Important Information

Investors should not base investment decisions on this content alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X Japan Global Leaders ETF (the “Fund”) seeks to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the FactSet Japan Global Leaders Index (the “Index”).

- The Fund is subject to general investment risk, equity market risk, new index risk, annual reconstitution risk, differences in dealing arrangements between Listed Class of Units and Unlisted Classes of Units risk, differences in cost mechanisms between Listed Class of Units and Unlisted Classes of Units risk, currency risk, risk of reliance on the Index Calculation Agent, trading difference risk, passive investment risk, tracking error risk, trading risk, termination risk, reliance on market maker risks and distributions out of or effectively out of capital risk.

- The Fund’s investments are concentrated in securities in Japan. The Fund’s value may be more volatile than that of a fund with a more diverse portfolio. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the Japanese market.

- The Japanese economy is heavily dependent on international trade and may be adversely affected by protectionist measures, competition from emerging economies, political tensions with its trading partners and their economic conditions, natural disasters and commodity prices. Further, the TSE or JASDAQ has the right to suspend trading in any security traded thereon. The Japanese government or the regulators in Japan may also implement policies that may affect the Japanese financial markets.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including product features and the risk factors. There is no guarantee of the repayment of the principal.

- Global X India Select Top 10 ETF’s (the “Fund”) underlying Index is a new index. The Underlying Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Underlying Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history. The Underlying Index is an equal weighted index whereby the Underlying Index constituents will have the same weighting at each rebalancing (but not between each rebalancing) regardless of its size or market capitalisation based on the methodology of the Underlying Index.

- The Fund is a FPI registered with the SEBI. The applicable laws, rules and guidelines on FPI impose limits on the ability of FPI to acquire shares in certain Indian issuers from time to time and are subject to change. This may also adversely affect the performance of the Fund. The FPI status of the Fund may be revoked by the SEBI under certain circumstances. In the event the Fund’s registration as a FPI is cancelled, revoked, terminated or not renewed, this would adversely impact the ability of the Fund to make further investments, or to hold and dispose of existing investment in Indian securities. The Fund may be required to liquidate all holdings in Indian securities acquired by the Fund as a FPI. Such liquidation may have to be undertaken at a substantial discount and the Fund may suffer significant/substantial losses.

- The Fund’s investments are concentrated in securities in India. The Fund’s value may be more volatile than that of a fund with a more diverse portfolio. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the Indian market.

- The Fund’s investments are concentrated in companies in various sectors and themes including communication services, information technology, financials, health care, consumer staples and consumer discretionary, industrials and energy. Fluctuations in the business for companies in these sectors or themes will have an adverse impact on the Net Asset Value of the Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may as a result suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- Global X K-pop and Culture ETF’s (the “Fund”)The Index is a new index. The Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history.

- The Fund is subject to concentration risk as a result of tracking the performance of a single geographical region or country (South Korea). The Fund may likely be more volatile than a broad-based fund, such as a global equity fund, as it is more susceptible to fluctuations in value of the Index resulting from adverse conditions in South Korea. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the South Korean market.

- The Fund’s investments are concentrated in companies in various industries and sectors including entertainment, communication services, internet, gaming, consumer staples, consumer discretionary as well as food. The business performance of these industries or sectors are subject to a wide range of risks. Fluctuations in the business for companies in these industries or sectors will have an adverse impact on the Net Asset Value of the Fund.

- The Fund may invest in small and/or mid-capitalisation companies. The stock of small-capitalisation and mid-capitalisation companies may have lower liquidity and their prices are more volatile to adverse economic developments than those of larger capitalisation companies in general.

- The borrower may fail to return the securities in a timely manner or at all. The Fund may as a result suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests. As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund.

- Global X Innovative Bluechip Top 10 ETF (the “Fund’s”) seeks to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Mirae Asset Global Innovative Bluechip Top 10 Index (the “Index”).

- The Fund is subject to general investment risk, equity market risk, new index risk, equal weighted index risk, risks related to companies with technology themes, differences in dealing arrangements between Listed Class of Units and Unlisted Classes of Units risks, differences in cost mechanisms between Listed Class of Units and Unlisted Classes of Units risk, currency risk, trading difference risk, risks associated with ADRs, passive investment risk, tracking error risk, trading risk, termination risk, reliance on market maker risks, reliance of the same group risk and distributions out of or effectively out of capital risk.

