Important Information

Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- The investment objective of Global X China Electric Vehicle and Battery ETF’s (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive China Electric Vehicle and Battery Index.

- The Fund is exposed to concentration risk by tracking a single region or country.

- The Index constituents may be concentrated in a specific industry or sector, which may potentially more volatile than a fund with a diversified portfolio.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy may invest up to 50% of its net asset value in financial derivative instruments (“FDIs”), which may expose the Fund to counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. The Fund may suffer losses from its usage of FDIs.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X China Clean Energy ETF (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive China Clean Energy Index.

- The Fund is exposed to concentration risk by tracking a single region or country.

- The Index constituents may be concentrated in a specific industry or sector, which may potentially more volatile than a fund with a diversified portfolio.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy may invest up to 50% of its net asset value in financial derivative instruments (“FDIs”), which may expose the Fund to counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. The Fund may suffer losses from its usage of FDIs.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X China Consumer Brand ETF (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive China Consumer Brand Index.

- The Fund is exposed to concentration risk by tracking a single region or country.

- The Index constituents may be concentrated in a specific industry or sector, which may potentially more volatile than a fund with a diversified portfolio.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy may invest up to 50% of its net asset value in financial derivative instruments (“FDIs”), which may expose the Fund to counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. The Fund may suffer losses from its usage of FDIs.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X China Robotics and AI ETF’s (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the FactSet China Robotics and Artificial Intelligence Index.

- The Fund is exposed to concentration risk by tracking a single region or country.

- The Index constituents may be concentrated in a specific industry or sector, which may potentially more volatile than a fund with a diversified portfolio.

- Robotics and artificial intelligence sector is sensitive to risks including small or limited markets for such securities, changes in business cycles, world economic growth, technological progress, rapid obsolescence, and government regulation.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy may invest up to 50% of its net asset value in financial derivative instruments (“FDIs”), which may expose the Fund to counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. The Fund may suffer losses from its usage of FDIs.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X Hang Seng TECH ETF (the “Fund”) is to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Hang Seng TECH Index.

- The Fund is exposed to concentration risk by tracking a specific regions or countries.

- The Index constituents may be concentrated in a specific industry or sector, which may potentially more volatile than a fund with a diversified portfolio.

- The Fund’s investments are concentrated in companies with a technology theme. Technology companies are often characterised by relatively higher volatility in price performance. Companies in the technology sector also face intense competition, and there may also be substantial government intervention, which may have an adverse effect on profit margins. These companies are also subject to the risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

- The investment objective of Global X China Little Giant ETF (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive China Little Giant Index.

- The Fund is exposed to concentration risk by tracking a single regions or countries.

- The Fund may invest in small and/or mid-sized companies, which may have lower liquidity and their prices are more volatile to adverse economic developments.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy may invest up to 50% of its net asset value in financial derivative instruments (“FDIs”), which may expose the Fund to counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. The Fund may suffer losses from its usage of FDIs.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

Monthly Commentary

China Thematic ETFs – September 2025

Global X China Electric Vehicle and Battery ETF (2845)

Industry Update

Divergent August EV Sales: According to CPCA, August NEV wholesale sales volume was 1.3mn, +10% YoY, +24% MoM. By individual brand, BYD reported August NEV PV sales of 374k units, flat YoY and +9% MoM. Overseas sales contributed 22%. Xpeng recorded YoY sales growth of +169% YoY to 38k, with MONA exceeding 15k. Li Auto sold 28.5 units in the month, -41% YoY. Management now targets monthly BEV sales to reach 18-20k units at a steady state. (for reference only, above mentioned stocks are not necessarily in the constituent list of the ETF). (CPCA, Company data, August 2025)

Battery material costs remained low: Battery grade lithium carbonate price at the last week of August was Rmb77.5k/ton, -3.1% wow, -5%/+1%/+2%/+18% vs. average of 3Q24/4Q24/1Q25/2Q25. Battery materials prices have decreased by over 80% from its peak in 2022, supporting the continued cost optimization for battery makers and EV manufacturers. (Goldman Sachs, August 2025)

