Important Information

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X Innovative Bluechip Top 10 ETF (the “Fund’s”) seeks to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Mirae Asset Global Innovative Bluechip Top 10 Index (the “Index”).

- The Index is a new index. The Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history. The Index is an equal weighted index whereby the Index constituents will have the same weighting at each rebalancing (but not between each rebalancing) regardless of its size or market capitalisation based on the methodology of the Index.

- The Fund’s investments are concentrated in companies with a technology theme. Many of the companies with a high business exposure to a technology theme have a relatively short operating history. Technology companies are often characterised by relatively higher volatility in price performance when compared to other economic sectors. Companies in the technology sector also face intense competition, and there may also be substantial government intervention, which may have an adverse effect on profit margins. Rapid changes could render obsolete the products and services offered by these companies. These companies are also subject to the risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences.

- The Fund’s investments are concentrated in companies in the technology sector. The Fund’s value may be more volatile than that of a fund with a more diverse portfolio. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the technology sector.

- The number of constituents of the Index is fixed at 10. The Fund by tracking the Index may have a more concentrated investment portfolio than it would have held if tracking an index with a higher number of constituents, leading to higher risks of volatility.

- Underlying investments of the Fund may be denominated in currencies other than the base currency of the Fund. In addition, the base currency of the Fund is USD but the trading currency of the Fund is in HKD. The Net Asset Value of the Fund and its performance may be affected unfavourably by fluctuations in the exchange rates between these currencies and the base currency and by changes in exchange rate controls.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- The trading price of the Units on the SEHK is driven by market factors such as the demand and supply of the Units. Therefore, the Units may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Unit of the Fund and will reduce the capital available for future investment.

Innovative Bluechip Top 10 ETF – Investing in the Global Disruptors

Global X Innovative Bluechip Top 10 ETF (3422 HK) invests in 10 leading technology companies across 4 mega trends – AI, Semiconductors, Electric Vehicles, and Biotech, offering compelling opportunity for investors to capitalize on disrupting technology developments globally. In this article, we dissect the investment cases for 6 companies – 1) Nvidia; 2) TSMC; 3) Eli Lily; 4) Novo Nordisk; 5) BYD; and 6) CATL, and discuss the competitive moats that established them as global leaders. We will follow with the next episode on the remaining 4 companies in the ETF – Microsoft, Amazon, Alphabet, and Apple.

1) Nvidia and 2) TSMC: Shovel-makers in the AI Gold Rush

Nvidia Competitiveness Analysis

Nvidia initially focused on developing high-performance graphics processing units (GPUs) for the gaming market, leveraging its expertise in graphics processing to establish a strong presence in the industry. Over time, Nvidia successfully diversified its product portfolio to cater to data center applications and other professional graphics processing.

