Important Information

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. There is no guarantee of the repayment of the principal. Investors should note:

- Global X China Consumer Brand ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- The performance of companies in the consumer sector are correlated to the growth rate of the global market, individual income levels and their impact on levels of domestic consumer spending in the global markets, which in turn depend on the worldwide economic conditions, which have recently deteriorated significantly in many countries and regions and may remain depressed for the foreseeable future.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

Monthly Commentary on China Consumer Brand ETF – Aug 2023

[2806/9806] Global X China Consumer Brand ETF

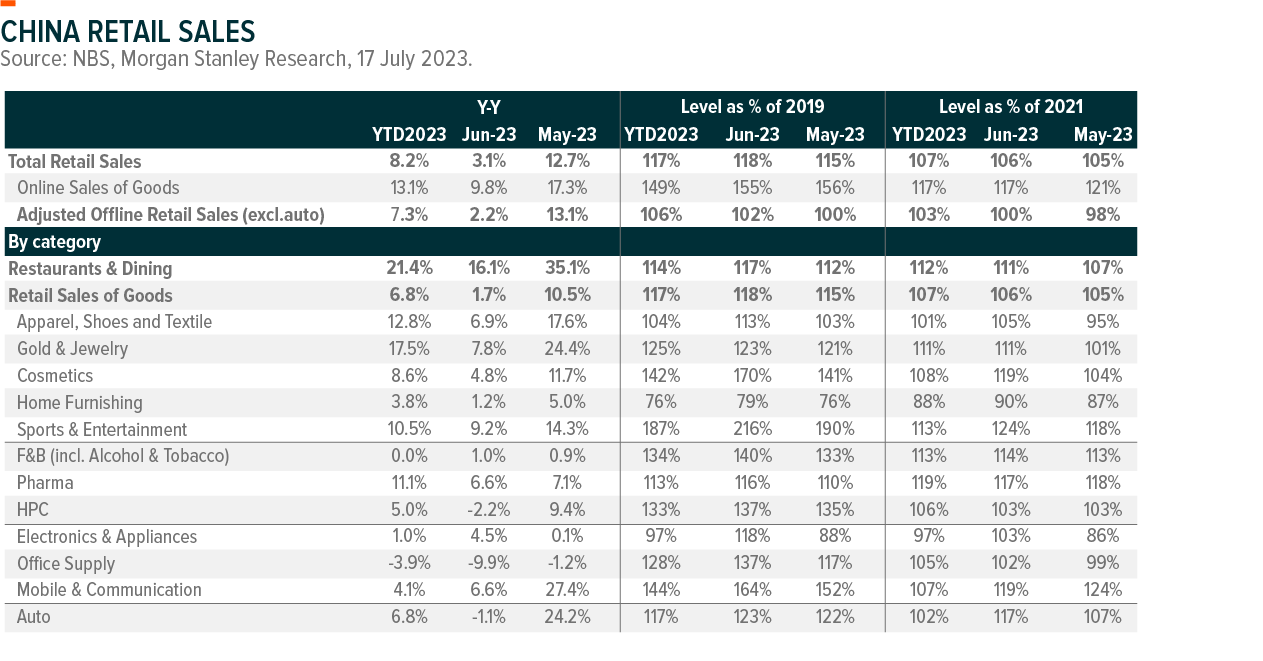

China’s consumption recovery pace remains sluggish amid reopening impact fading out. June retail sales growth came in at +3.1%yoy decelerating further from May’s +12.7%yoy growth partly due to a high base. This implies June retail sales reached 118% of 2019 level and total retail sales grew +8.2%yoy in H1 23. A weak property market and a high youth unemployment rate continued to weigh down on consumer confidence which went down back to 87.1 in April from 94.9 in March 2023. July retail sales trend is expected to have remained weak according to our channel checks.

The government held politburo meeting earlier than expected and set more dovish tone reaffirming its focus on economic growth. We expect more easing policies to be announced post this politburo meeting on July 24, 2023. In fact, the NDRC issued 20 guidelines to boost consumption recovery on July 31, 2023. The guidelines cover overall consumption aspects including support on purchases of big ticket items like auto and home appliances, consumer services such as restaurants and cultural tourism, as well as rural consumption and relevant infrastructure. We expect more detailed policies to be announced in coming months. In addition, the government is expected to further ease monetary policy, continue its efforts to stabilize property market as well as improve business confidence. This may then improve consumer confidence which will lead to gradual consumption recovery in H2 23.

While overall consumer sentiment remains weak, K consumption trend has continued in China. Most European luxury companies have reported their Q2 23 earnings and surprisingly, China has shown robust growth during the quarter for luxury brands. According to BofML estimates, Chinese luxury demand on average was up +80%yoy in Q2 23 on a weighted basis for those who provided commentary on China, and this implies +34% growth compared to Q2 21 level. In general, overall Chinese luxury demand has been stronger than the market expectation albeit weak overall consumption in the country. Similarly, Anta announced its Q2 23 update and shared that Anta core brand grew high single digit % yoy whereas its higher end brands like Fila’s retail sales grew high teens % yoy, Descente and Kolon’s retail sales grew 70-75%yoy during the quarter. We assume consumers traded down from Anta brand to lower priced other local brands amid weak consumption, while demand for higher end brands stayed more resilient. While Anta’s management has not changed their full year targets, they shared that they have not yet witnessed meaningful pick up in sales in July.

We expect more gradual consumption recovery this year as we need consumer sentiment to improve for high household savings to translate into consumption in a more meaningful way. We expect to see more policies to be announced to support economic and consumption recovery post July politburo meeting. The government will continue focus on economic growth and put more efforts to stabilize property market, improve business confidence as well as job market, which then will improve consumer confidence that can lead to a consumption growth in coming quarters.