- The Fund’s investments are concentrated in companies in the technology sector. The Fund’s value may be more volatile than that of a fund with a more diverse portfolio. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the technology sector.

- The number of constituents of the Index is fixed at 10. The Fund by tracking the Index may have a more concentrated investment portfolio than it would have held if tracking an index with a higher number of constituents, leading to higher risks of volatility.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including product features and the risk factors. There is no guarantee of the repayment of the principal.

- Global X AI & Innovative Technology Active ETF (the “Fund”)’s investment objective is to achieve long term capital growth by primarily investing in equities of exchange-listed companies globally, which fall within the investment theme of artificial intelligence (“AI”) and innovative technologies.

- The Fund will invest primarily (i.e. at least 70% of its net asset value (the “Net Asset Value”)) in equity securities and equity-related securities (such as common shares, preferred stock as well as American depositary receipts (“ADRs”), global depositary receipts (“GDRs”) and participation notes) of companies which (i) create, design and develop, or (ii) benefit from the advancement of, AI and Innovative Technologies Companies. Risk associated with AI and Innovative Technologies Companies include Operational and business risk, Changes in technology risk, Governmental intervention risk, Regulatory risk, Intellectual property risk, Significant capital investment risk, Cyberattack risk.

- The performance of the Fund may be exposed to risks associated with different sectors including but not limited to industrial, consumer discretionary, financial services, information technology, semiconductor, communication services, entertainment and healthcare. Fluctuations in the business for companies in these sectors will have an adverse impact on the Net Asset Value of the Fund.

- The Fund employs an actively managed investment strategy. The Fund does not seek to track any index or benchmark, and there is no replication or representative sampling conducted by the Manager. It may fail to meet its objective as a result of the Manager’s selection of investments, and/or the implementation of processes which may cause the Fund to underperform as compared to other index tracking funds with a similar objective.

- The Fund’s investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- There is no industry sector requirement and the Fund may from time to time concentrate in a particular sector. The performance of the Fund may be exposed to risks associated with different sectors and themes, including but not limited to industrial, consumer discretionary, financial services including fintech, information technology, semiconductor, communication services, entertainment, and healthcare. The Fund may experience relatively higher volatility in price performance when compared to other economic sectors.

- Securities lending transactions may involve the risk that the borrower may fail to return the securities lent out in a timely manner or at all. The Fund may as a result suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- Investors should note that Unitholders will only receive distributions in USD and not HKD. In the event the relevant Unitholder has no USD account, the Unitholder may have to bear the fees and charges associated with the conversion of such distribution from USD into HKD or any other currency.

- Payments of distributions out of capital and/or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions involving payment of dividends out of capital or effectively out of capital of the Fund may result in an immediate reduction in the Net Asset Value per Unit of the Fund and will reduce the capital available for future investment.

- The trading price of the Listed Class of Units on the SEHK is driven by market factors such as the demand for and supply of the Listed Class of Units. Therefore, the Listed Class of Units may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- The Fund may invest in financial derivative instruments (“FDIs”) for non-hedging (i.e. investment) and/or hedging purposes, in order to achieve efficient portfolio management. Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Fund.

- Global X Electric Vehicle and Battery Active ETF (the “Fund”) invests in equity to achieve long term capital growth by primarily investing in companies which are directly or indirectly involved in electric vehicle or electric vehicle-related battery businesses.

- The Fund employs an actively managed investment strategy and does not seek to track any index or benchmark. It may fail to meet its objective as a result of the Manager’s selection of investments, and/or the implementation of processes which may cause the Fund to underperform as compared to other index tracking funds with a similar objective.

- The Fund’s investments are concentrated in companies involved in the EV/Battery Business, which may experience relatively higher volatility in price performance when compared to other economic sectors. The value of the Fund may be more volatile than that of a fund having a more diverse portfolio of investments and may be more susceptible to adverse economic, political, policy, liquidity, tax, legal or regulatory event affecting the relevant sector.

- Electric vehicle companies and electric vehicle-related battery companies invest heavily in research and development which may not necessarily lead to commercially successful products. In addition, the prospects of electric vehicle companies and electric vehicle-related battery companies may be significantly impacted by technological changes, changing government regulations and intense competition from competitors.

- Investors should note that Unitholders will only receive distributions in USD and not HKD. In the event the relevant Unitholder has no USD account, the Unitholder may have to bear the fees and charges associated with the conversion of such distribution from USD into HKD or any other currency.

