Implications Following China’s National People’s Congress

Listen

China hosted its annual parliamentary meeting between the 5th to 13th of March 2023, revealing the country’s strategic policies in relation to its economy, trade, diplomacy, environment, and more. In the opening session, outgoing premier Li Keqiang announced the GDP growth target for 2023 to be around 5%, broadly in line with the local governments’ target announced earlier this year. Amid escalating concerns of a global economic slowdown, our view is that China purposely set a relatively conservative target, but the new cabinet would look to exceed 5% in practice. Since the re-opening, China is on track to recover its economy steadily, with most economic data points improved in January and gaining further momentum in February, as the feared second wave of COVID did not materialize. We expect domestic consumption will continue to be a key growth driver this year. In the rest of this article, we explore the potential implications following the Two Sessions across key investment themes in China.

Key Change in the Government Organization

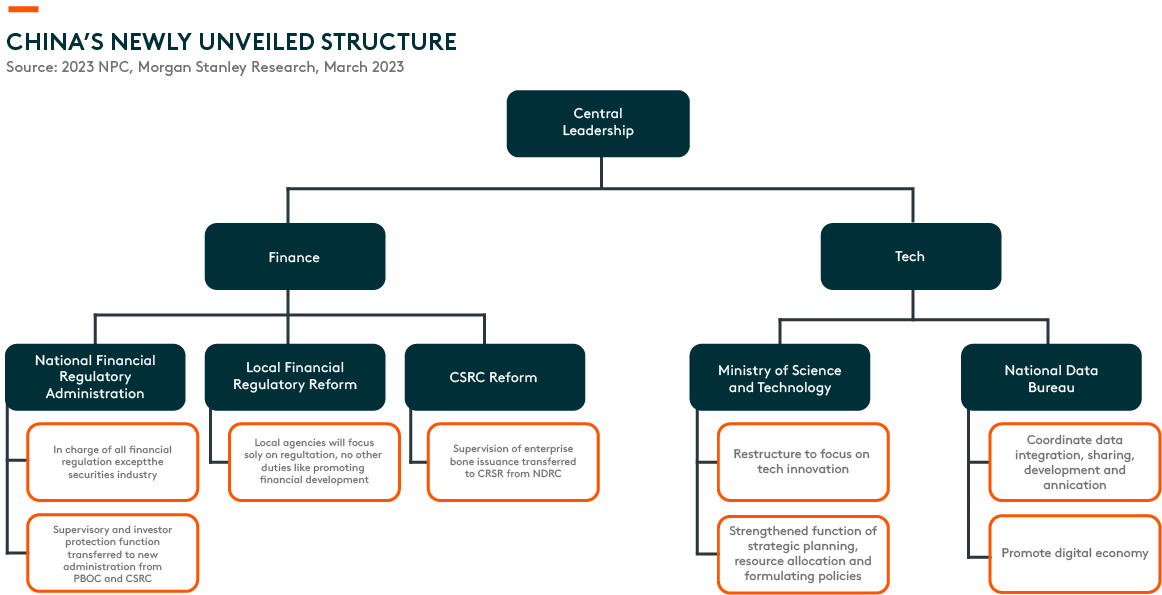

The Central Government unveiled a restructuring plan at the National People’s Congress (NPC) by establishing the National Financial Regulatory Administration and the National Data Bureau, and revamping the Ministry of Science and Technology. We regard these institutional changes to be positive with an objective to streamline regulatory oversight in the financial sector, promote the integration and utilization of big data, and accelerate technological innovation.

The reformed Ministry of Science and Technology will likely drive more dedicated and coordinated efforts in technological breakthroughs, especially in strategic tech industries like semiconductors and artificial intelligence (AI). Through the reorganization, China is looking to integrate science and technology with the economy more closely in order to promote productivity growth.

Electric Vehicle & Battery

Implication from NPC

In the NPC core meeting notes, the discussion around electric vehicles (EVs) falls under the section of boosting domestic consumption. The auto industry is an important contributor to China’s consumption growth. The manufacturing of a vehicle also involves a long supply chain. Hence, strong auto demand is positive for both consumption and industrial sector development. The government will add charging facilities and encourage battery recycling as a way to support the EV sector. Besides the main document are proposals from relevant officials and corporate leaders. Much of the new sector-relevant content is related to the energy storage battery sector, focusing on the energy storage industry ecosystem and battery recycling.

