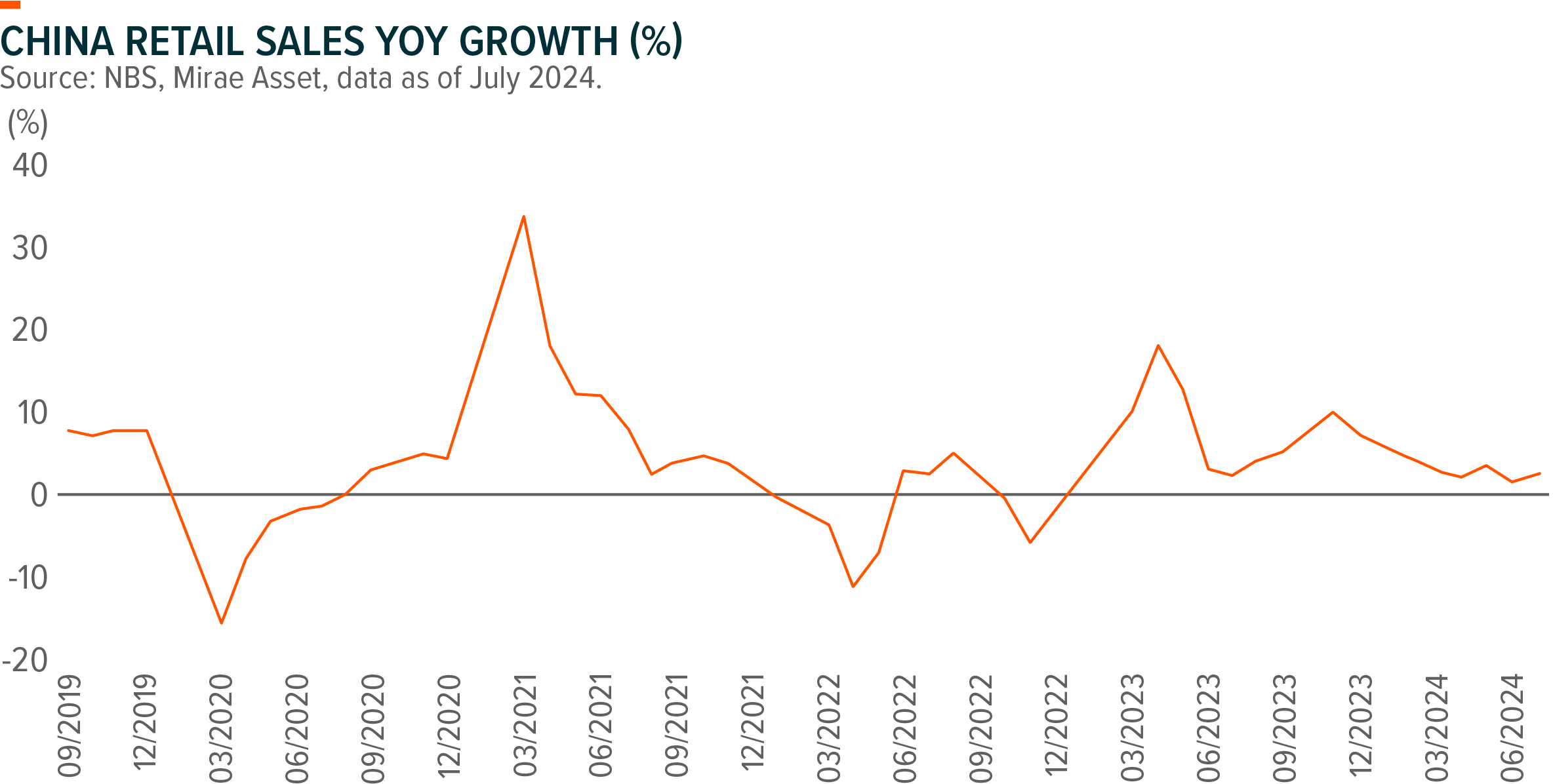

In July, China retail sales growth stood at +2.7% YoY (vs +2.0% YoY in June), largely in line with BBG consensus of 2.6% YoY. By region, rural areas (+4.6% YoY) continued to outperform urban areas (+2.4% YoY). The performance varies across categories. Sports and Entertainment Equipment (+10.7% YoY) and Soft Drinks (+6.1% YoY) experienced robust growth acceleration, likely fueled by the Olympic Games. Within staples, Food showed decent growth of 9.9% YoY. However, more discretionary goods faced challenges amid macro weakness. Jewellery experienced a widened YoY decline of -10% YoY despite a low base. Apparel, Shoes & Textile, and Electronics & Appliances remained in negative growth territory. Cosmetics continued to lag post the 618 online promotion, although YoY decline narrowed to 2.4% YoY vs. Jun.

Stock Comments

- Trip.com Group (TCOM US): Trip.com achieved a 9% return in August. 2Q24 revenue grew by 14% YoY to Rmb12.8bn, in line with consensus. Domestic room nights experienced robust double digits growth in 2Q and throughout the summer. The YoY decline of Hotel ADR stabilized in 3Q driven by higher leisure travel mix. Outbound air and hotel volume rebounded to 100% of 2019 levels in 2Q and is at 110-120% during the summer holiday. Non-GAAP OP reached Rmb4.2bn, with an OPM of 33.1%, beating consensus by 1.7ppt, mainly from opex savings. Management expects non-GAAP OPM continue to improve modestly going forward through enhanced efficiency and operating leverage.