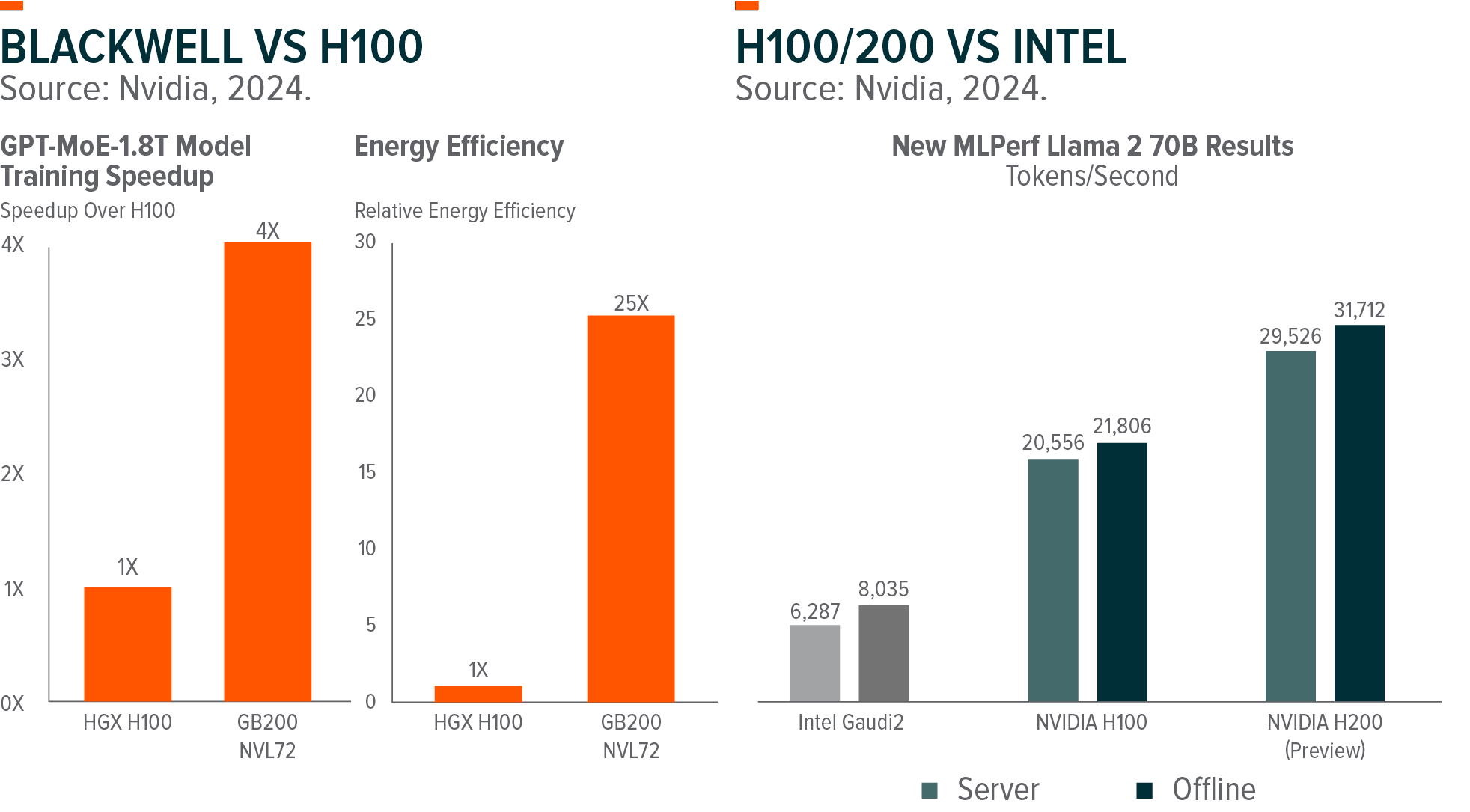

In our view, Nvidia’s dominance in AI chips is built on superior performance ultimately offering the lowest cost solution for customers to train and deploy AI models. In training, Nvidia has a significant lead over its competitors built on 1) superior cluster training performance thanks to technology leadership in chip-to-chip connection. This enabled high-bandwidth inter-chip connection to maximize training performance and efficiency. 2) CUDA and Nvidia’s software ecosystem are deeply integrated with existing AI development processes and software. The NVIDIA CUDA Toolkit provides a development environment for creating high-performance, GPU-accelerated applications.

