Important Information

Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- The investment objective of Global X Hang Seng High Dividend Yield ETF (the “Fund”) is to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Hang Seng High Dividend Yield Index.

- Whether or not distributions will be made by the Fund is at the discretion of the Manager taking into account various factors and its own distribution policy. There can be no assurance that the distribution yield of the Fund is the same as that of the Index.

- The Fund may invest in mid-sized companies, which may have lower liquidity and their prices are more volatile to adverse economic developments.

- The Fund invests in the emerging markets which may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risks, currency risks/control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

Why Hang Seng High Dividend ETF Outperformed the Market

The Global X Hang Seng High Dividend Yield ETF (3110 HK) has drawn investors’ attention by consistently outperforming the general market.

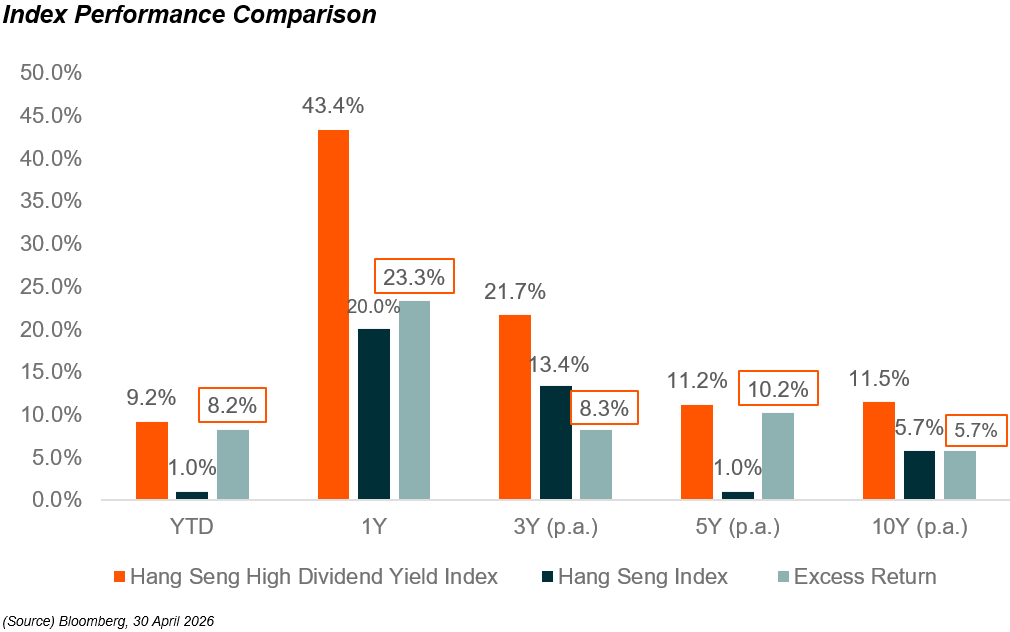

This trend was also demonstrated in the first four months of the year. From the beginning of January through April, the ETF delivered an exceptional performance, surging by over 10%. In contrast, the broad market Hang Seng Index (HSI) remained relatively muted.

But it’s not only for this year. For the last ten years to April 2026, the underlying index’s annualized return was 11.5% vs. 5.7% for Hang Seng Inex, implying 5.7% annualized excess return.

What lies behind the index’s sustained outperformance? The driving forces can be broken down into three pillars: valuation re-ratings, macroeconomic shifts, and structural industrial reforms.

Background 1. Re-rating

The primary background driving the index’s outperformance is the structural valuation re-rating of Chinese State-Owned Enterprises (SOEs) and traditional industries. The constituents of the Hang Seng High Dividend Yield Index are concentrated in mature, legacy sectors.

Following prolonged market corrections throughout the 2010s, these companies traded at historically depressed multiples, frequently languishing at a Price to Earnings ratio (PER) of 5~6x and a Price-to-Book ratio (PBR) below 0.5x.