- Anta Sports (2020 HK): Anta recorded gain of 8% in August on earnings beat and stock buyback initiatives. 1H24 sales grew by 14% YoY, with ANTA brand, FILA, and Descente/Kolon up 13%, 7% and 42%, respectively. GPM expanded 0.8ppt to 64.1% driven by GPM improvement across all core brands thanks to reduced discounts. NP (excl. Amer’s impact) rose by 17% YoY. Although sales in June and July were weaker, August witnessed an improvement. In addition to a 50% dividend payout ratio in 1H24, Anta announced a share buyback plan with up to HK$10bn in next 18 months, c.5% of its market cap on Aug 27 (announcement day) closing.

- Haier Smart Home (600690 CH): 2Q24 results is a mixed bag. Total revenue/net profit in 1H24 grew by 3%/16% YoY to Rmb135,623/10,420mn, implying flattish/13% YoY in 2Q24. By region, domestic/overseas revenue increased by 2.3/3.7% YoY in 1H24, indicating a largely similar YoY growth in overseas market but LSD-MSD% YoY decline in domestic market in 2Q24. GPM/OPM expanded by 0.2/1.1ppt YoY to 32.3/9.8% in 2Q, helped by improved mix, enhanced supply chain efficiency and digitalization. In 2H24, execution of consumer goods trade-in policy is in focus for domestic market.

Preview

China consumer is still facing uncertainties in the short term. As a late play of recovery story, the rebound of consumer sector still awaits more macroeconomic supportive signals. However, long term trends such as the ascendance of local brands and premiumization remain intact in our view. Quality leading players are better positioned to navigate through uncertain macro conditions and provide stability. While the recent policy supports have injected some positivity into the sector, their effects are yet to be apparent. For many consumer companies, 3Q is the peak season and sales performance during this period is vital for achieving their annual targets. We suggest to closely watch the policy impact roll out and 3Q performance of consumer companies.

Global X China Robotics and AI ETF (2807 HK)