TSMC Competitiveness Analysis

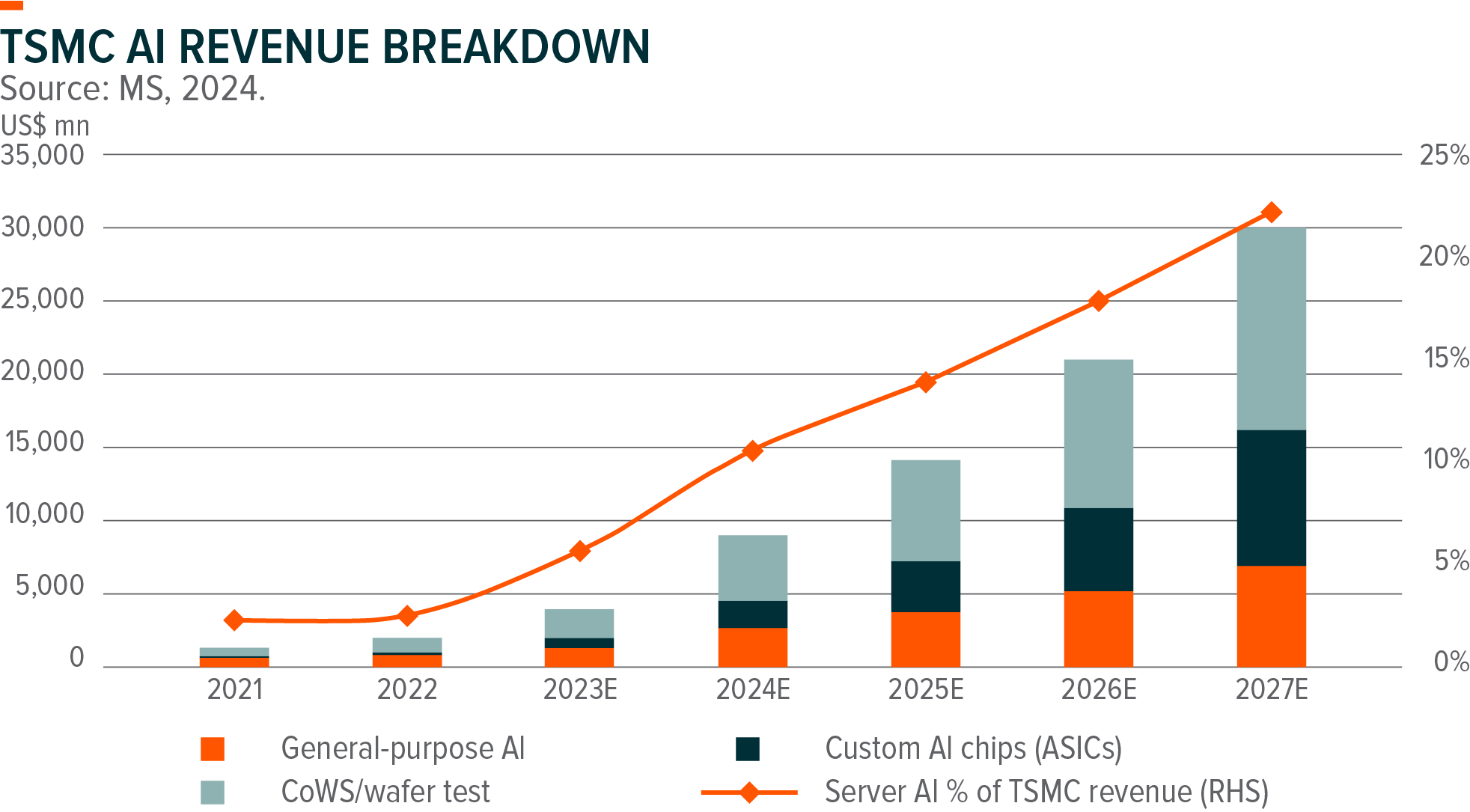

TSMC is the world’s leading independent semiconductor foundry, specializing in the manufacture of advanced integrated circuits (ICs) for a wide range of applications, including smartphones, high-performance computing, automotive, and Internet of Things (IoT) devices. TSMC’s business model is based on a pure-play foundry strategy, where the company focuses solely on manufacturing ICs for its customers, without designing or selling its own branded products. This approach allows TSMC to maintain a neutral position in the industry, enabling it to work with a diverse range of customers, from fabless semiconductor companies to integrated device manufacturers (IDMs).

TSMC’s leadership in advanced process nodes has created a significant gap between the company and its competitors, including Intel and Samsung. Following the 5nm node, TSMC has maintained a clear advantage in transistor density and performance at the same node, while also excelling in production yield and volume ramp execution. As a result, key customers such as Qualcomm and Nvidia have shifted a substantial portion of their product portfolios from Samsung Foundry to TSMC. We do not anticipate competitors closing this gap in the near term, as the majority of leading chip roadmaps are designed to be manufactured on TSMC process nodes. Notably, Intel’s latest client PC platform, Lunar Lake, is entirely outsourced to TSMC, underscoring the company’s technology leadership. We expect TSMC’s competitive advantage to widen over the next few years, driven by its continued innovation and execution excellence, and remain confident in the company’s outlook until meaningful improvements are made by its competitors.

![]()