Stock Comments

Shenzhen Inovance recorded 18% return in the month, a key contributor to the ETF. The company reported better than expected 2Q25 results, with revenue rising 19% YoY to Rmb 11.5bn and recurring Net Profit rising 13% YoY to Rmb 1.4bn. Inovance is spending increasing efforts on humanoid robot components, and is developing a series of modularized and standardized products. The company targets to debut humanoid robot components around September. (Company Data, Mirae Asset, August 2025)

CATL recorded 16% return in the month, a key contributor to the ETF. The company reported solid 2Q25 results, with record high net profit of Rmb 16.5bn (+34% YoY) driven by overseas expansion. Battery unit profit remains stable at Rmb110/kWh, thanks to raw material cost deflation and well executed cost control. In 1H25, overseas markets marked 34% revenue contribution amid robust EV momentum in Europe, while overseas GPM edged up by 4ppt to 29%. (Company Data, Mirae Asset, August 2025)

Tuopu recorded 36% gain in the month, a key contributor to the ETF. 2Q25 result was a slight be, with revenue up 9.7% YoY/24.3% QoQ to Rmb7.17bn, which we mainly attribute to its active penetration into domestic OEMs. Tuopu is already partnering with global top humanoid robot manufacturers on linear actuators, rotary actuators and dexterous hand motors. It is also tapping into other robot-related areas such as body structures, sensors, foot shock absorbers and electronic flexible skins. (Company Data, Mirae Asset, August 2025)

BYD reported a relatively weak set of quarterly results, with 2Q25 earnings of Rmb6.4bn (-30% YoY and -31% QoQ), below market expectations. Revenue grew 14% YoY to Rmb201bn. GPM was the key disappointment, with 2Q GPM falling 3.8ppts QoQ to 16.3%, dragged by dealer rebates, BoM cost increase, and price cuts in May. Price cut and Deal rebates could be oneoff and not extended into 2H. With stabilizing price and government’s ongoing anti-involution campaign, unit profit in the domestic market could further recover into 2H. On the other hand, overseas volume is tracking better than expectation, supporting both revenue and profit growth for BYD. Despite near term headwinds, long term outlook for BYD remains robust on the back of its vertical integration, technology leadership, and rapidly expanding global footprint. (Company Data, Mirae Asset, September 2025)

Preview

We remain positive on the long term growth potential for EV and battery value chain, along with the upward EV penetration trajectory. Domestic old car replacement demand, as stimulated by scaled-up auto trade-in program (which has been extended in 2025), together with export sales, should support China’s resilient auto momentum and benefit leading domestic brands. Anti-involution campaign by the government could potentially improve the pricing environment. We expect the China auto market to stay competitive with strong new product line-up and technology innovations from leading EV and battery brands, and new entrants such as Xiaomi. BYD’s launch of God’s Eye ADAS in mass market model should accelerate smart driving adoption in China. Geopolitical tensions remain the key risks, but China EV models will still remain competitive under new tariff landscape thanks to its cost advantages. Localized production will be the longer term solution for Chinese brands.

Global X China Clean Energy ETF (2809)

