Important Information

Investors should not base investment decisions on this content alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X China Electric Vehicle and Battery ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Electric vehicle companies invest heavily in research and development which may not necessarily lead to commercially successful products. In addition, the prospects of Electric vehicle companies may significantly be impacted by technological changes, changing governmental regulations and intense competition from competitors.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X Hang Seng TECH ETF (the “Fund”) seeks to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Hang Seng TECH Index (the “Index”).

- The Fund’s investments are concentrated in companies with a technology theme. Technology companies are often characterised by relatively higher volatility in price performance. Companies in the technology sector also face intense competition, and there may also be substantial government intervention, which may have an adverse effect on profit margins. These companies are also subject to the risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences.

- The Fund’s investments are concentrated in securities listed on the Stock Exchange of Hong Kong (the “SEHK”) of companies that are active in technology sector may result in greater volatility in the value of the Fund than more diverse portfolios which comprise broad-based global investments. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the technology sector.

- The Index is subject to concentration risk as a result of tracking the performance of securities incorporated in, or with majority of revenue derived from, or with a principal place of business in, the Greater China region. The Fund’s NAV is therefore likely to be more volatile than a broad-based fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- The trading price of the Fund unit (the “Unit”) on the SEHK is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- Dividends may be paid from capital or effectively out of capital of the Fund, which may amount to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment and result in an immediate reduction in the Net Asset Value per Unit of the Fund.

- Global X China Clean Energy ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Many clean energy companies are involved in the development and commercialization of new technologies, which may be subject to delays resulting from budget constraints and technological difficulties. Obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants and general economic conditions also significantly affect the clean energy sector.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Consumer Brand ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- The performance of companies in the consumer sector are correlated to the growth rate of the global market, individual income levels and their impact on levels of domestic consumer spending in the global markets, which in turn depend on the worldwide economic conditions, which have recently deteriorated significantly in many countries and regions and may remain depressed for the foreseeable future.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Robotics and AI ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Robotics and artificial intelligence sector is sensitive to risks including small or limited markets for such securities, changes in business cycles, world economic growth, technological progress, rapid obsolescence, and government regulation. These companies rely on significant spending on research and development and tend to be more volatile than securities of companies that do not rely heavily on technology.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Semiconductor ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Semiconductor industry may be affected by particular economic or market events, such as domestic and international competition pressures, rapid obsolescence of products, the economic performance of the customers of semiconductor companies and capital equipment expenditures. These companies rely on significant spending on research and development that may cause the value of securities of all companies within this sector of the market to deteriorate.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Little Giant ETF’s (the “Fund’s”) objective is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive China Little Giant Index (the “Index”).

- The Index is a new index. The Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history.

- The Fund may invest in small and/or mid-capitalisation companies which may have lower liquidity and their prices are more volatile to adverse economic developments than those of larger capitalisation companies in general.

- The Fund’s investments are concentrated in companies which are characterised by relatively higher volatility in price performance. The Sub-Fund may be exposed to risks associated with different sectors and themes including semiconductor, industrial, pharmaceutical, energy and technology. Fluctuations in the business for companies in these sectors or themes will have an adverse impact on the net asset value of the Sub-Fund.

- Some of the companies classified as the Little Giants have a relatively short operating history. Such companies also face intense competition and rapid changes could render the products and services offered by these companies obsolete, which may have an adverse effect on profit margins.

- They may be more susceptible to risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences affecting those companies.

- The Mainland China is an emerging market. The Fund invests in Mainland Chinese companies which

- may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risk, currency risks or control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk and the likelihood of a high degree of volatility.

- Securities exchanges in the Mainland Chinese markets typically have the right to suspend or limit trading in any security traded on the relevant exchange. The government or the regulators may also implement policies that may affect the financial markets. All these may have a negative impact on the Fund.

- Listed companies on the ChiNext market and/or STAR Board are subject to higher fluctuation on stock prices and liquidity risk, over-valuation risk, less stringent regulation risk, delisting risk and concentration risk.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Fund.

- The trading price of the Shares on the SEHK is driven by market factors such as the demand and supply of the Shares. Therefore, the Shares may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Share of the Fund and will reduce the capital available for future investment.