- Dividends may be paid from capital or effectively out of capital of the Fund, which may amount to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment and result in an immediate reduction in the Net Asset Value per Unit of the Fund.

- The trading price of the Fund unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

Monthly Commentary

Global Thematic ETFs – Jan 2025

Global X India Select Top 10 ETF (3184 HK)

Market Update

The MSCI India Index was down 2.85% (in USD terms) over the December reporting period underperforming the MSCI APxJ/EM Indices due to concerns on global macro uncertainties, weak Indian rupee, and domestic growth concerns. That said, for the full year CY24, the MSCI India Index ended +12.41% (in USD terms) outperforming the APxJ/EM region for the fourth consecutive year.

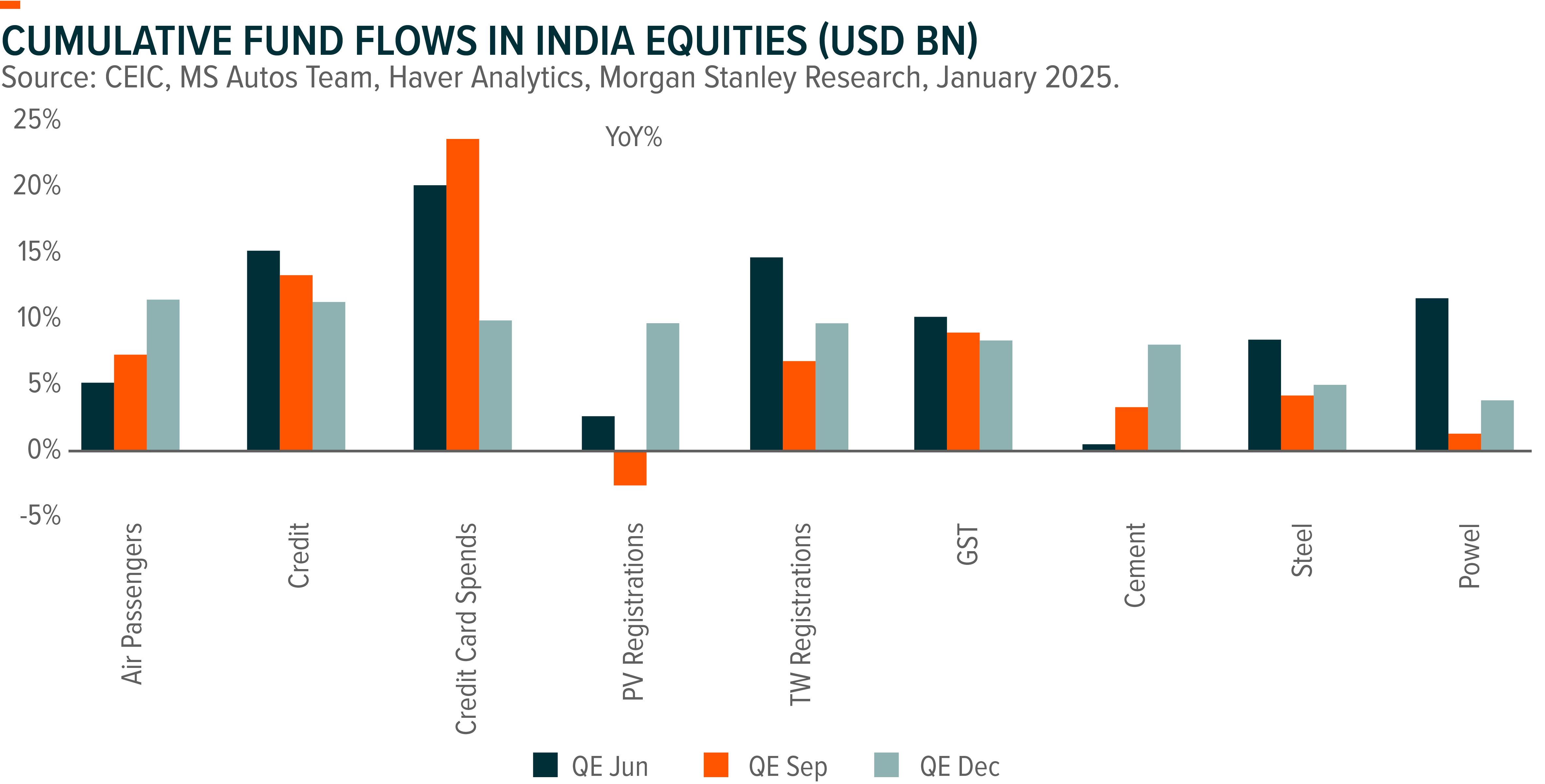

- Domestic demand-based high-frequency data for December showed an improving trend, yet the pace of recovery has been slower than anticipated. While PMI for manufacturing softened to a 12 month-low of 56.4, services PMI rose to a 4-month high of 59.3 in December. Power demand also rose to a five-month high of 5.9% and credit card spending stood at a 3-month high with average daily spending growing 13.5%yoy. Naukri job index picked up with recovery in hiring activity across the board. That said, the pace of pickup in government capex has been slower at average of 3.7% in Oct-Nov and a lagged impact of tighter monetary policy led to a slower growth recovery pace for this quarter.

- November CPI softened to 5.5% with steady Core CPI (ex food, fuel) at 3.7%yoy. Food inflation remained high but it is expected to moderate in coming months with an improved outlook for summer and winter crops. Also, core inflation has been trending down in the past 12 months thus this may give a room for the RBI to start an easing cycle from 1QCY25 onwards.

- Indian equity flows from foreign institutional investors ended with a net buying of USD 1.9 billion (vs. net selling of USD 2.7 billion in November) and ended CY2024 flows with flattish at USD -0.1bn, while domestic institutional investors maintained their buying trend for the 17th consecutive month by net buying USD 4.0 billion in December (vs. USD + 5.3 billion in November).

Stock Comments

- Sun Pharmaceutical (SUNP IN) and Infosys (INFO IN) were the major contributor in December as pharmaceutical and IT services outperformed the market post the US election as the companies in these two sectors are exporters who can benefit from strong US dollars and also considered as defensive sectors amid macro uncertainties and domestic growth concerns. IT services is expected to benefit from strong US economy next year and the latest Naukri job index also showed recovery hiring trend for the sector.