Industry Update

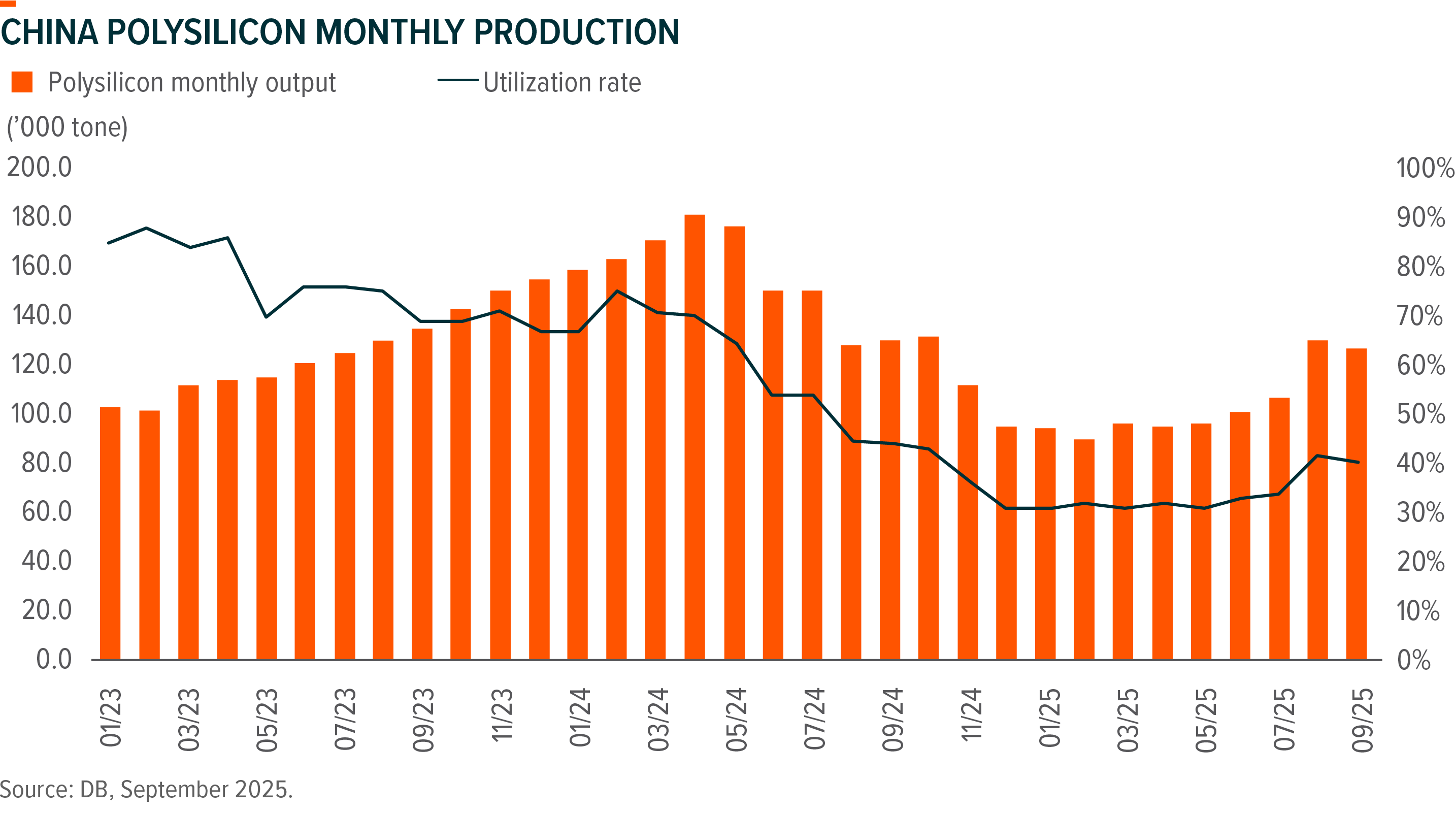

In July, China added 31.5GW (-1.9%YoY) generation capacity, including 16.2GW thermal (+1.6%YoY), 11.0GW solar (-47.6% YoY) driven by end of rush installation up to 31 July driven by government paper No.136 issued on 9 Feb, 2.3GW wind (-43.8%YoY), 2.0GW hydro (+1.3%YoY), and nil in nuclear. In 1H25, China’s new power generating capacity was 324.8GW (+75.7% YoY), comprising 223.3GW solar (+80.7% YoY), 53.7GW wind (+79.5% YoY), 42.0GW thermal (+72.2% YoY), 5.9GW hydro (+1.0% YoY) and nil in nuclear. Accumulated investment in power generation capacity was Rmb428.8bn as of July, +3.4%YoY. Accumulated investment in power grid was Rmb331.5bn during the same reporting period, +12.5%YoY. (Citi, August 2025)