- Global X China Cloud Computing ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Companies in the internet sector may face unpredictable changes in growth rates and competition for the services of qualified personnel. The products and services offered by internet companies generally incorporate complex software, which may contain errors, bugs or vulnerabilities.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

Monthly Commentary

China Thematic ETFs – Nov 2024

Global X China Electric Vehicle and Battery ETF (2845 HK)

Industry Update

- Strong October EV Sales; NEV penetration reached 54%: According to CPCA estimates, October NEV wholesale volume reached 1.4mn, +58% YoY1, as driven by supportive trade-in policies. Major EV Brands delivered solid October sales. BYD reported record-high monthly NEV PV sales of 500.5k units, +66% YoY, with PHEV continuing to record strong growth. Overseas sales grew by 2% MoM to 31k.2 Li Auto delivered 51k units in October, +27% YoY. Nio (+30% YoY) and Xpeng (+16% YoY) also recorded steady sales momentum in October. Xiaomi SU7 delivery exceeded 20k units in October. Xiaomi also launched SU7 Ultra, priced at Rmb814.9k (~US$114k), with over new order of 3,680 units within the first 10 mins of launch. (for reference only, abovementioned stocks are not necessarily in the constituent list of the ETF). Based on insurance registration, new energy vehicle (NEV) penetration was 54% in the last week of October.3

- Over 1.5mn applications for Auto trade-in program: The trade-in stimulus has been doubled to Rmb20k (from Rmb10k) per NEV, and Rmb15k (from Rmb7k) per eligible ICEV,4 following central government’s indication that long-term government bonds could be used to fund consumer goods trade-in.5 As of 24 October, the Ministry of Commerce trade-in information platform has received 1.57mn applications for the auto trade-in subsidy program.

- Tariff: In October, European Commission announced a new draft decision on final countervailing duties on BEV imports from China, which are marginally lower than those disclosed in early July. Notably, tariff on China-made Tesla would be cut to 9% from previously planned 20.8% (on top of the 10% existing tariff). In addition, Canada says it will impose a 100% tariff on imports of China-made EVs.6

- Battery material costs stabilized after substantial decline: China’s Battery grade lithium carbonate price was Rmb74.4k/ton as of end-October, +0.7% wow, -49%/-28%/-31%/-9% vs. average of 4Q23/1Q24/2Q24/3Q247. Battery materials prices have decreased by over 80% from its peak in 2022, supporting the continued cost optimization for battery makers and EV manufacturers.

Stock Comments

- Following a 23% gain in September, BYD recorded -4.6% loss in October, a negative contributor to the ETF. BYD reported solid 3Q24 results on 30 October. 3Q24 revenue was Rmb201.1bn, +24.0% YoY and +14.2% QoQ. Notably, BYD’s quarterly revenue tops Tesla for the first time and becomes the largest EV company globally (in terms of quarterly sales). Group GPM was 21.9%, +3.2ppts QoQ, and GP per vehicle increased by 16.7% QoQ to Rmb35.6k. The strong profitability is bolstered by expanding unit sales and margin-enhancing DM-i 5.0 deliveries. BYD will continue to benefit from the solid PHEV opportunity both domestically and overseas. The solid new launch pipeline in 2025E should help BYD to maintain its dominant position in PHEV market.

- Following a 37% gain in September, CATL recorded -2.3% loss in October, roughly in line with ETF performance. CATL reported solid 3Q24 results on 18 Oct. Net profit of Rmb13bn was +26% YoY. Excluding the one-off asset impairment of Rmb4.7bn, CATL’s 3Q24 core earnings implied c.30% beat vs consensus. 3Q24 revenue of Rmb92bn declined by 12% YoY mainly due to the c.30% YoY decrease in battery prices. EV Battery Unit GP of c.Rmb200/kWh was higher than consensus estimates, driven by product mix premiumization and cost savings from manufacturing advantages. Management is seeing even better 4Q order momentum as compared to 3Q, which should support CATL to regain revenue growth in 4Q on the back of stabilizing battery prices.

Preview

We remain positive on the long term growth potential for EV and battery value chain, along with the upward EV penetration trajectory. Domestic old car replacement demand, as stimulated by scaled-up auto trade-in program, together with export sales, should support China’s resilient auto momentum and benefit leading domestic brands. We expect the China auto market to stay competitive in 2024 with strong new product line-up and technology innovations from leading EV and battery brands, and new entrants such as Xiaomi. Geopolitical tensions remain the key risks, but China EV models will still remain competitive under new tariff landscape thanks to its cost advantages. Localized production will be the longer term solution for Chinese brands.

Global X Hang Seng TECH ETF (2837 HK)

Industry Update

Following a significant rebound of 33% in September on the back of strong policy stimulus, Global X Hang Seng Tech ETF (2837 HK) recorded -5% return in October. We are seeing divergent performance across different sectors, with semiconductor names recorded solid returns while internet companies recorded substantial corrections. With a clear change in policymaker stance, the gradual rollout of stimulus policies could support a revived consumer sentiments that will benefit sectors including ecommerce, advertising, EV, and 3C electronics.

Stock Comments

- Xiaomi recorded 19% return in October, a key contributor to the ETF. Xiaomi launched a series products across its Human x Car xHome ecosystem, including the AI-powered HyperOS 2.0 upgrade, Xiaomi 15 series, SU7 Ultra as well as several portable/home AIoT products. Xiaomi’s flagship series Xiaomi 15/15 Pro pricing starts from Rmb4,499 and Rmb5,299 for 12GB+256GB, Rmb200/300 higher than prior models, with key specs upgrades in SoC, screen technology, fingerprint scanner and battery. SU7 Ultra’s presale price is set at Rmb815k and received 3.7k preorders within the first 10mins. Xiaomi SU7 delivery exceeded 20k in October, and is on track to reach company’s annual delivery target of 120k.

