Japan Market 2025: Fundamentals Intact

Despite a volatile performance over the past few months due to currency, political, and global/US economic uncertainty, Japan market still managed to delivered 19% return (represented by Nikkei 225, in JPY terms, as of 5 Dec) on the back of recovering macro environment and solid corporate earnings. Looking beyond near term headwinds including Yen volatility, domestic political uncertainty and potential US tariff, we remain constructive on Japan market performance in 2025 as bolstered by domestic reflation, resilient exports, solid corporate earnings growth momentum, and ongoing capital market reforms. JPY is set for a modest appreciation going forward driven by the divergence in direction of monetary policy between US and Japan.

A Normalized Japan Economy –

Wage Growth, Reflation, Recovering Domestic Demand, and Resilient Export

In FY24 Shunto Spring Wage negotiation, Japan Union Group Secured over 5% wage hike for 2024, the heftiest pay hikes in 33 years. The wage hike is entrenched throughout the year, with real wage growth turning positive for the first time in 27 months in June. Looking ahead, wage hikes should be sustained in 2025 as supported by labor shortage and ongoing efforts by government, labor, and management to hike wages. Wage hike level for FY25 Shunto Spring Wage negotiation could be similar to FY24 level as The Japanese Trade Union Confederation announced its 2025 overall wage hike target at “at least 5%).