Industry Update

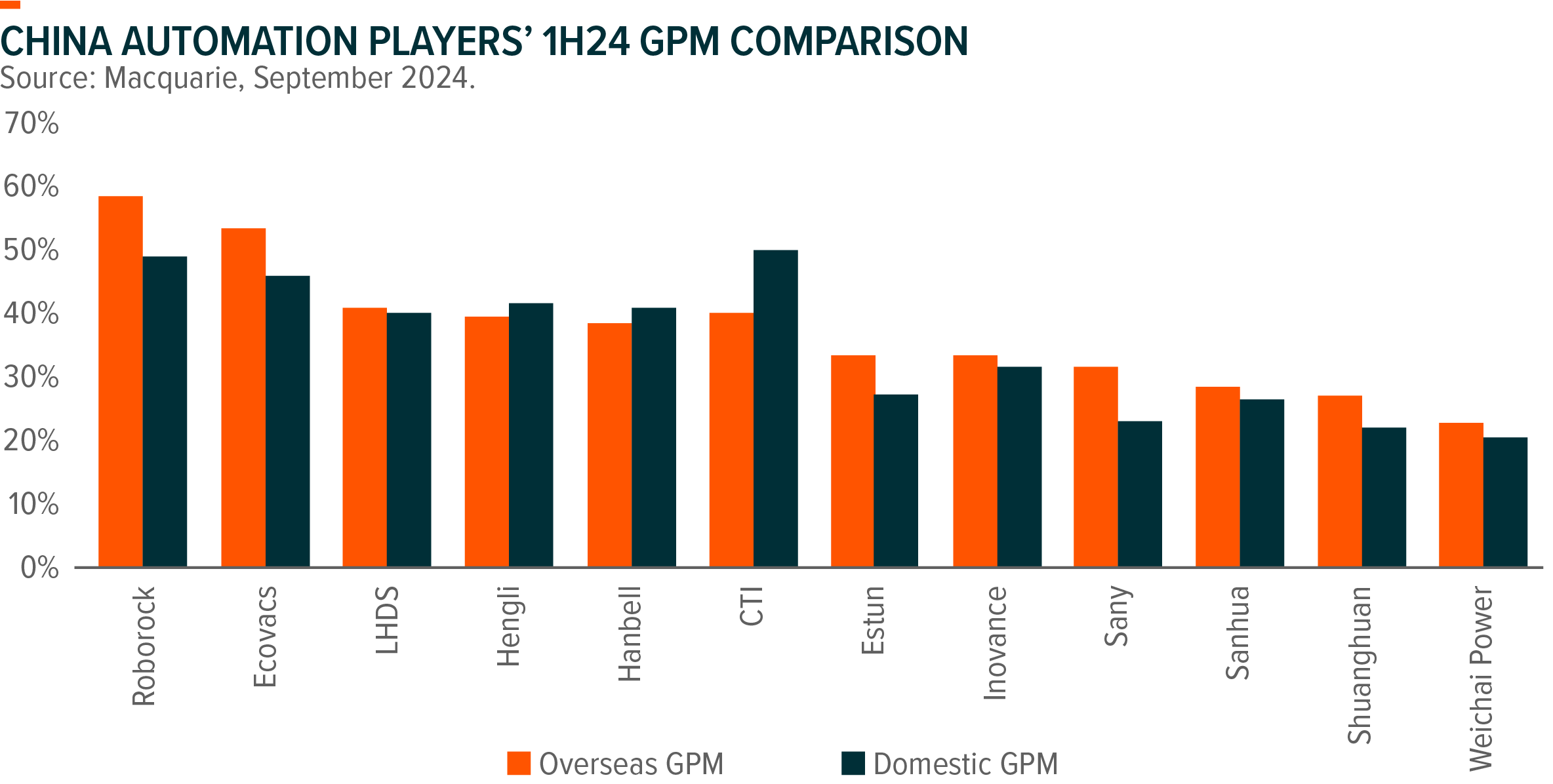

China factory automation demand remained sluggish and pricing pressure persists. The processing industry saw more resilient demand than the OEM market. Leading companies are able to maintain their top line relatively better than industry average by gaining market share but margins declined due to prices cut in 2Q24 results. Similarly, industrial robotics suffered from weak demand and fierce price competition. The top Chinese players also witnessed revenue growth under pressure or sharp margin contraction. Feedback from the industry experts showed no improvement in demand in July and August and the situation will likely persist in 2H24.

Stock Comments

- NARI Technology Co., Ltd. Class A: The company delivered stable strong Q2 results recently. They are also one of the key beneficiaries from UHV power grid capex in China in 2023-2026E.

- SUPCON Technology Co., Ltd. Class A: The company delivered a strong Q2 result. During the period, Supcon expanded into some new segments such as hydrogen production from wind and solar power, smart laboratories, smart coal mines and industrial parks, to seize more growth opportunities.