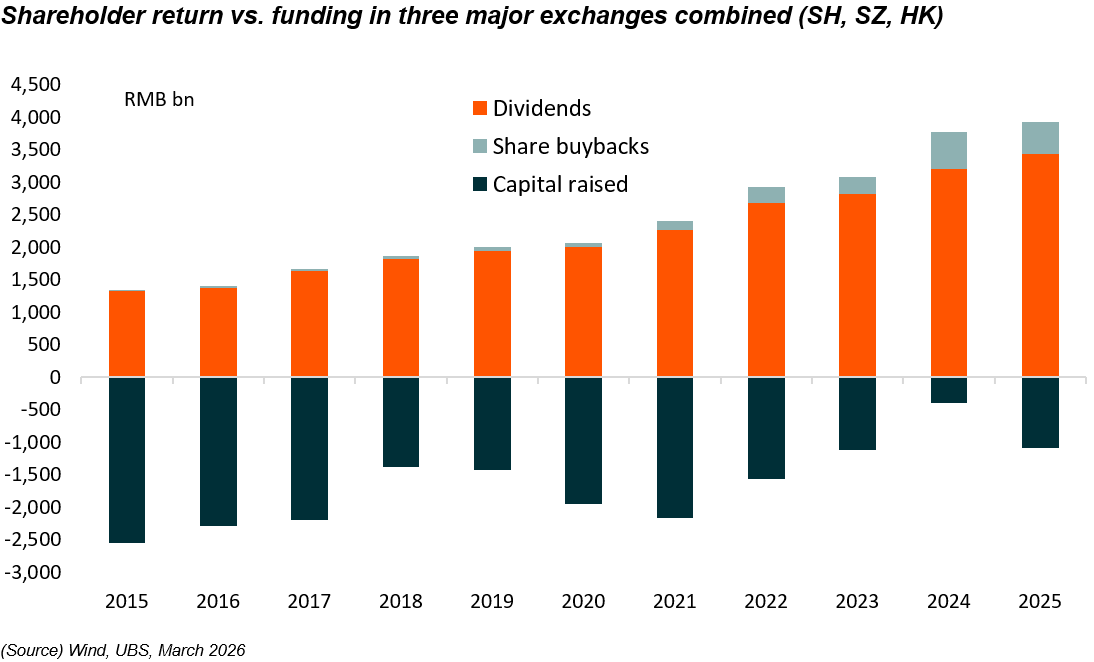

Recently, resilient operational earnings coupled with aggressive state-backed capital market reforms—such as “New Nine Measures(新国九条, 2024)” aimed at enforcing corporate payouts—triggered a powerful valuation re-rating.

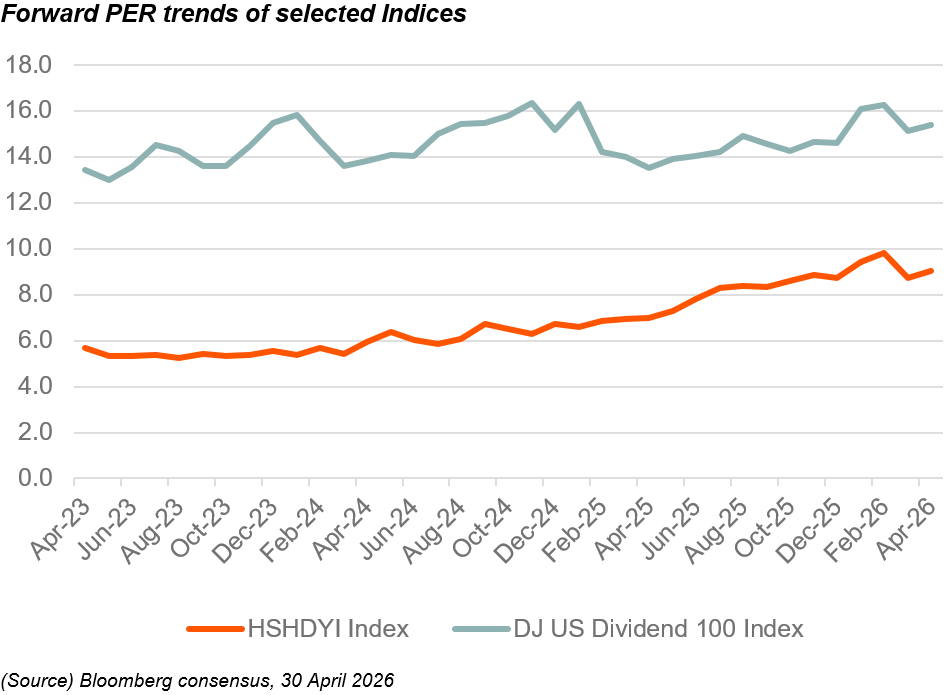

Even with its 12-month Forward PER expanding toward the 9x range, the index continues to trade at a steep discount to Western benchmarks, such as the Dow Jones US Dividend 100 Index.