3) Eli Lily and 4) Novo Nordisk: A Duopoly in the Obesity Medication Market

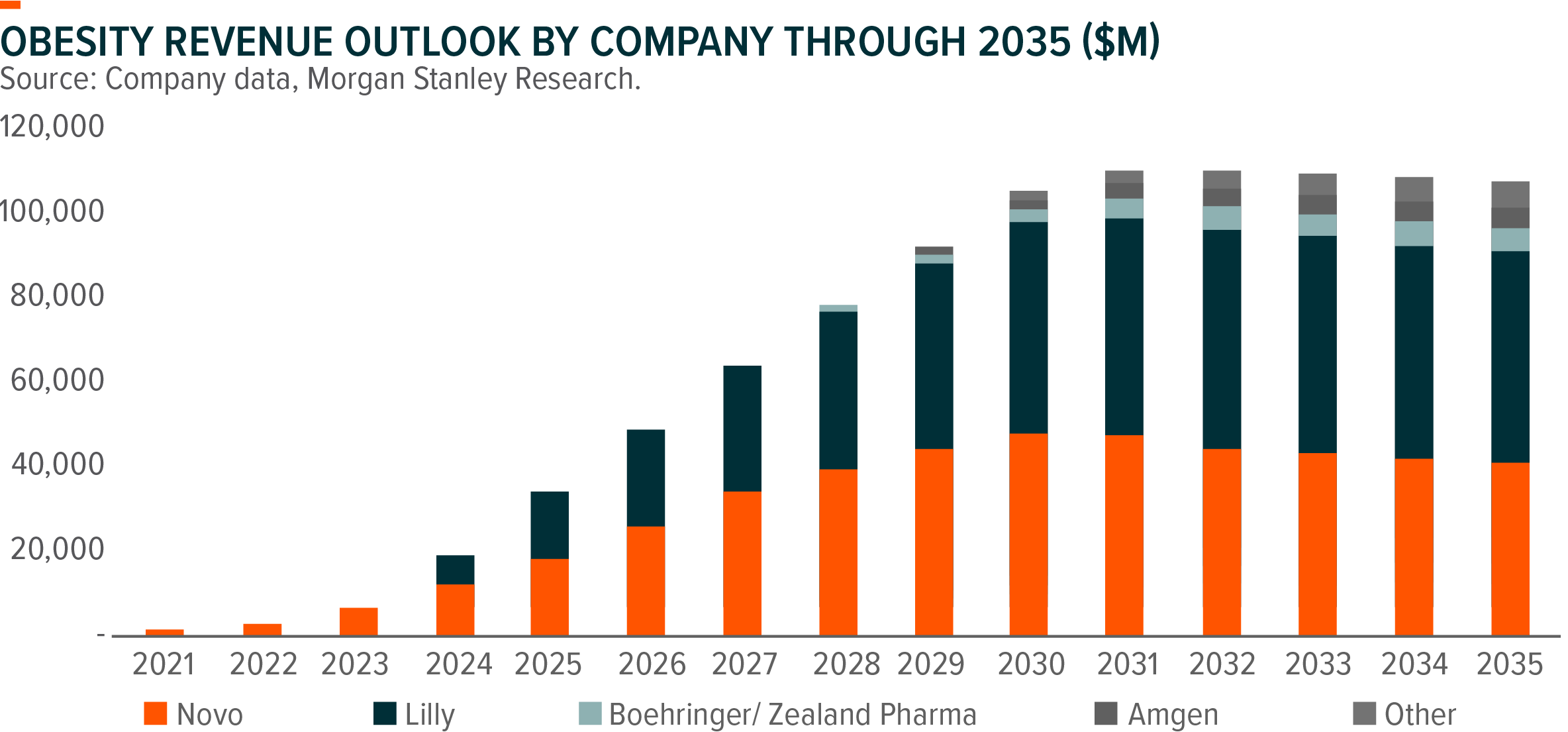

Currently, more than a billion people around the globe are affected by obesity, and 54% of adults will be overweight or obese by 2035. This rising global prevalence of obesity, coupled with the expanding use of obesity medications for related chronic diseases, presents substantial growth potential for the obesity market, which is anticipated to exceed $100bn by 2030. GLP-1 is the leading treatment in this space, with Novo Nordisk (NVO US) and Eli Lilly (LLY US) positioned as two major players. We believe these two companies will continue to dominate the market for the foreseeable future with 80%+ shares combined, primarily supported by their robust pipelines and significant capital expenditures.

For investors looking to capitalize on opportunities within the obesity market, the Global X Innovative Bluechip Top 10 ETF (3422 HK) offers a strategic investment avenue, with Novo and Lilly making up approximately 20% of the fund’s holdings.

Rosy Outlook of Obesity Medication: $100bn+ Market by 2030

The global prevalence of obesity has more than doubled since 1990, according to WHO. Currently, over a billion people worldwide are living with obesity, and 54% of adults are expected to be overweight or obese by 2035, up from 38% in 2020 (World Obesity Atlas 2024). Obesity is a significant contributor to more than half of all diabetes cases and is linked to over 200 other chronic conditions. The increasing rates of obesity, combined with rising life expectancy, suggest a growing financial burden on healthcare systems. This underscores the importance of early screening and prevention strategies.

GLP-1 is becoming a major treatment option in this arena and have demonstrated high efficacy and safety. Initially approved for diabetes management, injectable GLP-1 medications have been shown to help individuals lose 15-25% of their body weight by reducing appetite.

In 2023, sales of branded obesity drugs reached $6 billion. The global obesity market is expected to exceed $100 billion by 2030, driven by increasing adoption rates, extended treatment durations, and enhanced supply chains.