- Hindustan Unilever (HUVR IN) was the major detractor in December due to concerns on mass market consumption growth as one of its peers, Godrej Consumer, reported profit warning for 3QFY25E. Rising raw material prices also increased concerns on margins for staples companies including Hindustan Unilever. Moreover, a robust growth of quick commerce channel increased competition for traditional FMCG companies as this reduced big FMCG companies’ distribution moat in traditional channel and this concern has continued to weigh down on stock performance.

Preview

This confluence of strong GDP growth, moderate inflation, and recovery in consumption suggests a buoyant outlook for the Indian equity markets, and we believe these conditions will be conducive to capitalizing on potential growth opportunities during this fiscal year in India. We remain constructive on India market.

Global X K-pop and Culture ETF (3158 HK)

Market Update

December was particularly eventful for Korea market, with President Yoon declaring martial law early in the month and subsequently being impeached by the Assembly. KOSPI declined 9.6% during 2024, ending at 2,399. Political uncertainties are expected to be resolved in the next six months, with a likely early presidential election in mid-2025. The lack of visibility may hinder corporate decision-making in early 2025. Additionally, Korean won has depreciated by 14% throughout 2024 and is expected to weaken further due to the policy rate differential, ongoing investments in the US and the potential trade war.

Sector-wise, the entertainment sector (our product’s top holding sector) has experienced a challenging month post previous strong rally, with four leading players – HYBE, YG, SM and JYP – recording 1%, 4%, 9% and 8% loss in December, respectively. We reckon short-term volatility under recent political uncertainties and social events. However, we remain optimistic about the sector’s 2025 outlook, driven by top artists’ comeback (namely Blackpink and BTS), China rebound, low base, improved monetization as well as the industry’s resilience to potential tariff hike post Trump’s re-election.

Stock Comments

- Samyang Foods (003230 KS): Samyang recorded 47% return in December thanks to its success in exports, while domestic competitors are facing challenges in achieving growth due to the structural decline in domestic consumption influenced by demographic changes. The completion of the second plant in Miryang, which will increase production capacity by 39% by the end of May 2025, along with a new plant in China expected to enhance capacity by 32% by the end of January 2027, is poised to support top-line growth in both the short and long term.

