Why FinTech is Thriving in Emerging Markets

Emerging markets (EM) are proving to be fertile ground for financial technology (FinTech) to disrupt the financial services industry. Innovation in mobile payments, online banking and alternative lending platforms challenge the norm by leveraging technology to bring financial services to previously unbanked and underserved populations, and offer alternatives to incumbent service providers.

Historically, individuals and small businesses in emerging markets suffered from a lack of access to basic financial services, with banks only extending their offerings to the country’s wealthiest. This left many to rely on cash-based transactions which can be susceptible to fraud and theft, while access to loans were sparse. Yet with new technologies that leverage software and mobile connectivity, digital services are being extended efficiently and inexpensively to hundreds of millions of people in the developing world. The widespread adoption of these services is likely to accelerate growth, fueling consumerism, technological leap-frogging and more effective government policies.

Demographics Propel Emerging Market Growth

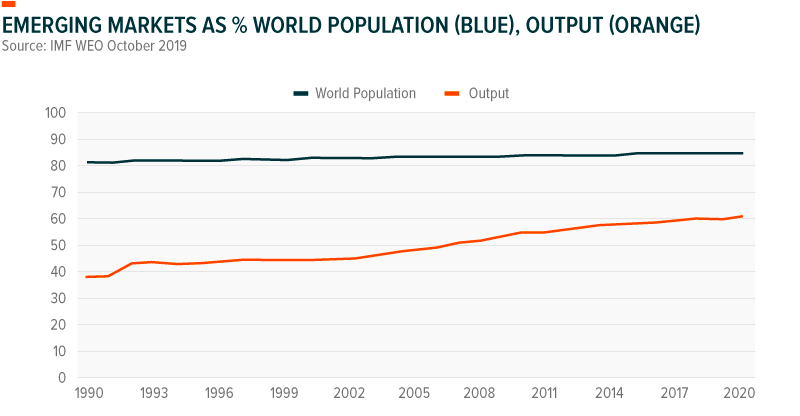

EMs make up nearly 86% of the world’s population yet produce only 40% of global economic output.1 However, EMs increased their share by nearly 10% over the last decade as fast-growing economies shifted from export-driven strategies to prioritize consumer-oriented growth.2 Total global consumption is expected to reach US$62 trillion by 2025 that is double 2013 levels, with half of this growth derived from EMs alone.3

Such growth benefits EM consumers, who are becoming wealthier and entering the middle class by the hundreds of millions. And with wealth comes the need for more financial services. Older generations may want savings accounts and insurance products, while younger generations prioritize linking a bank account to their phones for easy mobile payments.

FinTechs are especially powerful in EMs because they are able to capture unmet demand, filling gaps in the financial system left by traditional institutions for banking services and financial products. Roughly 2 billion adults lacked access to financial services globally, yet demand growth for such products has soared in EMs like China, which grew from 1% of global life insurance premiums in 2010 to 10% in 2017.4 And while the percent of unbanked or uninsured varies from country to country, serving underbanked individuals in EMs alone could generate US$200 billion in revenue.5

With FinTech, financial inclusion becomes a much more attainable goal because it becomes much cheaper to reach smaller or underserved segments of the population that might have previously been considered as “unattractive” customers. FinTech platforms largely have upfront costs with program and infrastructure development. By relying heavily on technology however, ongoing and variable costs tend to be quite low, making it possible to realize profit on a bank account with limited assets or a micro loan.

Greater Technology Adoption: Unlocking and Enabling Consumer Transactions

Internet penetration is lower in EMs than in the developed world, but a large population and a substantial willingness to adopt new technologies creates enormous potential. China for example has over 3x more internet users, over 3.75x more mobile phone users and spends 7.5x more money through mobile transactions than the US. Over the past decade, mobile phone usage has skyrocketed in China, with smartphone ownership in China growing from 56% in 2011 to 96% in 2018.6 For reference, mobile phone usage in the US is 96% but smartphone usage is 15% lower in the US at only 81%.7