- SMIC recorded 30% return in October, a key contributor to the ETF. China foundries will continue to benefit from increasing demand for localized semis production, which long-term revenue expansion. On the back of reviving investor sentiments, SMIC went through valuation re-rating as supported by shipment recovery in smartphone and consumer related applications, which drives better UT rate. China’s foundries are on track to build more localized capacity to capture a larger share of the domestic demand, and leading domestic foundries will benefit from the increasing demand given the technology advancements in AI, electronics vehicles, and robotics

Preview

Hang Seng Technology Index constituents are well positioned to benefit from the policy stimulus by central government. We see unique positioning of Hang Seng Tech thanks to its attractive valuation, ongoing margin expansion, and continued ramp up in shareholder returns. With well-established ecosystem containing large user base and leading technology in place, we see further upside potential for these leading technology companies coming from the rapid development of structural growth themes such as EV, Semiconductor and AI in China.

Global X China Clean Energy ETF (2809 HK)

Industry Update

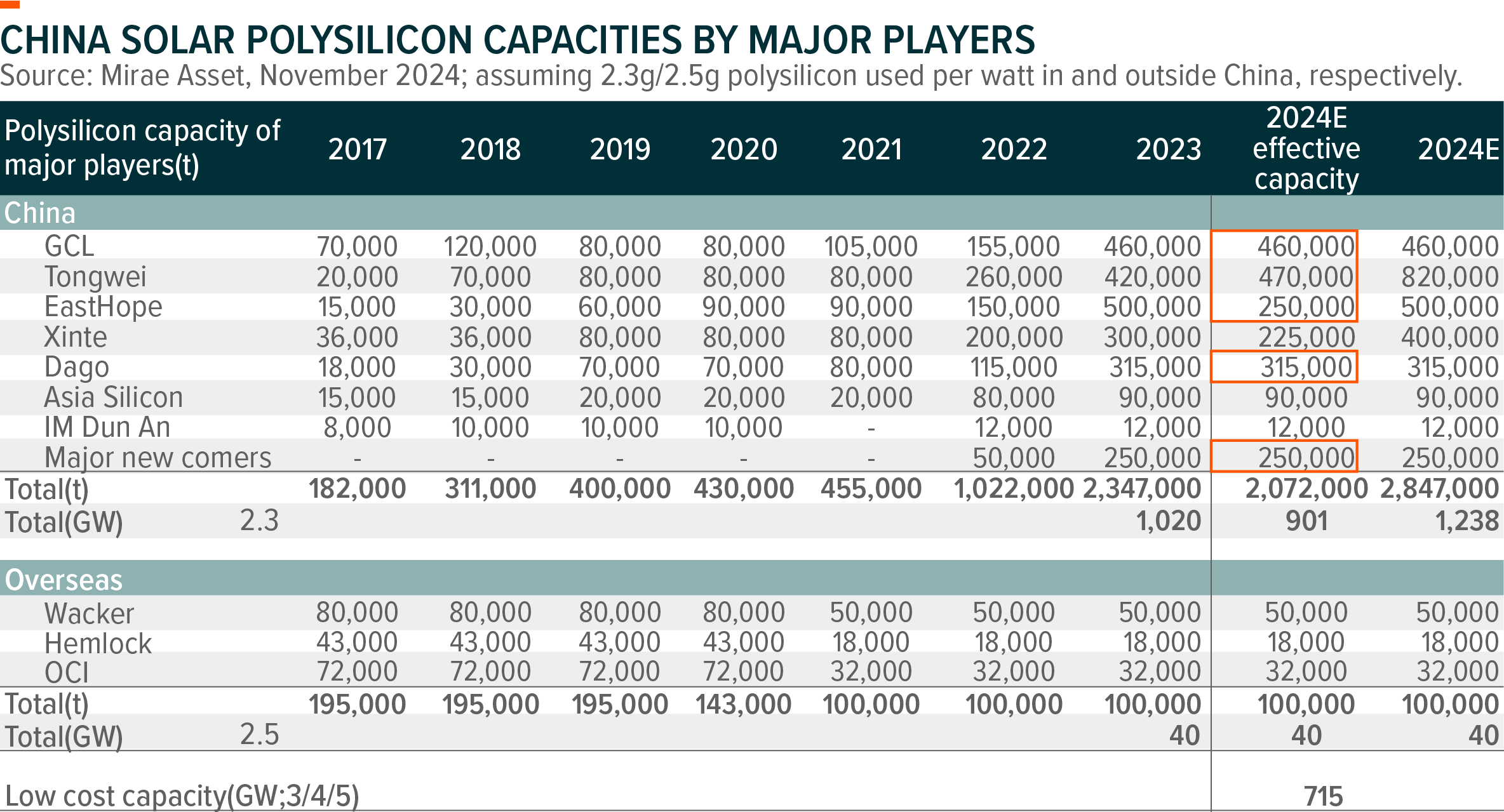

China solar installation picked up to +32%yoy in September, adding 20.9GW vs 16.5GW in August. In 9M24, the total solar installation in China is 161GW, +24.8%yoy. Global solar demand outlook in 2025 remains resilient from channel feedback. New policies have been drafted by China Ministry of Industry and Information Technology to force the inefficient electricity-consumption capacities exit and push the consolidation/production cut from a top-down perspective. The latest quarterly results of the major solar companies also showed the loss narrowed down or even slightly positive earnings, which implies the worst time is behind although the oversupply and excessive competition issues would last for a while. Should global demand increase by extra 20~30%, we may see substantial fundamental changes in solar value chain.

China wind installation ended at 5.5GW in September vs 3.7GW in August, sending 9M24 accumulated wind installation to 39GW, +16.8%yoy. China’s grid infrastructure investment in September was slightly decelerating to Rmb65bn, +12%yoy. Power grid capex is strong as expected to better utilize the renewables generation in the near future.

Stock Comments

- LONGi Green Energy Technology: The leading solar wafer makers slightly increased wafer selling prices recently, implying positive signals on wafer S/D balance. Additionally, China’s recent stimulus policies and solar manufacturing production cut plan also helps with high beta play like Longi.

- TCL Technology Group: Similarly as Longi, TCL benefits from marginally wafer prices hike, as well as China’s stimulus policies and solar manufacturing production cut plan.

- Sungrow Power Supply: The company has relatively larger ESS exposure to the US market which is beneath the overhang of Trump tariff on China imported products. In fact, company delivered solid 3Q24 earning results.

Preview