Stock Comments

LONGi Green Energy: The company’s net loss in 1H25 was narrowing down to Rmb2.6bn vs Rmb5.2bn in 1H24. China is pushing anti-involution in solar sector to reduce overcapacity and loss-making. People expect Longi would be one of the key beneficiaries despite weak fundamentals right now. (Company data, Mirae Asset, September 2025)

Sungrow Power Supply: Similar as Longi for anti-involution. Additionally, the company delivered a very strong 1H25 results with revenue up by 40%YoY and net profits up by 56%YoY, driven by fast growing ESS demand in and outside China. (Company data, Mirae Asset, August 2025)

NAURA Technology: The company is one of the key beneficiaries from China’s semiconductor capex in the long term. The company’s 1H25 results were actually miss street estimations. Top line grew by 29.5%YoY, while bottom. (Company data, Mirae Asset, September 2025)

NARI Technology: Nari’s 1H25 results were better than initial guidance, with bottom line up by 8%YoY, 2% higher than guided. Grid and renewable businesses grew by nearly 30%YoY, while exporting business are more than doubled. However, people are worried about China’s power grid capex slowdown. (Company data, Mirae Asset, September 2025)

Preview

The top-down anti-involution reform is now playing a critical role to assist renewable industry self-discipline and sustainable growth. 2026 is the first year of the fifteenth five-year plan. We expect renewable installation may not decelerate on the back of China’s power consumption growth in the long term, driven by electrical vehicles, residential demand, data center and industrial/manufacturing demand. If people can ultimately find out a way to reduce utilization and increase profitability, we will see the sector bottom out from here.

Global X China Consumer Brand ETF (2806)

Sector Update

China Retail sales growth decelerated to 3.7% YoY in July (vs. +4.8% YoY in June), below market consensus of +4.6%. The 1H25 earnings season reiterated a persistent theme of the past months: a divergence between muted broad consumption and robust growth in “new consumption” categories. Key outperformers included RTD beverages (notably sugar-free tea, energy, and sports drinks), freshly-made tea & coffee, snacks like konjac, outdoor sports, emotionally-driven products, and discount retail channels. Within new consumption names, investor interest in Pop Mart (9992 HK) remained elevated following its earnings call, which unveiled the new Mini Labubu. The product has been a positive surprise and could expand the IP’s application to new use cases like mobile phone charms. Meanwhile, ASP declines continuously to weigh on restaurants and beverages (especially bottled water) under deflation environment. Sportswear names experienced a beta-driven grind higher on low expectations. However, this trend reversed following weak 3Q sales commentary from both Li Ning and Anta, which triggered a sector-wide pullback. (Mirae Asset, August 2025)

Stock Comments

Pop Mart (9992 HK): Pop Mart achieved 30% return in August. The company strong 1H25 results with sales/NP up 204%/397% YoY. This growth was fueled by a significant global expansion, with overseas sales mix now contributing 40% of the total. Sales surged across all regions, particularly in the Americas (+1142%), Europe (+729%), and APAC (+258%). Within Greater China, which saw a 135% increase, growth in Hong Kong, Macau, and Taiwan outpaced that of the mainland. IP wise, Labubu represented 35% of 1H25 sales, while Molly/Skullpanda/Dimoo/Crybaby in total accounted for another 35%. Notably, Crybaby (9% of 1H sales) and Twinkle Twinkle (3% of 1H sales) demonstrated strong demand and were likely to pick up in sales contribution. (Company data, Mirae Asset, September 2025)

Trip.com (TCOM US): Trip.com recorded 18% return in August. The company reported an all-round beat results in 2Q25, with net revenue up 16% YoY to Rmb14.8bn. Profitability was a key highlight, with an operating margin of 31.4% significantly exceeding guidance of 29.1%, bringing Non-GAAP operating profit up 10%YoY to Rmb4.7bn. Furthermore, the company announced a new share repurchase program of US$5bn in August. (Company data, Mirae Asset, September 2025)