Wide Applications Beyond Weight Loss with Huge Potentials Ahead

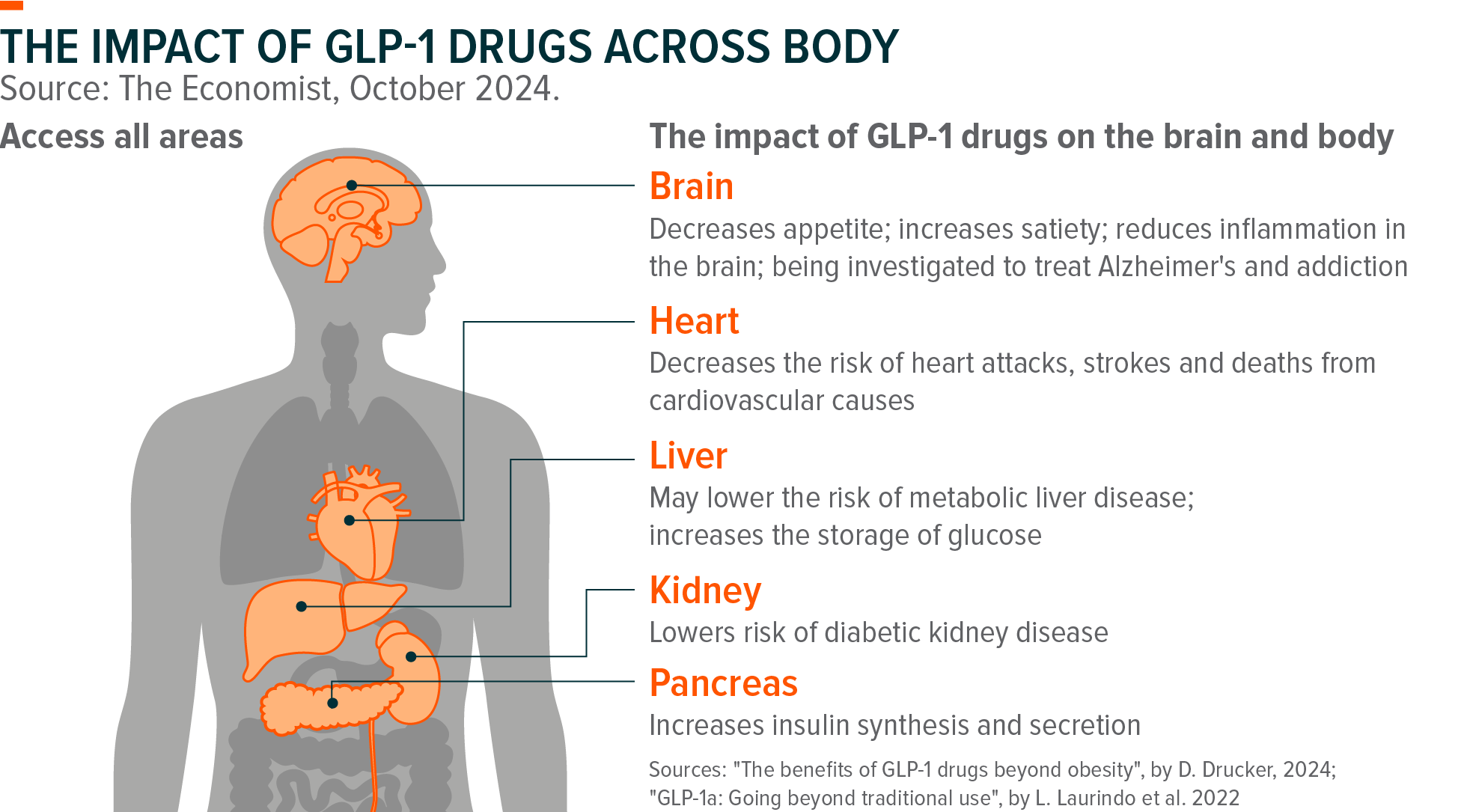

Recent findings indicate that obesity medications may not only address obesity itself but also prevent associated diseases. For instance, SELECT, Novo Nordisk’s landmark trial for its obesity medicine Wegovy, reported a 20% reduction in the risk of heart attacks, strokes, and cardiovascular-related deaths in non-diabetic patients with obesity and pre-existing cardiovascular conditions. GLP-1 are emerging as a ground-breaking class of drugs with potential benefits for various chronic conditions and a wide range of areas:

- Cardiovascular disease: In March, semaglutide (a GLP-1 receptor agonist sold as Ozempic for diabetes and Wegovy for weight-loss) was approved in America for treating cardiovascular disease in overweight individuals. A study of more than 17,600 overweight and obese patients from 41 countries demonstrated that those taking semaglutide experienced an average weight loss of approximately 10%, and a 20% reduction in serious adverse coronary events, strokes, heart attacks, and all-cause mortality. Importantly, these cardiovascular benefits were observed well before any significant weight loss occurred.

- Sleep apnea: In April tirzepatide (sold as Mounjaro and Zepbound) demonstrated positive results in late-stage trials for sleep apnoea, a breathing disorder.

- Chronic kidney and liver disease: Trials suggest that a potential for reducing chronic kidney disease, while it is currently under testing for liver disease.

- Substance use disorders (Addiction): recent study revealed that patients with a history of opioid or alcohol abuse, who were prescribed GLP-1 medications experienced lower rates of opioid overdoses and reported drinking less frequently. Additionally, research conducted on monkeys indicated that liraglutide can decrease alcohol consumption; however, trials involving human subjects have yielded inconclusive results.

- Alzheimer’s Disease: Early research suggests potential to improve learning, memory, and reduce amyloid buildup and brain shrinkage.

- Anti-aging: GLP-1’s ability to maintain cell health, reduce inflammation, and oxidative stress is leading to research into its potential as an anti-aging or longevity treatment.

Competition Landscape: Two-player Story to Remain

Novo and Lilly are poised to maintain their dominant duopoly in the obesity market, holding a combined market share of over 80% for the foreseeable future. This strong position is supported by their robust pipelines, enormous supply chain investments, and compelling clinical data. Additionally, their significant marketing expenditures to reach target patient populations, along with their first-mover advantage, further reinforce their market dominance, all backed by multi-year, multi-billion dollar capital expenditures