We were happy to see marginal fundamental improvements in renewables sector in the 3Q24 results, who have been suffering from over capacities for a long time. For example, the renewables sectors have made great efforts in cost cutting to make renewable power more and more cost competitive globally, exporting to every corner in the earth and digesting the huge amount of capacities.

We have been constructive on the global clean energy growth and the trend of energy transition, just worried about the near-term broad mismatch between supply and demand. We believe, it still needs time to get out of the woods, but winter is behind.

Global X China Consumer Brand ETF (2806 HKD)

Industry Update

With ongoing policy support in consumer over the past few months, consumer sentiment in China has shown improvement. Sep 24 total retail sales growth was up 3.2% YoY (vs +2.1% YoY in Aug 24), beat BBG consensus of 2.5% YoY. Retail and consumer sector data during the National Day holiday also suggest mild growth. During the National Holiday, tourist visitation and sales grew by 5.9% and 6.3%, respectively, reaching 110% and 108% of 2019 level. Per capita consumption saw a 2% YoY growth, at around 98% of the 2019 level — an improvement from 89%/91% level in 2024 Labor Day holiday/2024 CNY Holiday. Therefore, we expect continued policy support, along with improving fundamentals and sentiment, to further bolster sector growth moving forward.

Stock Comments

- Trip.com Group (TCOM US): Trip.com achieved a 10% return in October. The recovery in Chinese outbound travel trend accelerated during the Golden Week. According to the National Immigration Administration, the avg daily cross-border volume reached 1.87m person times during the holiday, +25.8% YoY and 8% above pre-covid level. TCOM is well-positioned to provide better certainty with its dominant position in the Chinese outbound travel market and increasing exposure to the overseas OTA sector through its Trip.com platform.

- Pop Mart (9992 HK): Pop Mart achieved a 35% return in October backed by strong beat 3Q earnings. Pop Mart reported 120-125% YoY sales growth for 3Q24. By market, overseas market delivered 440-445% sales growth and China reported 55-60% sales growth, indicating robust QoQ acceleration for both regions (vs. overseas/China +260%/32% in 1H24). Going forward, we expect continued overseas expansion, particularly the ramping up in US market, strong product pipeline and potential improvement in Chinese consumer sentiment could further bolster sales growth.

- Moutai (600519 CH): Moutai experienced 12% loss in October due to Baijiu sector’s correction. Despite that, Moutai reported solid 3Q24 results on Oct 25, with sales up 15.6% YoY to Rmb39.7bn and net profit increasing 13.2% YoY to Rmb19.1bn. 9M24 sales growth of 17.0% (with earnings growth at 15.0%) is on track with company’s full-year sales growth target of 15%. Post National Day holiday, the wholesale price of a Feitian single bottle declined to Rmb2,250 from approximately Rmb2,300 during the holidays, which is within a reasonable range given seasonality. Additionally, Moutai has been managing its shipment pace to support pricing levels.