Li Auto (Li US): Li Auto experienced 12% loss in August following a disappointing 2Q25 results and weak 3Q guidance. The company delivered 4.5%/1.8% sales/GP YoY decline in 2Q, largely in-line with consensus, but operating profit missed due to higher R&D expenses. 3Q25 guidance was below consensus, with guided vehicle sales volume of 90k-95k units and revenue of Rmb24.8bn-26.2bn both down 41-42% comparing to the midpoint of consensus. (Company data, Mirae Asset, September 2025)

Preview

We believe policy stimulus remains key to enhancing consumer sentiment and bolstering stock performance for China consumer in 2025. During the Two Sessions, consumption was reaffirmed as a primary policy focus, and the introduction of the Special Action Plan to boost consumption underscores this commitment. Amid escalating trade tensions, China government may accelerate the pace and scale of these policies. We expect that macroeconomic recovery, supported by policies and the stabilization of the property market, presents the largest upside potential for China consumer sector in 2025. Among subsector, we favour those that are directly targeted by stimulus policies, such as home appliance and EV under extended consumer goods trade-in programs, as well as sectors sensitive to macroeconomic changes, such as Baijiu, catering and beverage.

Global X China Robotics and AI ETF (2807)

Sector Update

The China State Council has announced an artificial intelligence plus action plan recently that promotes the application of artificial intelligence technologies, targeting a 90% application rate by 2030. We will see more policy details to follow in terms of specific measures and targets. On the manufacturing side, the plan is aimed at speeding up the commercialization of AI technologies such as humanoid robots and autonomous logistics, which are restricted by high production and R&D cost, legislation and many other factors now. (Mirae Asset, September 2025)

The general China factory automation demand is bottom out from OEM segments including lithium battery, electronics, auto and industrial robotics, while process automation such as petrochemical and chemicals industry remained sluggish. The sector’s outlook has shifted decisively upward, with some leading companies delivering strong sales and earnings results in 1H25, much better than feared at the early of the year. Chinese leading companies, such as Inovance, Leader Drive, Shuanghuan, keep gaining market share thanks to growth in lithium battery and logistics industries. (Mirae Asset, September 2025)

Stock Comments

Horizon Robotics: The company’s shipment and margins are expected to improve in 2H25, thanks to more sales from key customers and increasing penetration to new automakers. The 1H25 results ended at 68%YoY revenue growth and the net loss Rmb5.2bn due to high R&D cost, but management shared they would improve the profitability with fast volume growth to reduce the R&D D&A cost going forward. (Company data, Mirae Asset, September 2025)

Huagong Tech: The company is one of the key beneficiaries from 800G optical module domestic production and semiconductor imports substitution. The company also delivered solid 1H25 results with revenue up by 45%YoY and net profits up by 45%YoY driven by strong order growth in all segments. (Company data, Mirae Asset, September 2025)

Shenzhen Inovance Technology: The company’s order intake was reaccelerating in July and August with double digits growth. Demand from logistics and heavy machines, lithium battery and autos, F&B and some traditional industries are quite strong, which are not impacted by the tariff headwinds. The company also delivered much better than expected 1H25 results with top line up by 27%YoY and bottom line up by 40%YoY. (Company data, Mirae Asset, September 2025)

WeRide Inc: The company delivered 33%YoY revenue growth in 1H25 and the net loss was a little narrowing down. WeRide is partnering with Uber to offer robotaxi services beyond China and the United States. (Company data, Mirae Asset, September 2025)

Preview

Robotics, AI and automation are one of the key beneficiaries from both China’s stimulus measures in the near term and the economy transition goal in the long run. We expect the monetization of humanoid robots in industrial, transportation and residential scenarios to accelerate going forward, driven by large amount of bottom-up R&D investment and continuously cost cutting. We may see some leading companies to deliver material fundamental changes in the coming twelve months.

Global X Hang Seng TECH ETF (2837)

Industry Update

Global X Hang Seng TECH ETF (2837) recorded positive return in August. Semiconductor stocks (SMIC, Hua Hong Semi) led the gain as domestic substitution theme prevails on news that Nvidia planned to halt H20 production and Deepseek launched new model targeting domestic chips. Some EV companies performed well thanks to solid demand of new models. Food delivery platforms continue to underperform as intense competition continue to weigh on profitability. With a clear change in policymaker stance, the gradual rollout of stimulus policies could support a revived consumer sentiment that will benefit sectors including ecommerce, advertising, EV, and 3C electronics. Online gaming sector remains less macro-dependent and continued to record solid revenue supported by high quality games.