- Zhongji Innolight Co., Ltd. Class A: The company delivered solid Q2 results actually, with revenue up by 175%yoy and net profits up by 271%yoy. Management reiterated a strong demand outlook for 2H24, as they will continue to expand capacity to meet the downstream demand. The stock may be negatively impacted by the US tech correction.

Preview

We remain positive on the long-term trend of China industrial automation market growth. Domestic manufacturers continue gaining market share on the back of customized products across emerging industries, fast delivery and advanced post-sale services, while foreign brands keep losing market share in China. However, in the near term, the drag from renewables and electric vehicles will last for the whole year of 2024, which cannot be fully offset by the demand growth in traditional industries. Additionally, it takes time to see the positive impact on demand pickup from the current stimulus policies on large-scale equipment replacement.

Global X China Cloud Computing ETF (2826 HK)

Industry Update

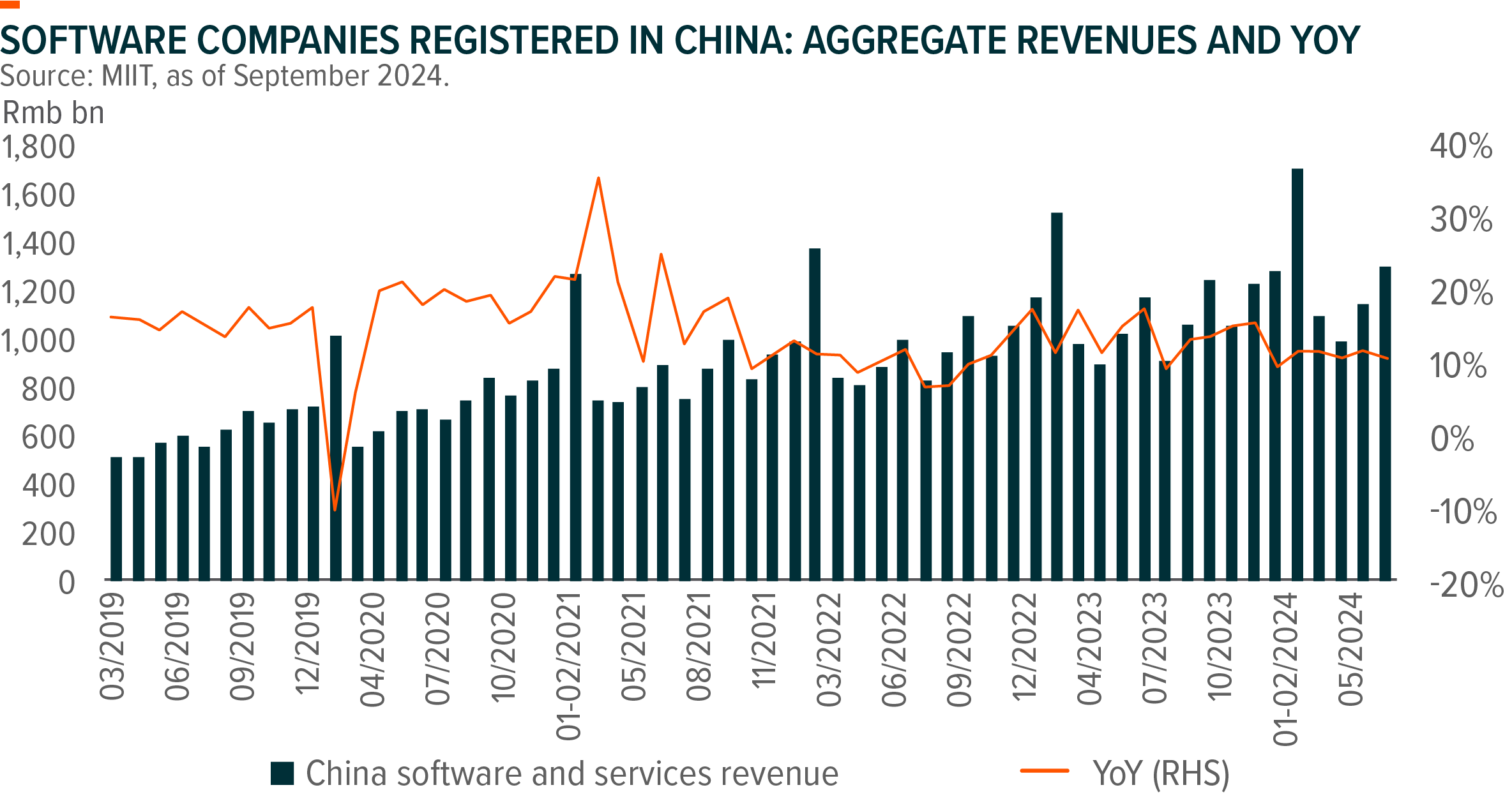

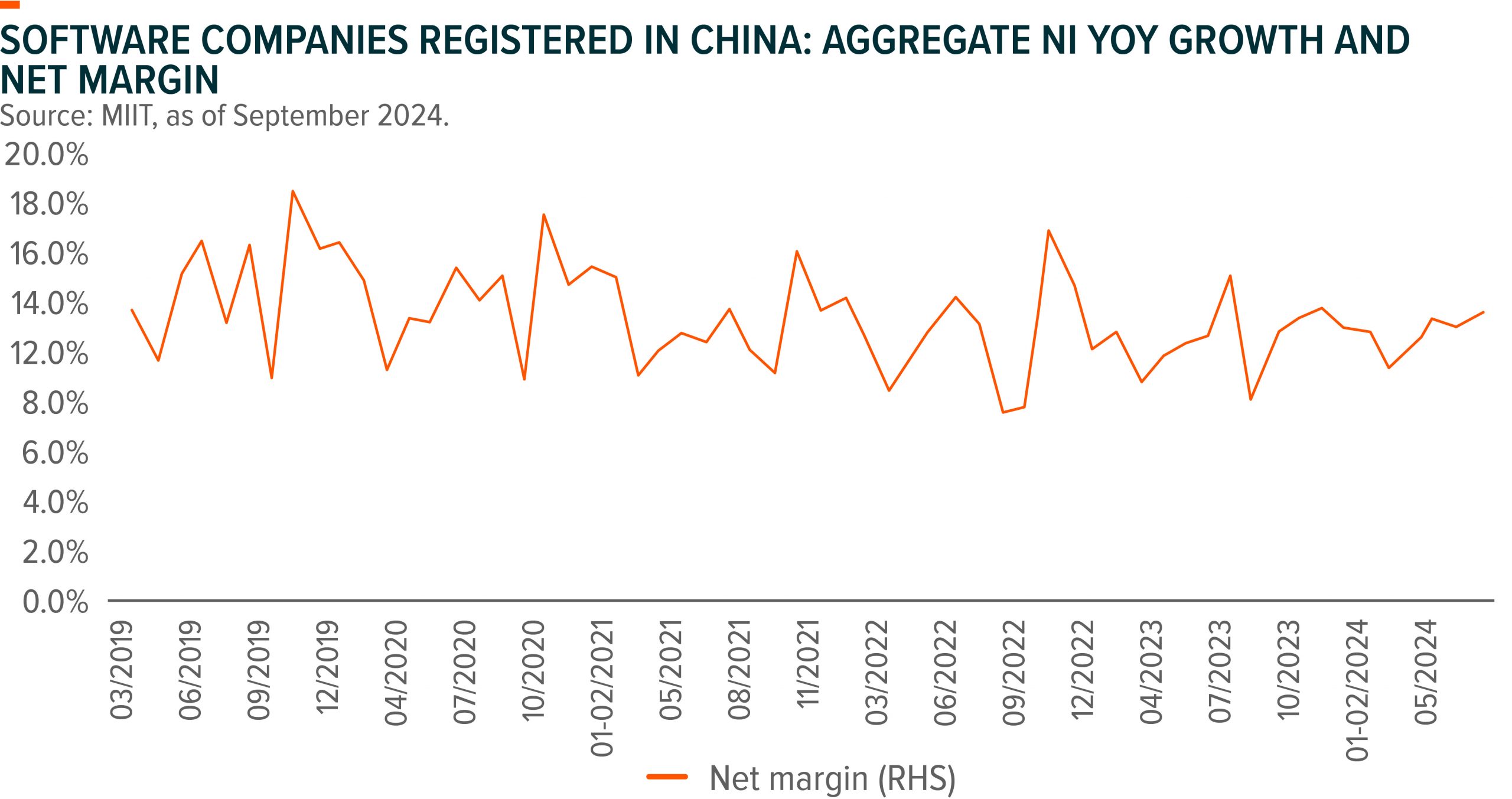

China software industry growth in July was weak at 9.4% YoY (vs. June at +10.9% YoY), further deteriorated from June, leading 7M24 revenues +11.2% YoY (vs. 7M23 at 13.5% YoY), due to weaker-than-expected client budgeting, and delay of certain large-scale SOE projects, especially slower software products and security software growth, while the profitability improvement continued, with net margin up to 12.7% in July (vs. 11.8% in 7M23) on slower headcount expansion and cost control.