Latest Updates

After several phases of subsidy cuts in China, we believe the whole EV and battery theme is now less dependent on government policy incentives. Instead, electrification trends are now more driven by the shift in strategy from corporates and consumer behaviour change. As a result, more auto original equipment manufacturers (OEMs) are embracing the electrification demand, whether willingly or unwillingly, and are redirecting their resources into making competitive car models.

The main issue on the EV theme is around competition. Tesla announced a global auto price cut earlier this year, followed by many other Chinese OEMs. With many more traditional OEMs launching their EV car models, we anticipate intensified price competition in 2023. Cost-competitive car models, both EV and hybrid, are becoming more of a critical differentiator. This environment generally benefits vertically integrated automakers such as BYD and Tesla to win market attention and market share. On the battery end, CATL is trying a new pricing strategy to win market share by sharing its profits from mining lithium resources. We believe competition in a fast-growing theme is inevitable. But only the top leaders and technology innovators can survive during the market consolidation phase and thrive immediately after. The market leaders will be in an even better position post the consolidation and earn their bargaining power beyond this period.

Clean Energy

Implication from NPC

According to the NPC working paper, clean energy will be one of the key beneficiaries of “green development”. The Chinese government emphasized the need to strengthen the construction of urban and rural environmental infrastructure, implement important ecosystem protection, and repair major projects; promote clean coal utilization and technology development; endorse green development policies and promote energy-saving. This will be favourable to renewables and renewables-related infrastructure investment growth in 2023. Undoubtedly, clean energy will be one of the key tools to realize China’s long-term carbon neutrality ambitions.

Latest Updates

Sectorwise, the polysilicon shortage was the bottleneck in the solar value chain over the last two years. We witnessed a short and sharp fall in polysilicon prices around the new year holidays from the peak of RMB 300/kg to as low as RMB 120/kg, despite a very small number of orders applied.1 Channel checks show an accumulation of inventory, implying that a downward trend of polysilicon prices is almost ensured going forward. The total polysilicon shipment is expected to exceed 400GW, sufficient to fulfil the whole year’s demand.2 Therefore, we believe a shortage will no longer exist across the solar value chain in 2023. As a result, solar panel prices may end at a certain level widely accepted by the downstream, with a reasonable profit distribution amongst each segment.

We are quite bullish about the global solar demand in 2023 as polysilicon prices are stepping down, particularly in the second half of the year when new supply comes out. Additionaly, falling costs of manufacturing will drive up demand for solar farm installations in China. 2023 will also be a recovery year for the US market on the back of Biden’s supportive policies for US clean energy.

The imminent technological innovation and differentiation of more powerful solar cells are also worth mentioning. Solar cell technology migration from PERC to the next-generation product has been the key trend since early 2022 and will likely speed up in 2023, particularly for Topcon. An increasing number of solar cell makers or integrated solar panel makers are accelerating mass production of Topcon, while the development of xBC solar cells in residential projects and cost-cutting for HJT solar cells are just around the corner. There is no conclusion yet about which technology will be the winner to replace PERC. The most likely outcome is that cell makers diverge in solar cell technologies for years, while cautiously adding new capacities. What’s worth highlighting is that the current PERC capacities are quite new and concentrated in a few big solar companies. These companies have incentives to fully utilize their PERC capacities before moving on to the next generation of technologies, even if they already have them. Therefore, we anticipate PERC will remain the mainstream product in 2023.

For wind, the new order growth of China wind projects remains very compelling in recent months, thanks to solid project economics. The moderation of raw material inflation has helped to improve the margin outlook of wind component suppliers and enhanced the profitability of companies in the supply chain. Despite the strong new orders, the pace of actual installations has been slower than expected, partly due to the disruption of lockdowns in December and January. However, there is now growing interest in the space as we expect the logistics and installation disruptions to be behind us. Into the rest of the year, we believe the strong new order growth in 2022 will finally translate to actual installations in 2023.

Semiconductor & Hardware

Implication from NPC

China will restructure its science and technology ministry to channel more resources to achieving important breakthroughs, with the goal of moving faster towards self-reliance. The proposed restructuring of the Ministry of Science and Technology (MoST) signals more targeted efforts in supporting tech and innovation, as well as a top-down approach to organizing nationwide research and development (R&D) resources.

The direction is in line with the focus of industrial upgrade from the Government Work Report and a continuation from the 14th Five-Year Plan, which listed multiple strategic areas such as AI, quantum computing, semiconductor and other technologies, which will enjoy policy support. Other functions of the old MoST, such as overseeing technology advancement for agriculture, will be consolidated into other ministries. The proposal also upgrades the National Intellectual Property Administration to a State Council department, indicating stronger protection of IPs, an essential institutional element for innovation.