Stock Comments

SMIC recorded 19% return in the month, a key contributor to the ETF. 2Q result was a slight beat. Utilization rate remains high with solid order ahead. Share price is bolstered by the strong domestic substitution demand for China Semi sector. The company’s long-term outlook remains solid driven by local fabless customers’ growing demand. (Company data, Mirae Asset, August 2025)

Meituan recorded -16% return in the month, a key detractor to the ETF. 2Q25 earnings missed market expectation due to intense competition. The competition is likely to extend into 3Q25 and continue to weigh on the company. (Company data, Mirae Asset, August 2025)

JD Health recorded 25% return in the month. The company reported strong 2Q25 results due to continued strength in drug sales (30% YoY in 1H25), under policy tailwinds that propel online drug sales. JD Health also raised its 2025 revenue target to 20% YoY (from previous mid-teens %). (Company data, Mirae Asset, August 2025)

Xiaomi reported in-line 2Q25 results in August. 2Q Revenue of Rmb116bn was 31% YoY, in-line with consensus estimates. Across core business, EV (>2x YoY) and AIoT (+35% YoY) growth was the brightspot, while Smartphone revenue was down 2% YoY mainly due to the decrease in ASP. Adj. Net profit grew +75% YoY and was higher than consensus, thanks to solid profitability for EV and other new initiatives segments. With the solid EV demand and orders in the past several months, the key driver for Xiaomi will shift to capacity rampup and delivery. For EV segment, increased contribution from high-end models with higher ASP (SU7 Ultra and YU7) could continue to improve profitability. (Company data, Mirae Asset, August 2025)

Preview

Hang Seng TECH Index constituents are well positioned to benefit from the policy stimulus by central government. We see unique positioning of Hang Seng TECH Index thanks to its undemanding valuation, ongoing margin expansion, and continued ramp up in shareholder returns. With well-established ecosystem containing large user base and leading technology in place, we see further upside potential for these leading technology companies coming from the rapid development of structural growth themes such as EV, Semiconductor and AI in China.

Global X China Little Giant ETF (2815)

Industry Update

China Little Giant ETF gain positive return in the month. China A share market is supported by abundant liquidity, solid 2Q25 real GDP growth, and expanded policy support, both on the supply side (anti-involution) and the demand side. Small-mid caps are benefiting more from abundant liquidity. We still expect promoting emerging industries to climb up technology tree and supporting domestic substitution remain policies priorities in 2025. Therefore, these specialized and sophisticated SMEs play a crucial role in China’s transition to high quality development. (Mirae Asset, August 2025)

Stock Comments

Suzhou TFC Optical returned 87% in the month, a key contributor to the ETF. The company reported 1H25 results, with revenue of Rmb 2.46bn, +58% YoY; Net income Rmb 899mn, +37% YoY. The company is a leading CPO company in China, benefiting from the rising AI computing power demand. (Company data, Mirae Asset, August 2025)

Rockchip Electronics returned 52% in the month, a key contributor to the ETF. The stock is supported by the positive sentiments around China semiconductor sector. (Company data, Mirae Asset, August 2025)

Shanghai Bochu returned 16% in the month. The company reported in-line 2Q25 results, with revenue growing 21% YoY to Rmb608mn, net profit growing 29% YoY to Rmb386mn. The company expects solid overseas sales growth at 30%~40% going forward, emphasising more aggressive overseas expansion plans with stronger demand in Brazil, Southeast Asia, and Turkey. (Company data, Mirae Asset, August 2025)

Preview

As a high-quality, small-cap fund, Global X China Little Giant ETF is likely to benefit from government’s supportive policies on tech innovation and may outperform large-cap funds if the economy turns to recovery in 2025. SMid is likely to outperform given abundant liquidity in China A Share