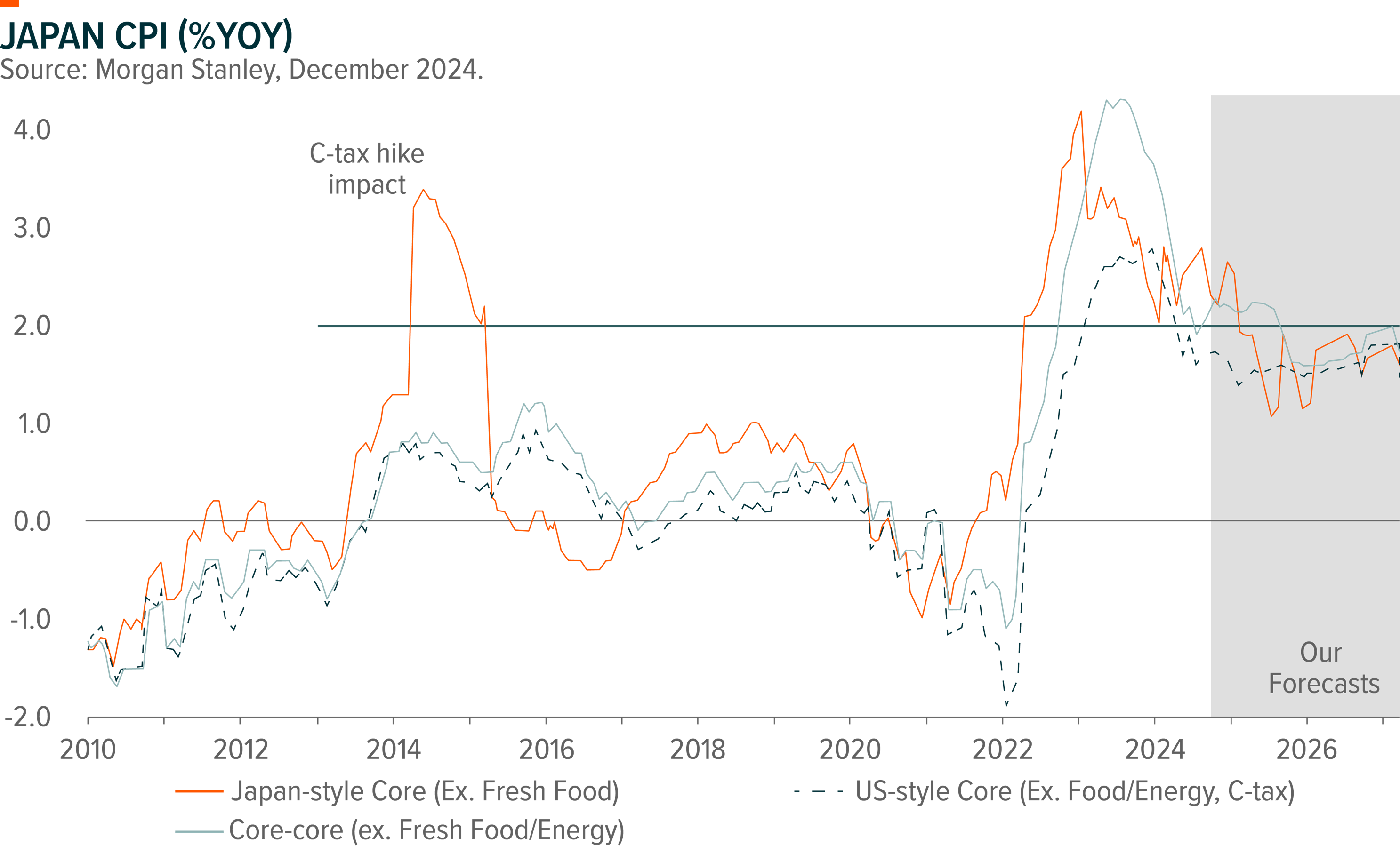

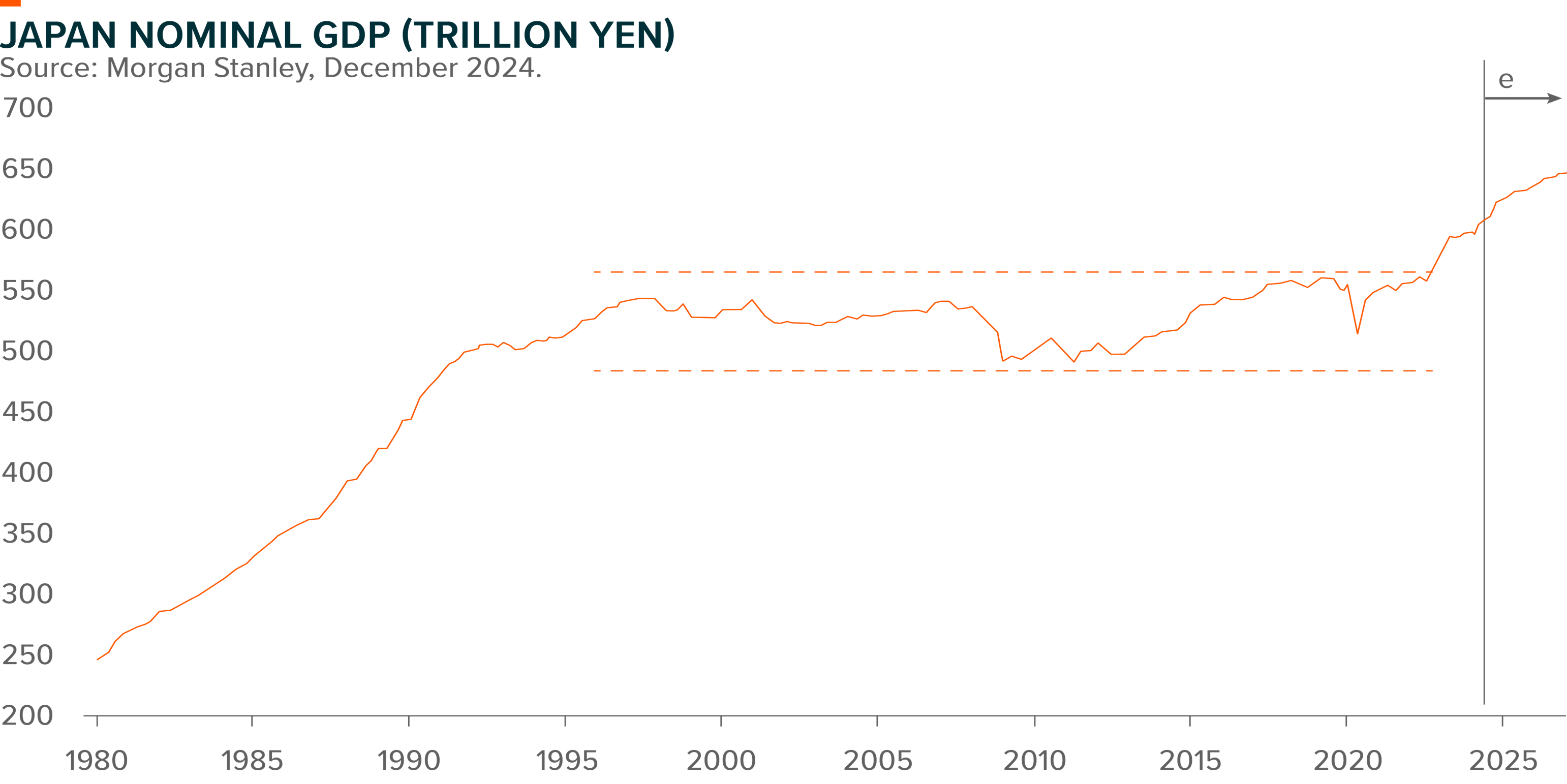

The highest wage hike in three decades could support a sustainable inflation. A virtuous wage-price cycle is in the making, as 1) with the rise in employee wages, corporates tend to increase product/services prices to pass through the costs to consumers; and 2) Consumer spending should be boosted by higher income and income expectation. Japan inflation returned to above 2% level in 2022 – 2024 amid a global inflationary environment and inflationary pressure from import prices under Yen depreciation. Although Energy-related subsidies and some food price increases affects the visibility of pricing trends, Japan’s core CPI inflation should remain at around 2% level as supported by wage hikes and changes in corporate price-setting pattern. Inflation pick up also supports the reacceleration of Japan’s Nominal GDP growth to the highest level in past decades.