For telecom industry, July industry revenue growth rebounded to 3.3% YoY (vs -0.2% YoY in Jun 24) helped by uptick in traditional business. Mobile decline narrowed to -1.3% YoY vs -4.2% YoY in Jun 24 and fixed service improved to 4.6% YoY vs 2.7% YoY in June 24. New business growth moderated slightly to 8.1% YoY.

Stock Comments

- Alibaba Group Holding Limited Sponsored ADR: Alibaba’s share price performance remained solid for this month, mostly driven by market anticipation of a potential inclusion in South Bound Connect. Companies’ eligibility for Stock Connect would be confirmed as of two trading days before the first Friday of September. In this year’s case that would be September 4 and September 6. If confirmed eligible, the Southbound inclusion should be completed after the close on Friday (September 6) and trading would start on the first trading day thereafter. if included, there could be potentially US$12bn inflow which is equivalent to ~6% of market cap. (according to Morgan Stanley Research)

- Tencent Holdings Ltd.: Stock price was relatively resilient vs. other index names attributable to Tencent’s strong fundamentals. Online game rev. growth accelerated for 1H24 in both domestic and overseas market driven by release of DnF Mobile and revived popularity of existing games.

- iflytek Co., Ltd. Class A: The Company posted 1H24 preliminary results with both sales and bottom line missing consensus. Worsened profitability in 1H24 was mainly due to LLM investments, increasing bad debt provisions and less other income. Spark LLM v4.0 was launched end June-24, with eight areas said to beat GPT-4 Turbo, according to the management.