Preview

We believe policy stimulus could enhance consumer sentiment and bolster stock performance in the near term. As a late cycle play, consumer sector valuation has been compressed over the past year under an uncertain macroeconomic environment. Despite a recent rebound, the sector is currently trading at 16x PE as of September end, which remains well below the long-term average.

In our view, a fundamental turnaround and sustained improvement will take time. Large-cap sectors such as liquor, dining, and home appliances exhibit higher beta characteristics in a bullish macro scenario. Notably, home appliances and dining are also direct beneficiaries of consumer stimulus policies, including trade-in programs and consumption vouchers. For many consumer companies, especially staple names, we expect stabilization and recovery of earnings entering 4Q24 given easing comps.

The market is expecting additional stimulus measures in the near future. To track sector sentiment and performance, we recommend to follow forthcoming policy announcements, the impact of key initiatives such as trade-in program progress, and data points relating to consumer income outlook, including property price trends.

Global X China Robotics and AI ETF (2807 HK)

Industry Update

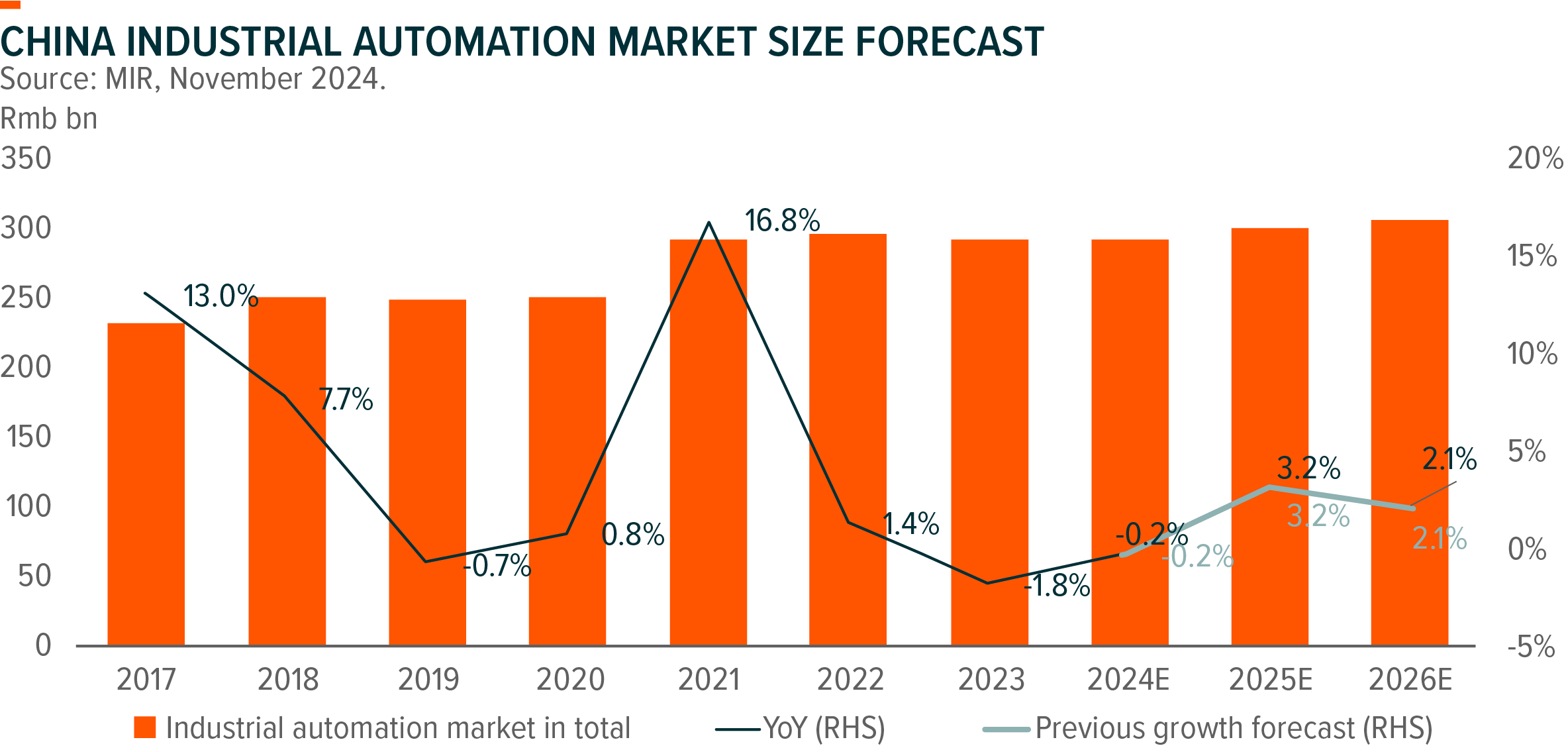

China industrial automation (IA) demand decline narrowed to 1.3%yoy as of 3Q24 from -2.8%yoy in 1H24. Demand from the OEM segment fell by 4.3%yoy, while demand from the end user segment turned around to +0.1%yoy growth with solid demand from chemicals, electricity and petrochemicals industries. MIR retains its mild recovery forecast in 2025 and 2026. By segment, servo demand was down by 3.6%yoy as of 3Q24, vs -5.8%yoy in 1H24. Inovance and Siemens maintained their top positions in servo systems but both saw market share lose due to sluggish demand in EV and lithium battery. Inverter demand fell by 7.7%yoy as of 3Q24. Inovance lost its top position to ABB (market share of 19.1% as of 3Q24), with market share declining to 18.6% during the same reporting period, owing to more exposure to construction machinery sector. Large/small PLC market continued declining by 35.8%yoy and 7.6%yoy as of 3Q24, respectively. Packaging, machinery, textile and F&B were the bright spot. Siemens remains the leader in PLC market, notwithstanding the trend of localization. Inovance’s market share in small PLC was 13.9% as of 3Q24, slightly improving vs 13.7% in 1H24.

Stock Comments

- Suzhou TFC Optical Communication: Company delivered strong Q3 results with gross margin improved significantly. Company is one of the key beneficiaries from AI computational demand growth in the long run.

- IEIT Systems: Company delivered strong Q3 results with revenue/net profits up by 76%yoy and 51%yoy, +68%qoq and +140%qoq, respectively. We have seen strong downstream capex that will boost demand for the server industry.

- Shenzhen Inovance Technology: New order inflow for Inovance remains soft in October despite low base for renewables segment in 4Q23. Valuation is relatively higher within the sector.

Preview