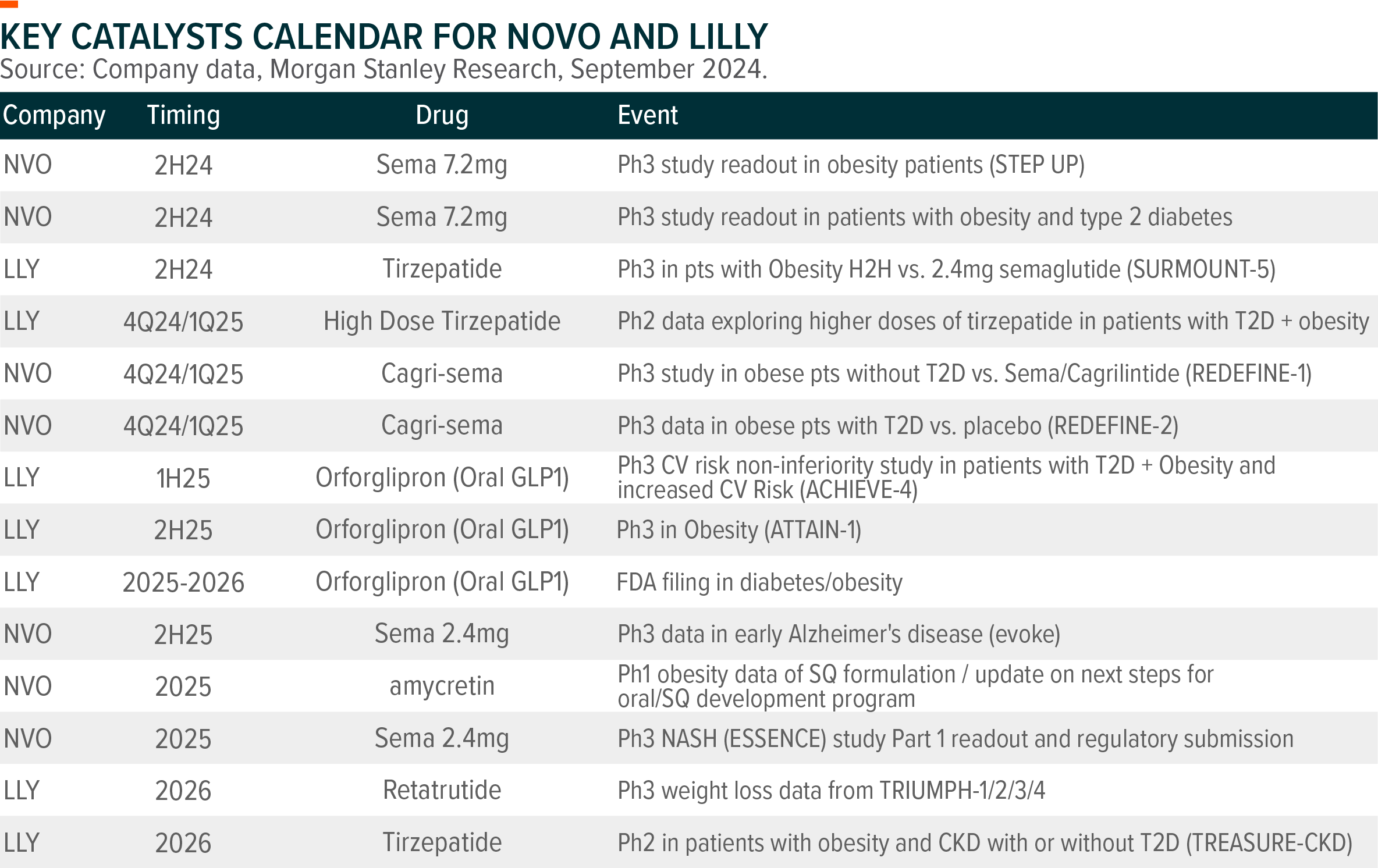

Novo and Lilly are expected to invest over $50 billion combined from 2022 to 2028 to bolster the supply chain supporting their GLP-1-based obesity franchises. While potential competition poses a challenge in the obesity market, the recent developments in their pipelines remain encouraging. In 2H24, there are several key diabesity pipeline readouts, including data from Novo’s Phase 3 REDEFINE 1 trial for its next-generation obesity asset, CagriSema, as well as results for high-dose Semaglutide.

Given the significant potential scale of the obesity market and the heightened interest from investors, there are compelling incentives for other companies to enter this lucrative market. Major players, including Roche, AstraZeneca, Pfizer, Novartis, Amgen, and Regeneron, have expressed interest in the obesity market and are developing related assets. For instance, Roche and AstraZeneca entered this space through acquisitions in 2023, while Amgen and Pfizer are advancing their diabesity pipeline drugs. However, it is crucial to note that these companies lag significantly behind Novo and Lilly in terms of innovation and infrastructure for obesity treatments. Novo and Lilly’s substantial head start, strong brand recognition, and positive clinic data may provide a protective buffer against competitive pressures. As a result, we expect the duopoly established by Novo and Lilly to continue thriving in the market.