- Cosmax (192820 KS): Cosmax recorded 12% return in December. As a leading global player in cosmetic ODM, Cosmax is experiencing strong top-line growth and margin expansion from the K-Beauty boom in the global market. Additionally, Cosmax has the highest exposure to foreign brands and stands to gain the most from the increasing reliance of global and western indie brands on ODMs. The decline in China market used to be a major concern for Cosmax’ earnings. However, the company’s exposure to China will be almost none since 2024 and the impact from China will be much less significant since 2025.

- CJ ENM (035760 KS): CJ ENM experienced 17% loss in December. The media business is experiencing improvement from a low base, yet losses persist in the movie/drama divisions. TVING has recorded flat growth in 2024. We identify risks related to the baseball off-season and heightened competition and concern about long-term growth for both television and OTT.

Preview

Although facing short term fluctuations such as political uncertainties, we maintain positive on the rise of K-Pop and cultural phenomenon in global market. Recent hit track APT by Rose and Bruno Mars, along with Han Kang’s Nobel Prize win in Literature, have significantly raised global awareness of K-pop culture. We expect it to continuously provide a halo effect towards Korean goods such as cosmetics and packaged food. We also believe that price competitiveness and compelling value propositions stand out as key factors driving the strong export of Korean consumer goods in the global market, especially under current economic uncertainties and consumer downtrading trend.

Global X Innovative Bluechip Top 10 ETF (3422 HK)

Google launched Gemini 2.0

Google has launched Gemini 2.0, a significant upgrade to its AI capabilities, designed to enhance user assistance through advanced multimodal features, including the ability to generate images and audio, and perform tasks autonomously.

The updates emphasize the development of agentic models that can understand user contexts and take actions under supervision. This aligns with Google’s vision of creating a universal AI assistant capable of managing complex tasks and providing real-time responses.

Google plans to expand Gemini 2.0’s availability in early 2025, aiming to integrate these advancements across its products and enhance user experiences through improved AI interactions .(Company data, the verge)

Amazon Re: Invest 2024

Amazon Web Services (AWS) announced several new high-profile partnerships and product launches on its re:Invest 2024 conference, further solidifying its position as a leader in the cloud computing industry. These developments boosted investor confidence and contributed to the stock’s upward momentum. Key announcements included the launch of Amazon Nova, a new generation of foundation models, and several high-profile partnerships. The event featured five keynotes and 18 innovation talks, with AWS leaders discussing the latest in AI, machine learning, and cloud computing. Attendees engaged in hands-on activities, demos, and immersive experiences, such as racing autonomous cars and exploring AI-powered art installations. The event also highlighted AWS’s commitment to sustainability and strategic investments in AI and cloud infrastructure. (Company data).

Global X Japan Global Leaders 10 ETF (3150 HK)

Industry Update

In December 2024, the FactSet Japan Global Leaders Index recorded +7% gains in JPY terms1. Central bank rates decision remains the key focus. BOJ leaves policy rate unchanged in December, while US Fed cut rates by 25bps as expected. However, December FOMC Dot Plot indicated only 2 rate cuts in 2025, down from 4 cuts in previous forecast. JPY depreciated by 4.5% throughout the month as a result of the more hawkish stance by US Fed. USDJPY ended December at 157, from 150 as of end November.2

Stock Comments

Toyota recorded 23% gain in December, a key contributor to the ETF. In December, Nikkei reported that Toyota management has set an ambitious ROE target of 20%, to be achieved by 2030. Company is also seeking to reform its business model, provide better aftersale services, and bolster shareholder returns. In addition, media report pointed out that the firm plans for Jan-Mar output of 2,450k units (+7% YoY), which could imply recovery in output.

Sony recorded 12% gain in December, a key contributor to the ETF. On 19 Dec, Sony announced that it has entered into a capital and business alliance agreement with Kadokawa. Sony will acquire another 12mn common share, making it the largest shareholder of Kadokawa with 10% of share. This acquisition will enhance further collaboration around joint production of anime titles and increased publishing of games. The strong gaming pipeline in 2025 should support revenue and OP growth for Sony’s Games business.

Preview

Japan stock market went through massive volatility over past few months under concern for JPY volatility and US economy recession. While short term outlook remains uncertain given slowing global economy and political events uncertainty, we remain constructive over Japan stock market in the long term, as supported by a combination of robust export growth, recovering domestic demand, and ongoing corporate reform. JPY appreciation is a key market concern as it could weigh on Japanese corporate earnings, but gradual appreciation should be manageable for global investors as it is also positive for dollar-denominated returns (without currency hedging).3

Global X AI & Innovative Technology Active ETF (3006 HK)

Industry Update

Google launched Gemini 2.0

Google has launched Gemini 2.0, a significant upgrade to its AI capabilities, designed to enhance user assistance through advanced multimodal features, including the ability to generate images and audio, and perform tasks autonomously.