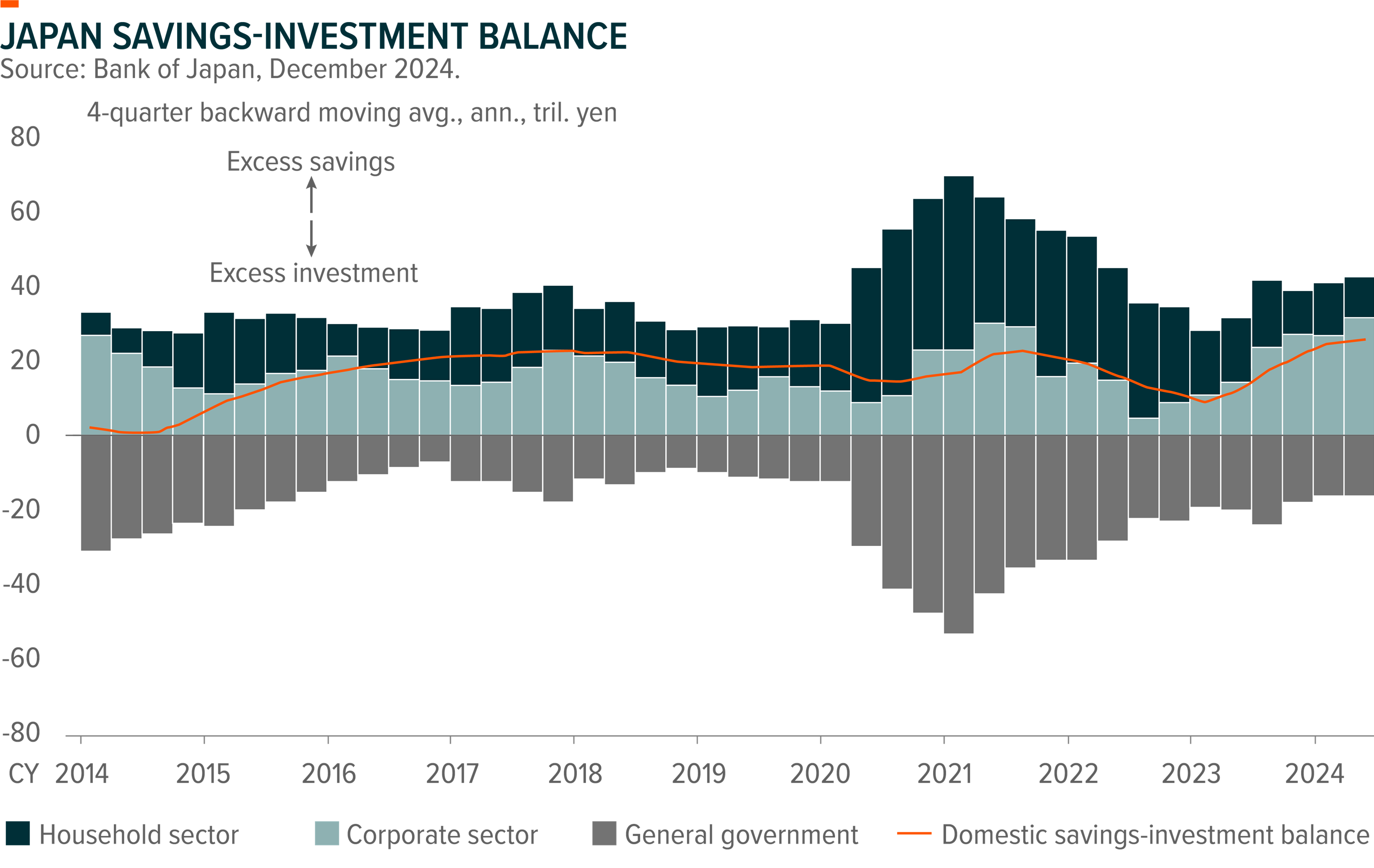

A reflationary Japan economy has positive implication on capital market as it supports revitalized domestic demand and could potentially affect Japan household’s saving patterns. Covid-19 catalysed Japan consumers’ saving behaviour, leading to c.US$500bn in excess savings during the pandemic. The gradual transition towards mild inflationary mindset from deflationary mindset over the past 30 years could potentially unlock the wealth pool and fuel consumer spending. In addition, Japanese household could increase their historically low allocation into equity market in an inflationary economy and incentivized by the new Nippon Individual Savings Account (NISA) scheme. A shift in consumer mindset and the rise in income expectation should drive domestic demand recovery and support Japan market performance.

Japan’s export recorded three consecutive years of growth reached historical high level in 2023 on the back of Yen weakness. Despite Yen fluctuation in 2H24, Japan’s export recorded 7% growth YTD (as of Oct 2024), demonstrating the strong competitiveness of Japan’s high-end products. Looking ahead, Japan’s export could continue growth momentum in 2025 as driven by Japan’s auto production normalization and semiconductor-related exports growth amid US economy soft-landing and continued moderate growth in the global economy. Potential recovery of China economy under policy supports present upside opportunities as Japan exports to China has been more closely linked to overall manufacturing activity in China since the COVID-19 pandemic. However, potential US tariff under Trump administration casts downside risks to Japan exports through decline in Japan goods price competitiveness and decline in demand for Japan goods as a results of higher US inflation. Japan exports could see acceleration in 1Q25 as a result of rush demand before US tariff.

Corporate Earnings Growth to Accelerate

An inflationary economy supports a better corporate earnings growth outlook as price hikes, along with volume improvement under domestic demand recovery, should drive an accelerate in revenue growth. The price pass through from corporate to customers also led to upward trajectory in profit margin since Covid. In local currency terms, Japan corporates recorded robust EPS growth over the past decade thanks to the loose monetary policy and strong product competitiveness. Solid earnings growth should provide sound foundation for stock market performance.