Background 2. Widening Yield Gap

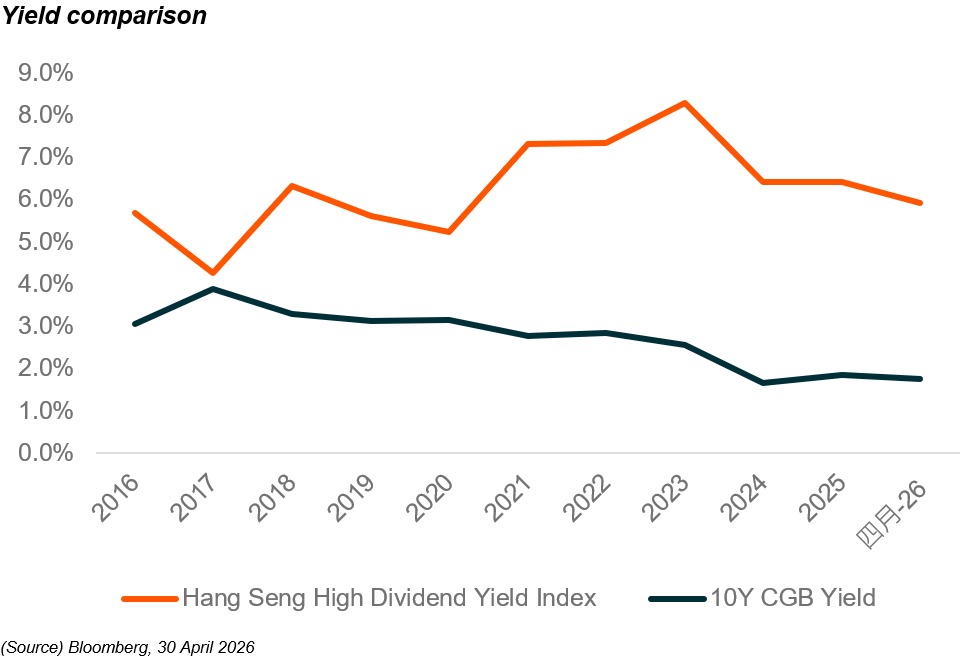

The second background is the evolving yield environment in Mainland China in favour of high-yielding equities. Low inflation and ample liquidity have compressed the 10-year government bond yield to approximately 2%, a steep decline from the 4% level maintained during the early 2010s. Simultaneously, banks’ one-year deposit rates have trended below 1%, compelling retail and institutional investors to seek out yield-generative alternatives like high dividend yield stocks

This transition has catalysed historic capital inflows into Hong Kong via the Southbound Stock Connect infrastructure. Because dual-listed state-owned enterprises traditionally trade at deep valuation discounts in Hong Kong (H-shares) relative to their domestic mainland listings (A-shares), their effective dividend yields have been higher.

Background 3. Reforms

The final background stems from a stabilized, consolidated competitive landscape.

While the State-Owned Enterprises (SOEs) within the ETF’s portfolio generally deliver modest revenue growth, they generate resilient free cash flows. Thanks to the sweeping “supply-side reforms(供给侧结构性改革)” implemented over the past decade, upstream industries such as materials, energy, and infrastructure, have largely eradicated excess capacity and achieved market consolidation.

Furthermore, the regulatory landscape has evolved to structurally enforce capital discipline. Beijing’s landmark “New Nine Measures(新国九条)” framework has effectively curbed corporate overinvestment. Because access to fresh equity financing from the capital markets has been significantly reduced and highly scrutinized under these regulations, companies are disincentivized from pursuing speculative capital expenditure. Instead, they are channeled toward boosting shareholder distributions.