The updates emphasize the development of agentic models that can understand user contexts and take actions under supervision. This aligns with Google’s vision of creating a universal AI assistant capable of managing complex tasks and providing real-time responses.

Google plans to expand Gemini 2.0’s availability in early 2025, aiming to integrate these advancements across its products and enhance user experiences through improved AI interactions.(Company data, the verge)

OpenAI announces new o3 models

o3 is the successor to the earlier o1 model and includes a smaller variant called o3-mini. Unlike standard AI models, o3 incorporates a self-fact-checking mechanism that enhances its reliability in complex domains like physics and mathematics, albeit with increased response times. Users can adjust the reasoning time for better performance. OpenAI is currently conducting safety tests and red teaming for o3, with plans to release a preview of o3-mini by the end of January 2025. (TechCrunch)

Stock Comments

Alphabet + 11.07% : The introduction of Gemini 2.0, Alphabet’s most advanced AI model yet, significantly boosted investor confidence. This new model features enhanced multimodal capabilities, including native image and audio output, and improved performance with lower latency. Additionally, the launch included exciting new features like Deep Research, which acts as a research assistant, and experimental projects such as Project Mariner and Jules. Overall, the successful launch of Gemini 2.0 and its promising applications across various Google products played a crucial role in driving Alphabet’s stock performance this month.

Amazon +5.53%: Amazon Web Services (AWS) announced several new high-profile partnerships and product launches on its re:Invest 2024 conference, further solidifying its position as a leader in the cloud computing industry. These developments boosted investor confidence and contributed to the stock’s upward momentum.

Preview

The Global X AI and Innovative Technology Active ETF Fund is committed to being at the forefront of AI investment, leveraging our expertise to identify and capitalize on opportunities across the AI value chain. By focusing on both established leaders and emerging innovators, we aim to provide our investors exposure to one of the most dynamic and impactful sectors of the global economy. As the AI landscape continues to evolve, we remain dedicated to adapting our strategy to ensure that our investors benefit from the full spectrum of AI-driven growth and innovation.

Global X Electric Vehicle and Battery Active ETF (3139 HK)

Industry Update

China electric vehicle sales were further accelerating in December 2024, driven by the mild promotions from automakers and the pre-purchase behavior before the trade-in program exit by the year end. CPCA expects 2025 national old-for-new subsidy likely to come out recently and be implemented from early-2025. As a matter of fact, we have witnessed some provinces of China announced to extend the subsidy program in 2025 to continuously boost the EV sales as well local economy.

Regarding the battery production and sales, utilization remained high despite the low season. Channel checks implied the leading battery makers, especially Top 2 Chinese battery makers, are maintaining a full utilization rate largely owing to their positive demand outlook and advanced production for the upcoming peak season in March. Consequently, battery materials and the upstream mining companies’ utilization are also significantly improved. Some subsectors who suffered from loss-making in the last two years are discussing to raise prices, e.g. cathode, anode and lithium carbonate.

Stock Comments

Tesla INC: Tesla INC: Company delivered solid quarterly results and unveiled their self-driving robotaxi. The stock also benefits from positive sentiment after Trump comes into power.

Albemarle Corporation: Lithium carbonate prices came down to Rmb70k-75k/t. The company’s stock price largely moved along with lithium carbonate prices.

Preview

Looking ahead to 2025, we expect China xEV sales around 15mn units, +40%yoy, Europe +5%yoy to 4.56mn units, US flat yoy at 1.57mn units and other markets of 0.74mn units. We have seen some China provinces extended the EV replacement subsidies to boost EV sales as well as the economy. We expect ESS battery may still see 30%+ fast growing next year, driven by more energy storage used per Wh in renewables projects and mild renewables installation growth globally. We believe, battery business success relies on EV partnership in the long run. CATL, BYD and LGES are relatively better positioning at the moment. Competition amongst the second-tier Chinese battery makers (EVE, CALB, Gotion, Sunwoda) and SDI could be intensified to win orders from leading EV makers from a long-term strategic perspective, but the worst time on ASP and margins are behind.