The Chinese government’s stimulus measures launched in late September, along with the “large-sized replacement program”, are starting to translate into improved enterprise confidence and the initiation of new projects. We have seen some early signs of stabilizing pricing trend and demand bottom-out. We remain positive on the long-term trend of China industrial automation market growth. Domestic manufacturers continue gaining market share on the back of customized products across emerging industries, fast delivery and advanced post-sale services, while foreign brands keep losing market share in China.

Global X China Semiconductor ETF (3191 HK)

Industry Update

TSMC posted strong 3Q result and 4Q guidance

3Q strong beat on GPM: 3Q24 GM exceeded its high-end guidance of 55.5%, to 57.8% (vs cons. Of 54.8%), with 4Q24 GM guidance coming in at 58% (at the midpoint; vs cons. of 54.7%) We believe this is driven by higher UTR (Utilisation Rate) in N5/N3, and slower than expected depreciation growth potentially due to slower ramp of oversea fabs. We think the N5 UTR likely exceed 100% in 3Q and will continue to stay at this level in 4Q.

4Q guidance beat: For 4Q24E, management guided revenue to be in the range of US$26.1-26.9bn. GM in the range of 57.0-59.0%, and OpM in the range of 46.5-48.5%. The margin guidance was well above street expectations due to higher utilisation rate.8

Memory makers ramp up HBM production

SK Hynix expect HBM3e 12H begin shipment in 4Q24. HBM 3e12H as % of total HBM3e will exceed 50% in 1H25. The volume and price of HBM products are largely locked in long-term contracts and HBM ASP in 2025E is expected to increase YoY along with the increasing share of the HBM3e products.

Samsung 3Q24 HBM revenue grew >70% QoQ. HBM3E mix was “low to mid -10s%” of the total HBM and is expected to be 50% in 4Q24. Samsung continue to make progress in Nvidia Blackwell HBM qualification, management commented an important HBM3E qualification phase with the “major account” has been completed and expect to start expanding sales in 4Q24.9

Stock Comments

- SMIC recorded +44.91% return. Domestic foundry utilization continues to recover on restocking orders. Market turn more positive on China semiconductor demand after the government announced stimulus package. SMIC has projected a 13-15% Q/Q revenue growth for 3Q24. 3Q gross margin guidance of 18-20% exceeds expectations, due to rising ASP, given a higher 12-inch wafer shipment mix.

- AMEC recorded +17.34% return. 3Q result was a miss but management provided positive outlook for 2025. 3Q24 revenue reached Rmb2,059mn, up 12% Q/Q and up 36% Y/Y. Backlog in 2024 will be Rmb11-13bn. 2025 backlog is expected to grow further as the management team expects 2025 foundry capex to enjoy 10%+ growth, along with market share gain in China.

Preview

Increasing AI adoption in the data centre and increasing penetration of AI at the edge and on-device will be the key enabler of next upcycle semiconductor as AI-enabled devices have much higher semi-content. Currently we are still in the process of cycle recovery as both stocks and earnings are below previous peak. We expect volume growth in end devices to drive broad-based semiconductor cycle recovery in 2024.