Latest Updates

In 2023, with the further recovery of the semiconductor industry supply and demand dynamics, some subsectors, such as chip design and foundries, are expected to bottom out and usher in recovery in the second half of the year. Over the medium and longer term, localization and structural demand from high-performance computing (HPC) and new energy applications continue to be the key driver for the domestic semiconductor industry.

Cloud Computing

Implication from NPC

China’s digital economy totalled USD 7.1 trillion in 2021.3 At 16.2% year-on-year (y/y) growth in 2021, China’s digital economy has grown significantly faster than the country’s overall GDP growth and accounts for roughly 40% of total GDP, up by 1.2ppts from 2020.4

The State Council issued the “Rollout Plan for Digital China” (the Plan) to achieve major progress by 2025 and material digitalization by 2035. The Plan specifies that China will 1) accelerate the construction of digital infrastructure (e.g. 5G, gigabyte fiber, IPv6 implementation, IoT, and BeiDou Satellite system) and improve the layout of computing power such as data centers, and 2) circulate the digital resource cycle by building country-level data management mechanisms, better utilize the data resources, and unleash the value of commercial data.

We expect the Chinese government’s rising focus on building a digital economy will provide a positive policy environment for internet, software, and telecommunication services companies. The Plan accelerates demands for cloud computing resources, benefiting cloud computing service providers like telecom (private cloud) and large internet companies (public cloud). Moreover, increasing the exchange of data resources amongst industry participants will lead to rising requirements for cybersecurity, resulting in increasing cybersecurity spending. According to IDC, China’s cybersecurity spending will record a CAGR of 18.8% between 2021 and 2026, much higher than the 11.9% growth expected globally.5 Lastly, we expect software localization demand to recover in 2023, driven by the national strategy and more government procurement.

Consumer

Implication from NPC

As expected, no specific consumption-related policies were announced at the NPC this year, and we did not expect any large stimulus packages to be announced during the meeting. The government seems to be relying on domestic consumption recovery to offset weaker exports and drive economic growth in 2023. We expect a job market recovery, stabilized property market, a recovery of consumer confidence, income growth, and the release of excess savings to drive private consumption growth throughout the year.

Latest Updates

We have witnessed a weaker February recovery trend than January, which we think is largely due to the timing difference of the Chinese New Year. In aggregate, for the first two months, our channel checks suggest that overall China consumption growth year-to-date remains solid. Strong February PMI data suggests that recovery is gaining momentum, with employment PMI rebounding during the month to expansionary territory. Mobility in China has already improved beyond pre-Covid levels, reflecting further normalization in business activity and travel. In addition, property markets have largely stabilized, with primary sales in the top 28 cities showing some recovery trend, according to Morgan Stanley. We believe the overall recovery trend remains on track and expect a stronger recovery from the second quarter onwards, which would reinvigorate the market’s confidence in the consumption growth outlook in China.

While we are waiting to hear more from the management of consumer companies in the upcoming weeks during the results season, we remain constructive on the consumption outlook in China this year. Overall, we believe private consumption will be the major growth driver of China’s economic growth, benefiting Chinese consumer companies in 2023.

Biotech

Implication from NPC

While no specific biotech-related measures were announced during the Two Sessions, the lack of any discussion on central procurement is a positive as it appears that the aggressive price cut for drugs is behind us.

Latest Updates

The new 2022 National Reimbursement Drug List (NDRL) was officially launched and will be effective from 1 March 2023. The new NDRL includes 2,967 drugs: 1,586 western drugs and 1381 finished traditional Chinese medicine (TCM). There are +111 new entrants with an average price cut of 60%. Among the 111, 23 drugs are very new, launched only in 2022. 14 oncology drugs made the cut after price negotiations, along with new indications from 10 existing oncology drugs. With this list, around RMB 90 billion is expected to be saved over the next two years.

For the CRO (Contract Research Organizations) / CDMO (Contract Development and Manufacturing Companies) sub-sector, excluding COVID projects, we expect the growth rates to range between 20-30% for most companies.6 For example, the management incentive plan for Tigermed Consulting assumes a 21% growth rate for 2023.7

For large companies, we expect core business volume growth to bounce back to 10-15% as normalization kicks in, which will be further aided by their innovative drug portfolios, which will likely be above this growth rate. Finally, for biotech companies, many are still in the early days of profitability.