Without existing infrastructure in place like traditional bank branches and credit cards, EMs can easily adopt the latest technology without forcing an old business model into obsolescence. China has the highest adoption rate of mobile payments globally, leapfrogging credit cards to spend over US$15 trillion in 2017 digitally. This compares to just US$2 trillion in the US, as consumers slowly shift away from paying with plastic. For perspective, consumers in China spent just US$377 billion five years earlier, demonstrating the rapid rise of this technology.8

Big Tech Becomes FinTech

Some of the largest tech companies in the emerging markets are waking up to the opportunity in FinTech and making major investments in the space. Global investment in FinTech increased from US$50.8 billion in 2017 to a new highs of US$135.7 billion in 2019.9 The Asia Pacific region accounted for nearly 20% of the 2,693 FinTech deals completed globally in 2019 as major tech platforms sought to incorporate FinTech services into their ecosystems.

China’s Tencent for example began originally as a social media application, but by 2017 facilitated 40% of China’s mobile payments.10 The platform allows users to make payments, order food delivery, purchase entertainment tickets and order rides through one of its million-plus “mini-apps”.11 The firm accomplished this by buying stakes in nearly 300 companies across developed and developing markets over the past six years.

Another major area of investment is in digital banking, offering online bank accounts, transfers and loans to occur without depending on a physical branch location. These themes are powerful in EMs, given their large, unbanked populations, inefficient banking systems and general lack of financial infrastructure.

In Brazil, major banks, including Bradesco, Itaú, and Banco do Brasil, are going digital to provide and expand client services as more transactions are conducted through the internet or mobile phones. In 2019, over 80% of transactions conducted by Banco do Brasil were carried out on mobile phones.12 Many of these services are offered through the WhatsApp messaging platform and range from simple balance checks to complex debt restructuring services. In its 2019 annual results, Banco do Brasil said that its retail customers renegotiated nearly US$4 million in debt via WhatsApp.13

Innovative Policies Bring Innovative Technologies

Recognizing the value of a more inclusive financial system, EM governments are increasingly supporting FinTech efforts through relaxed regulations, infrastructure development and pro-consumption policies.

Some EM governments are incubating domestic FinTech efforts by cultivating their own start-up hubs or clusters. Public-private partnership programs (PPPs) such as Start-Up Chile, Start-Up Brazil and IncubAR (Argentina) provide equity-free funding, training, mentorship and partnership opportunities for innovators, as well as special visa programs for foreigners. By keeping barriers to entry low, these programs are a relatively easy way governments can encourage innovation.

Other measures remove regulations to foster innovation. For example, the sandbox approach permits new products, technologies and business models to be tested under easier regulatory conditions, with appropriate supervision requirements and safeguards. These flexible frameworks allow incumbents and challengers to innovate outside of the existing regulatory framework while regulators monitor the impact.

EM regulatory bodies and central banks using this framework include the Central Bank of Brazil (BCB) and the Central Bank of Malaysia (BNM) in EMs. The sandbox approach is especially helpful for EMs because it fosters financial inclusion, which is critical to developing financial systems.

Under this framework, countries are developing advanced biometric ID systems, alternative credit scoring models, novel servicing platforms and distributed ledger technologies (DLT) such as blockchain.

Who are the Emerging Market FinTech Leaders?

Several prominent EM FinTechs are local firms that graduated from startups to unicorns, before becoming multi-billion-dollar tech giants. Often these firms recognize unmet demand or look to disrupt an inefficient or anti-competitive domestic financial services industry. Other major players include FinTech firms from developed markets, whose software or infrastructure can be adapted to local emerging markets.

Conclusion

FinTech is a disruptive theme challenging all ways that money changes hands. For individuals it can remove frictions and reduce the costs of paying for goods, saving and investing. For businesses, it can digitalize certain functions, reduce borrowing costs and enhance risk controls. While FinTech’s potential is global in nature, its potential across the EM landscape is vast as demand for broader access to financial services and greater competition is widely unmet.

Within FinTech, it may be an unusual case where EMs lead their developed market peers who are playing catch up, such as the US Treasury Department and the Office of the Comptroller of the Currency’s Fintech Charter, the European Central Bank (ECB) blockchain project or the US Federal Reserve’s plans to implement a real-time payments system by 2024.14