- Netease Inc Sponsored ADR: 2Q results were a slight miss on revenue/earnings. Cash revenue and deferred revenue -13% QoQ respectively (ex-Youdao and Music basis) due to adjustments to FWJ PC on May 21 and Eggy Party in April. Market remained concerned on 3Q as the impact of FWJ PC will only see full-quarter impact.

Preview

China software industry’s growth remained subdued with no meaningful inflection seen in growth, due to the late cycle nature. Companies have been adapting cost control measures to reduce operating deleverage. AI LLMs continue to iterate with new feature/upgrades but monetization progress remains slow.

Global X China Little Giant ETF (2815 HK)

Industry Update

Bochu and APT Medical are among the key contributors for little giant this month.

Bochu:

2Q24 results were in line. We continued to see gross margin expansion on increasing high-power contribution while we expect robust overseas growth to continue;

Smart welding business has been expanding to more verticals; we see substantial domestic substitution potential given smooth progress in 1H24;

Tariff concern and domestic weakness are likely priced in.

APT:

Q24 results were in line: revenue grew by 25%, with net profit increasing by 31%;

We see stable growth in all segments: electrophysiology revenue rose by 28%, coronary revenue increased by 32%, and peripheral revenue surged by 40%. The company completed over 7,500 three-dimensional surgeries, doubling the number from the previous year;

We expect the approval of key electrophysiology products could significantly further boost revenue starting in 2025.