Global X China Cloud Computing ETF (2826 HK)

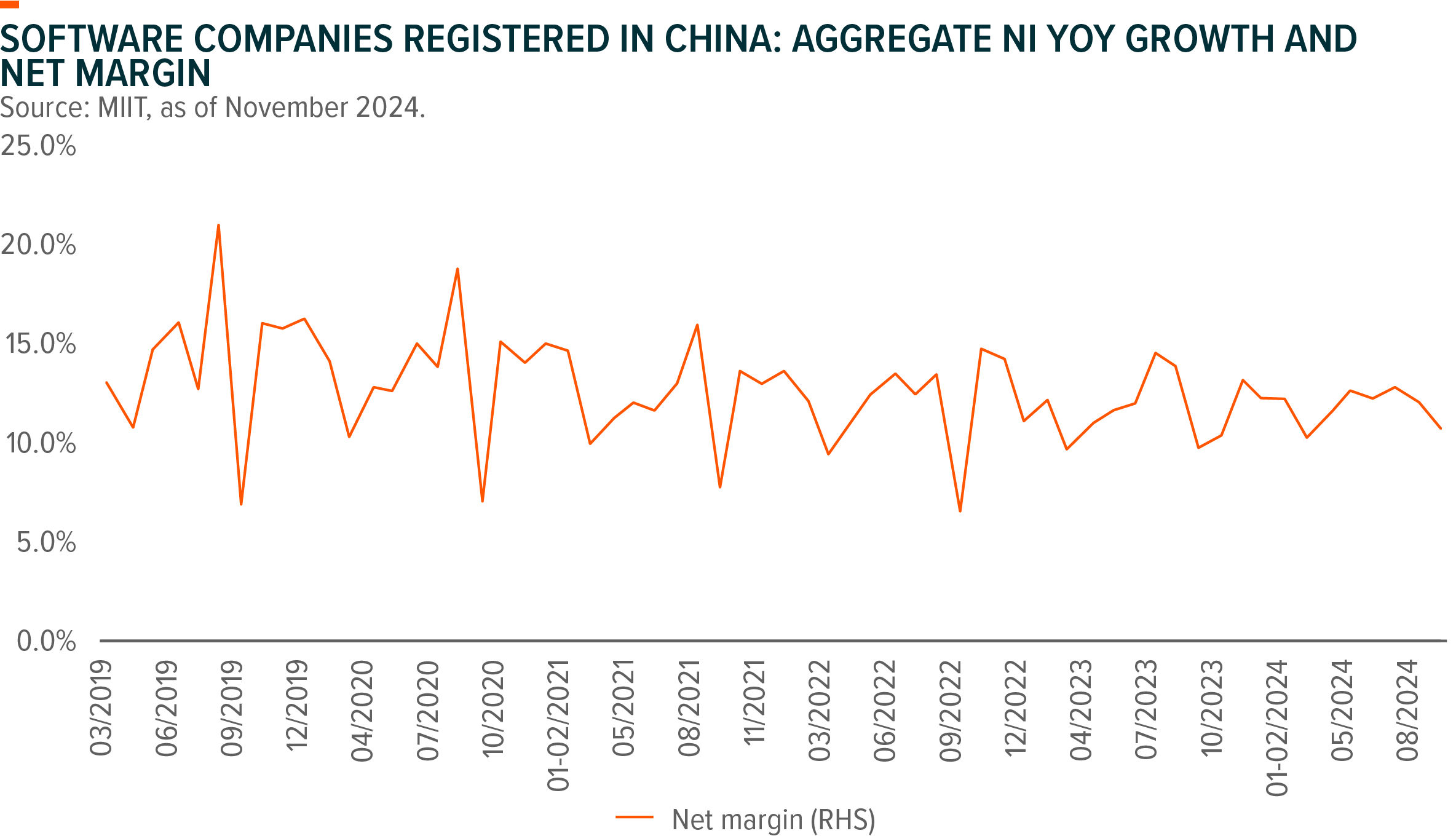

China software industry growth in September was weak at 8.2% YoY (vs. August at +9.4% YoY), down from last month, leading aggregate 9M24 revenues +10.8% YoY (vs. 8M24 at 11.2% YoY), due to delays of large-scale SOE projects, and slow improvement in client IT budgets. By segment, embedded system software and IT services outpaced software products and security software.

In September, aggregate net income of software companies registered in China was Rmb140bn (US$20bn), implying net margin of 10.9% (vs. 12.2% in August). 9M24 net margin was 11.8%, lower than 8M24 net margin of 12.0%.

Stock Comments

- iSoftStone Information Technology: iSoftStone is a leading domestic IT services supplier serving large-scale enterprises, including Huawei, internet companies, financial institutions and manufacturers. Overall market sentiment on Huawei related IT services stock during the month was positive, mainly driven by potentially increasing orders attributable to strong auto and mobile phone businesses of Huawei. iSoftStone’s business migration toward standard services and software products will result in a better margin in the medium-term.

