Important Information

Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- The investment objective of Global X FTSE Greater China ETF (the “Fund”) is to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the FTSE MPF Greater China Index.

- The Fund is exposed to concentration risk by tracking a specific regions or countries.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

Market Commentary

Global X FTSE Greater China ETF (3470)

Taiwan Market

Taiwan semiconductor stocks continued strong performance in 4Q25, on the back of resilient AI demand. With tight capacity expected to persist through 2027 due to the continuous growth in token consumption leading to a demand-supply imbalance, leading foundries are poised to witness accelerated revenue and capital expenditures. TSMC’s enhanced revenue streams are expected to be supported by the migration of AI GPUs/ASICs from 5nm to 3nm, with both nodes projected to operate at full capacity in 2026 and 2027. (Company data, January 2026) Furthermore, higher gross margin could become a consistent feature, driven by productivity enhancements and minimal dilution from overseas fabs. Leading foundries’ revenue growth is also underpinned by the robust demand for leading-edge nodes, with a focus on tight 3nm/5nm utilization and the acceleration of 2nm adoption. (Mirae Asset, January 2026)

Taiwan’s semiconductor sector could maintain its outperformance into 2026 driven by sustained, massive AI infrastructure spending from cloud providers, which is creating an extended semiconductor upcycle through 2027. A critical resulting bottleneck and primary beneficiary is the memory sector, where severe undersupply is expected to drive significant price hikes, benefiting memory makers but pressuring system company margins and capping growth in non-AI consumer segments like smartphones, which face shipment declines due to these cost increases. Within the AI boom, ASICs could perform better over GPUs due to higher growth and broader adoption, with sustained semiconductor capital expenditure growth as foundries and memory makers race to expand capacity to meet this demand. (Mirae Asset, January 2026)

HK/China Market

Hong Kong Market recorded certain level of consolidation in 4Q after strong 9M25 gains. Key reasons for the correction include the escalation and de-escalation of US-China trade tensions in October, intensified price competition in quick commerce space, investor profit taking, and global market uncertainty (caused by rapid swings in Fed rate cut expectations, liquidity drain due to US government shutdown, and the heated AI bubble debate). We see style rotation amid risk-off sentiments from growth to value, leading to outperformance of high dividend stocks against technology stocks in 4Q. China A-Share market performed better, with CSI300 closing flat in 4Q supported by abundant onshore liquidity, solid 3Q earnings, and targeted policy supports. Both Hong Kong market and China A-Share concluded 2025 with its most impressive one-year performance since 2021. Notably, the technology, internet, and renewable energy sectors emerged as the top performers, capitalizing on advances in artificial intelligence and support from anti-involution initiatives. Conversely, consumer and property sectors lagged behind, primarily attributed to subdued macro conditions and a persistent downturn in the property market. (Bloomberg, Mirae Asset, January 2026)

- Internet and AI: China’s internet sector underperformed in 4Q mainly due to the worsening profitability for transaction platforms amid intensified quick commerce price war and slow consumption recovery. Internet companies reported divergent 3Q results, with ecommerce/local service platforms recording significant profit decline while others recorded in-line top and bottom line growth. Notably the cloud revenue growth for hyperscalers remains robust on the back of strong AI demand. Advertising and gaming business for leading companies are also largely stable. This divergence in performance may persist into 2026, with cloud services expected to maintain their strong momentum while the growth of ecommerce/local services revenue could face challenges. AI continues to be a key theme and driver for the internet sector, with leading companies set to be key beneficiaries. In addition to their cloud business which already seen growth driven by very strong AI inference demand, hyperscalers continue to be drive the iteration of their frontier AI models and agentic capabilities, which could be well integrated into their core business and support ecosystem growth. (Mirae Asset, January 2026)

- Semiconductor: Albeit with certain level of correction in 4Q, semiconductor remains one of the best performing sectors in 2025 driven by AI and localisation. China’s semiconductor ecosystem is becoming increasingly richer by the day. Recently, fabless companies specializing in AI accelerator design, such as Moore Threads, MetaX, and Biren, have gone public, and large-scale model (LLM) companies like MiniMax and Zhipu are also listing. These rapid listings by fabless companies may mean intensified competition for existing index constituents like Cambricon. However, they are also positive in that the funds raised from capital markets serve as a driving force for reinvestment in the overall semiconductor ecosystem. In particular, since the China Semiconductor Index heavily relies on equipment and foundry companies, the increased listing of fabless companies, which are downstream industries, will create a favorable environment for our index constituents. Risk Factors: Recently, concerns have been raised about the possibility of allowing imports of the NVIDIA H200 into China, raising concerns about a contraction in the Chinese AI chip industry. However, with the Chinese government expected to implement a “quota system” to manage the ratio of domestic and foreign chips, the growth of the local ecosystem is expected to continue. (Company data, Mirae Asset, January 2026)