5) BYD and 6) CATL: The Chinese Giants Will Emerge Stronger

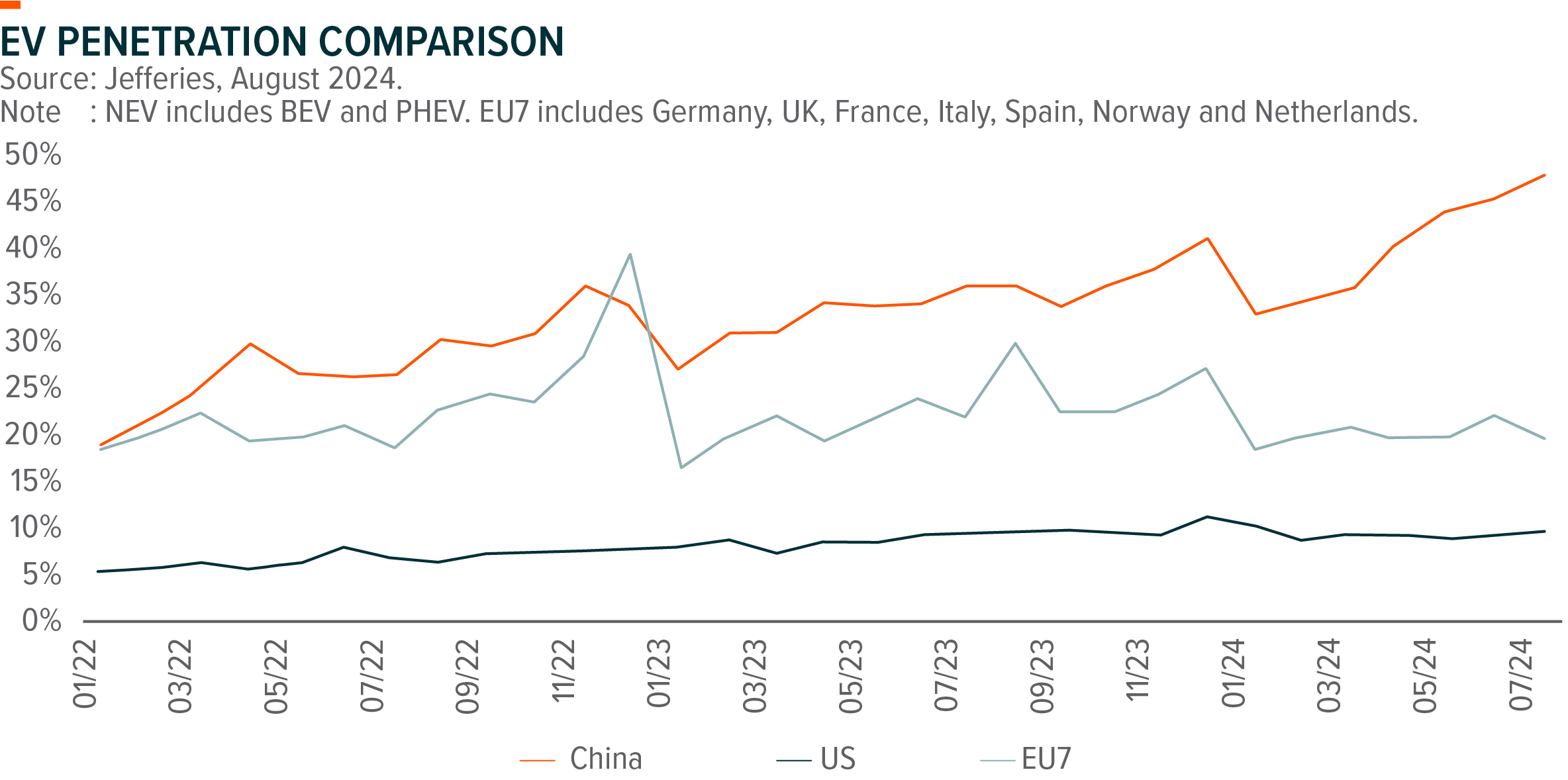

In the wave of global EV transition, China emerges as a global leader thanks to the ramp-up of charging infrastructure, rapid launches of competitive models, and rising awareness of consumers. China EV (including BEV and PHEV) penetration reaches 45%+ in past months, substantially higher than EU (c.20%) and US (c.10%), and China accounts for over half of EV sales globally. Across global EV value chain, Chinese enterprises are gaining traction, commanding the largest global share in EV (BYD) and battery (CATL) market. In a rapidly evolving industry, we see the solid cash position and strong R&D capability as the key for BYD and CATL to fend off competition and sustain leading positions.