- Tsinghua Tongfang: The company’s 3Q24 result was in-line with expectation. There have been expectations on potential M&A deals related to the name which led to stock price rally.

- Netease: NetEase underperformed both the internet and software peers, due to lack of meaningful new game contribution, and limited positive surprise in grossing from legacy games.

- Shanghai Baosight Software: Baosight reported 3Q24 revenue decline of 4.1% YoY to Rmb3,014mn, 10% lower than consensus. Normalized net profit declined 16.3% YoY, 20% below market expectation. However, recent order win signals positive. On Sept 22, Baosight announced that its IDC arm Bao Cloud has won the tender for a major internet hyperscaler’s new IDC with 60MW capacity contracted and another 60MW reserved. This is Bao Cloud’s first sizable order after being very muted for ~4 years and also the business’ first sizable order outside of Shanghai.

Preview

Overall the avg. revenue growth of local software names remained weak in 3Q24, due to the challenging environment and budget constraints. Into 4Q24E, major software companies’ revenue growth should accelerate because of low-base effect. Leading software companies’ managements still view employee efficiency improvement as one of the key priorities into rest of the year. Therefore, margin is set to improve mainly driven by cost control and efficiency improvement.

In 3Q24, the majority of the software names started to see increased holdings from local funds, likely happened since PBOC’s policy pivot at the end of Sept, while foreign funds remained on the sidelines, cutting more positions. Near-term share price might be overshooting but companies with improved revenue and earnings growth outlook should enjoy valuation premium.

Global X China Little Giant ETF (2815 HK)

Industry Update

Following a 25% strong return in September, Global X China Little Giant ETF delivered a resilient 3% return in October. In the current volatile market environment, small- and medium-sized enterprises (SMEs) have shown strong stock performance, particularly those benefiting from government support. Post US election, to mitigate the impact of rising US tariffs on China economy, Beijing would be likely to scale-up fiscal stimulus. The resurgence of trade tensions might reinforce the top leadership’s commitment to enhancing supply chain upgrades and achieving self-sufficiency. President Xi’s earlier remarks in October also underscored importance of science and technology in advancing China’s modernization. Therefore, these specialized and sophisticated SMEs play a crucial role in China’s transition to high quality development. Moreover, as a high-quality, small-cap fund, Global X China Little Giant ETF is likely to benefit more than large-cap funds if the economy turns to strong recovery in 2025.

Stock Comments

Suzhou TFC Optical

TFC is a leading passive component (ceramics, lens array, optical fiber adaptors, transmit optical packaging, arrayed waveguide grating, etc.) and active components (optical engines) supplier in the global transceiver supply chain and its key clients include major optical transceiver players in both domestic and overseas markets.

CPO is the trend for future: Fiber Array Units (FAU) are integral to Co-Packaged Optics (CPO) technology, serving as the bridge that ensures the precise alignment of optical fibers with Photonic Integrated Circuits (PICs), such as silicon waveguides and Electro-optic Integrated Circuits (EICs). This alignment is crucial for minimizing signal loss and maximizing the efficiency of data transmission. Currently, most FAU coupling solutions for pluggable transceivers are based on discrete product designs, which typically have a lower average selling price (ASP) of around $4-5.

The integration of more passive optical components through Silicon Photonics (SiPh) technology is a growing trend. In this context, the role of FAU becomes even more critical, and its coupling solutions are set to undergo significant advancements. Innovations such as 90-Degree FAU and Lensed-fiber coupling are expected to further reduce signal loss. These advancements will not only enhance the performance of CPO systems but also increase the content value of FAU, potentially leading to a multi-fold increase in their ASP. This evolution underscores the importance of FAU in the future of high-speed data transmission and the continuous development of CPO technology.

TFC is likely to benefit: TFC has stronger technology capabilities like CPO/OCS and stronger customer relationships (though Mellanox to Nvdia). Hence it is likely benefit from this trend.

Rockchip Electronics

Rockchip rallied on strong 3Q result. It achieved record revenue of RMB 911 million in 3Q24, marking a 51.36% increase YoY and a 29.12% rise QoQ, with a net profit of RMB 169 million, up 221.68% YoY and 46.75% QoQ. This performance was driven by market share growth in the AIoT sector, particularly in automotive electronics, and increased revenue from industrial and consumer markets.

The company’s GPM reached 37.34% in 3Q24, due to cost optimizations and a higher proportion of mid-to-high-end products. Rockchip’s flagship RK3588 chip experienced rapid sales growth, and the company expects to maintain stable GPM in 4Q24 with potential for long-term improvement.

Looking forward, Rockchip will focus on product and market development, aiming to enhance operating efficiency and create a diversified product portfolio.