- Humanoid Robot : NVIDIA’s announcement of new open models, frameworks and AI infrastructure for physical AI in CES 2026 further boosts sector sentiments. Orders for Chinese humanoid robot integrators ramped up rapidly in 2H25, totalling over Rmb2bn from 3 key areas: 1) industrials, 2) commercial services, and 3) data collection centers (mainly gov’t-backed projects). Many companies have optimistic target for 2026, with industry-level delivery potentially reaching 100k. The increasing adoption across industries, sophisticated local supply chain (covering >90% of components), and strong government push (humanoids mentioned in the 15th FYP as a ‘strategic emerging sector’) should support its long term development in China. Furthermore, Trump administration is also preparing to announce an executive order on robotics, “All in robots”, after AI push. As a result, Asia robotics companies including some Chinese leading robot-related companies rallied a lot, especially those closely tied to the US value chain. (Company data, Mirae Asset, January 2026)

- Consumer: Retail sales data remain relatively weak over past months. China consumer sector has been muted and lagged behind the performance of China broad market in 2025. Reviewing the historical performance of the consumer sector during the bull markets (such as: 1999–2001, 2005–2007, 2014–2015, and 2019–2021), a notable trend emerges: China consumer sector’s notable rallies all occurred when economic fundamentals began to recover. This suggests that the consumer sector typically thrives in the post-cyclical phase. The revival of consumer spending is largely dependent on improvements in household employment and income, stabilization of asset prices, the emergence of new drivers for the “wealth effect,” and an overall recovery in the macroeconomic environment. Currently, a sluggish macroeconomic landscape continues to dampen consumption demand, indicating that a fundamental recovery may take longer than anticipated. In 2025, IP merchandise segment is one of the top-performing areas within the consumer sector. Leading IP companies are projecting a CAGR of over 20% in sales and earnings for the next three years, while most traditional businesses are expected to see single-digit sales growth coupled with margin improvements. One good news is the release of extended trade-in policy by central and local governments at end-2025. Looking ahead to 2026, policy support is likely to intensify in the new year, with an expected shift in focus toward service-sector spending rather than big-ticket goods. (Mirae Asset, January 2026)

Global X FTSE Greater China ETF (3470)

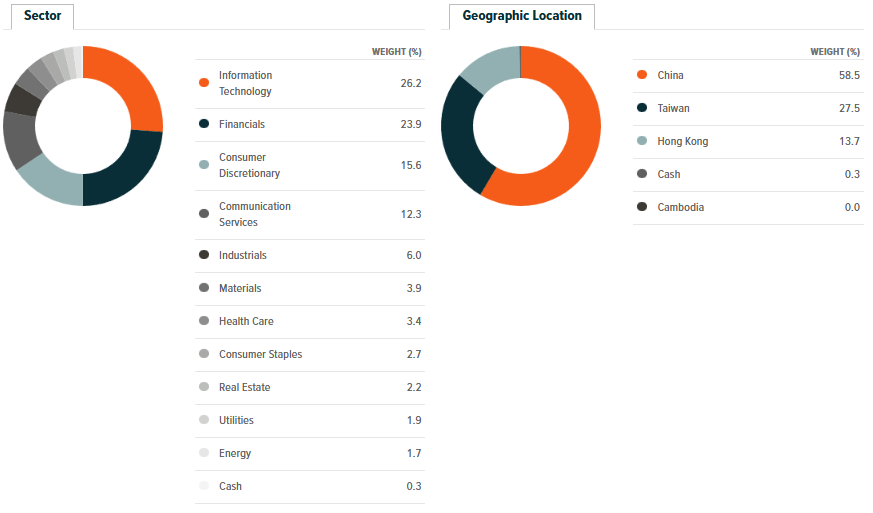

Asset Allocations