Corporate Governance Reform Start Bearing Fruits

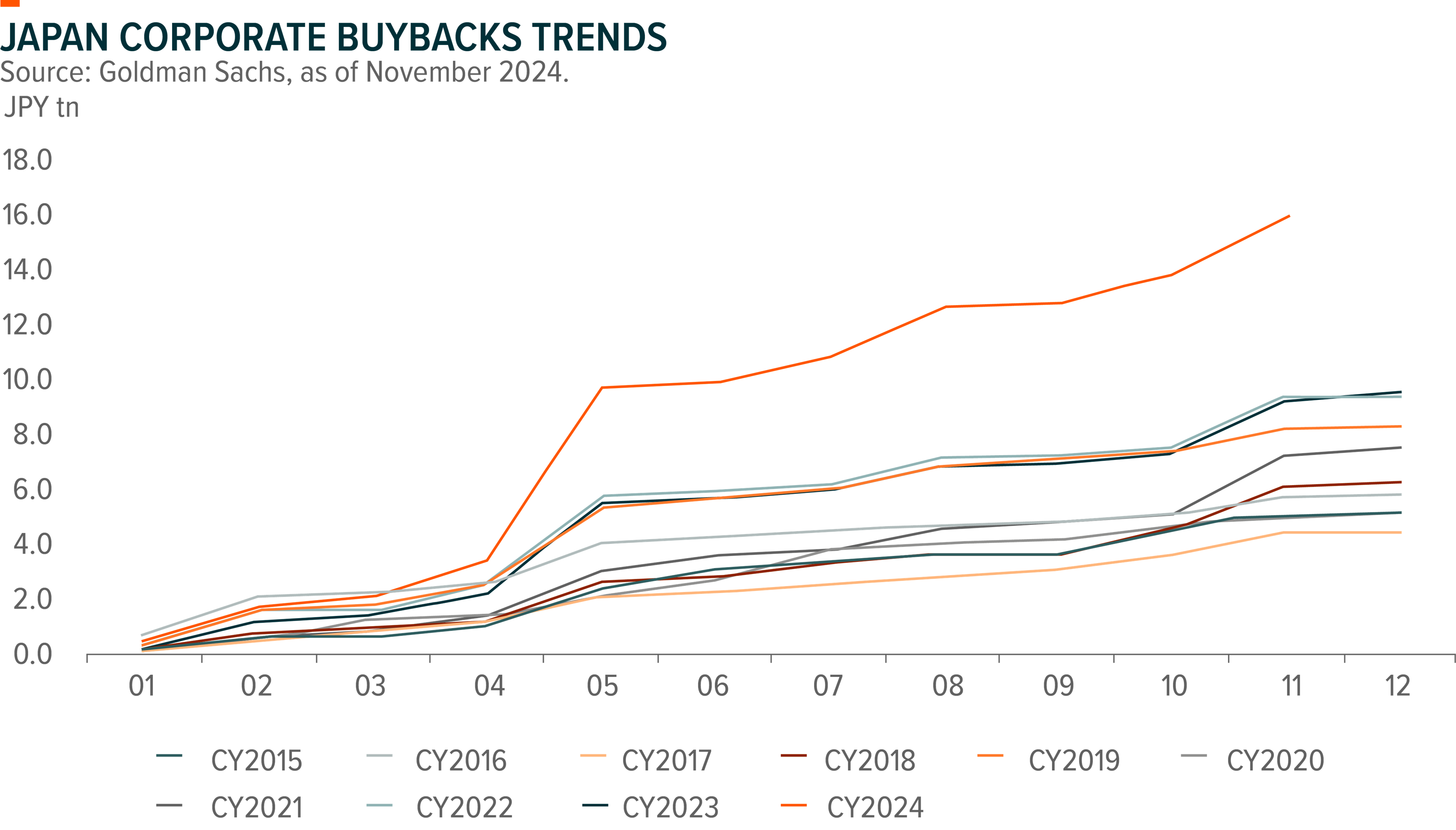

Corporate Governance Reform led by TSE improves the overall quality and shareholder friendliness for Japan listed companies. Initiated in early 2023, TSE reforms expands its focus from enhancing corporate disclosure to improving corporate quality through unwinding cross-shareholding unwind, improving ROE, and increasing shareholder returns. As a result, corporate buybacks increased significantly in 2024, and companies with higher disclosure quality have performed better than those that have not.

JPY – Modest Appreciation Ahead

JPY is set for a modest appreciation in 2025 driven by the divergence in direction of monetary policy between US and Japan. A more sustained wage growth and inflation pattern should support further BOJ rate hike to 0.75% in 4Q25 (Bloomberg consensus data). In addition, the recovery in trade surplus could also support JPY from supply-demand perspective. However, the still negative real policy rate limits further appreciation for JPY. Stickier US inflation under potential Trump tariff could also slow down the pace of rate cut in the US. JPY will appreciate modestly to 147 in 4Q25, and 140 in 2026, from 150 currently, according to Bloomberg consensus. In a JPY appreciation environment, unhedged ETFs is poised to outperform, as the impact on corporate earnings is manageable and the currency appreciation can be positive for dollar-denominated returns for unhedged products. See our previous Unhedged ETFs Set to Outperform Amid Yen Appreciation.