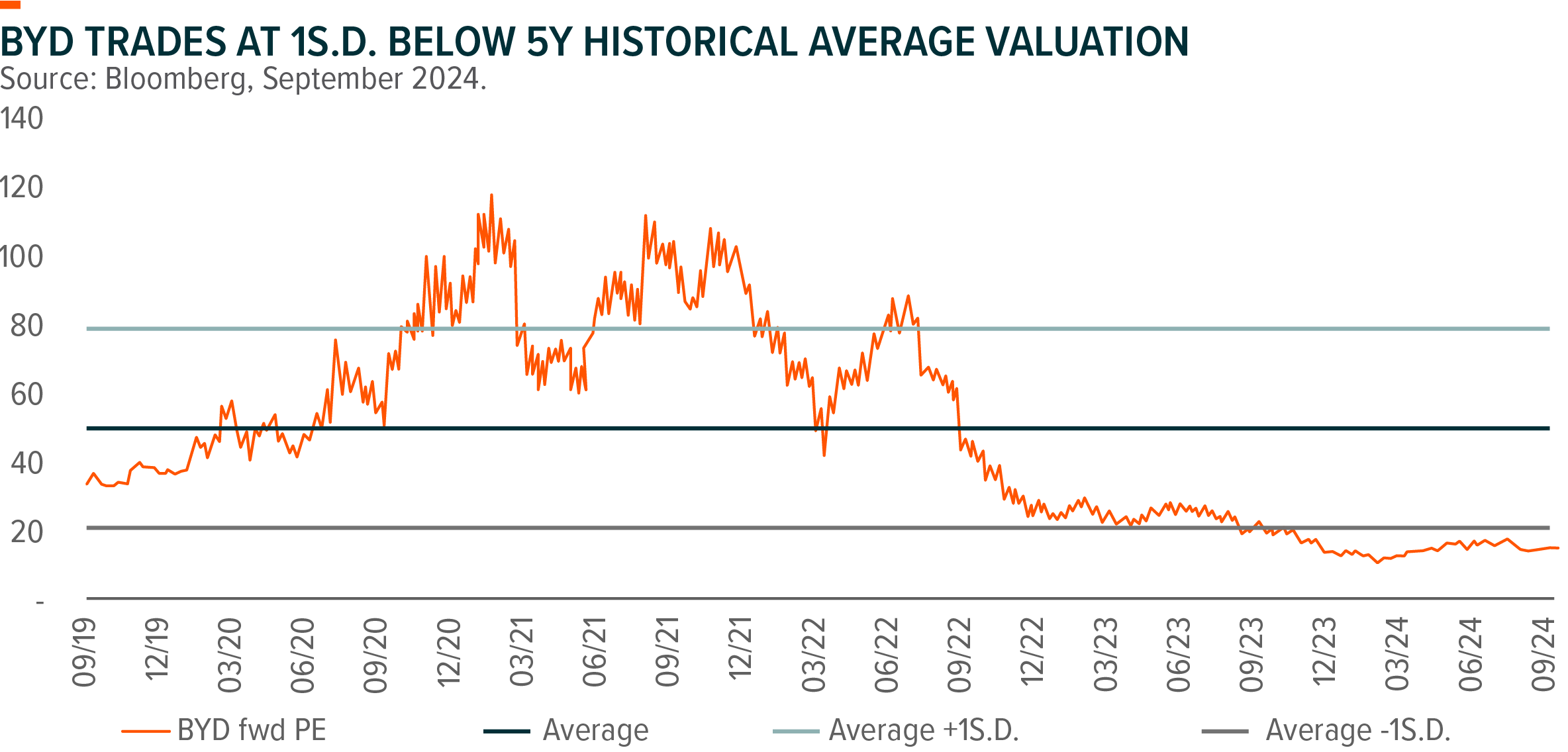

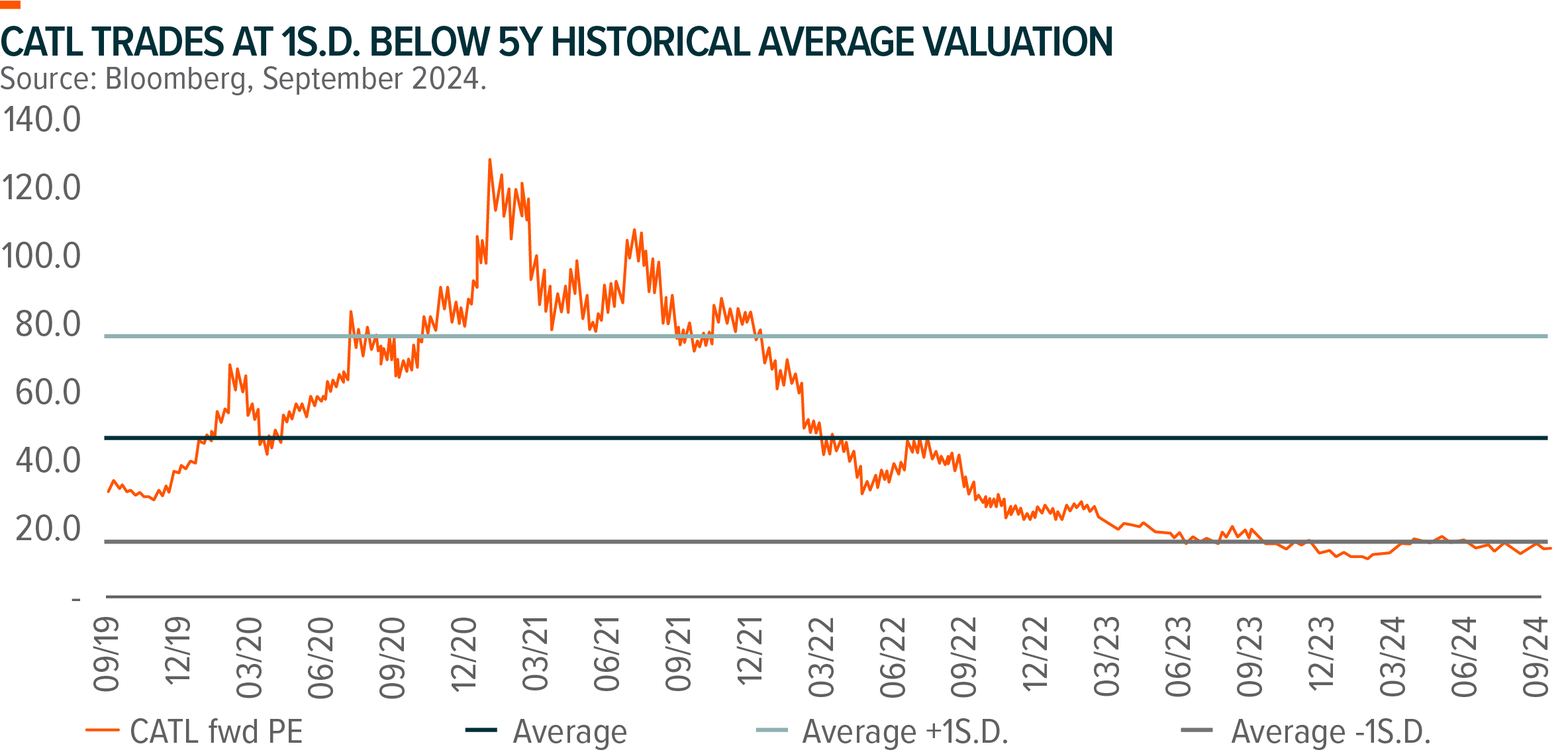

Albeit with strong product and cost competitiveness as well as solid growth outlook, BYD and CATL currently trade at undemanding valuations, offering a compelling opportunity for investors seeking to capitalize on the global EV development. BYD and CATL are key holdings for Global X Innovative Bluechip Top 10 ETF (3422 HK) with combined weighting of c.20%.

BYD – More Than a Cost Leader

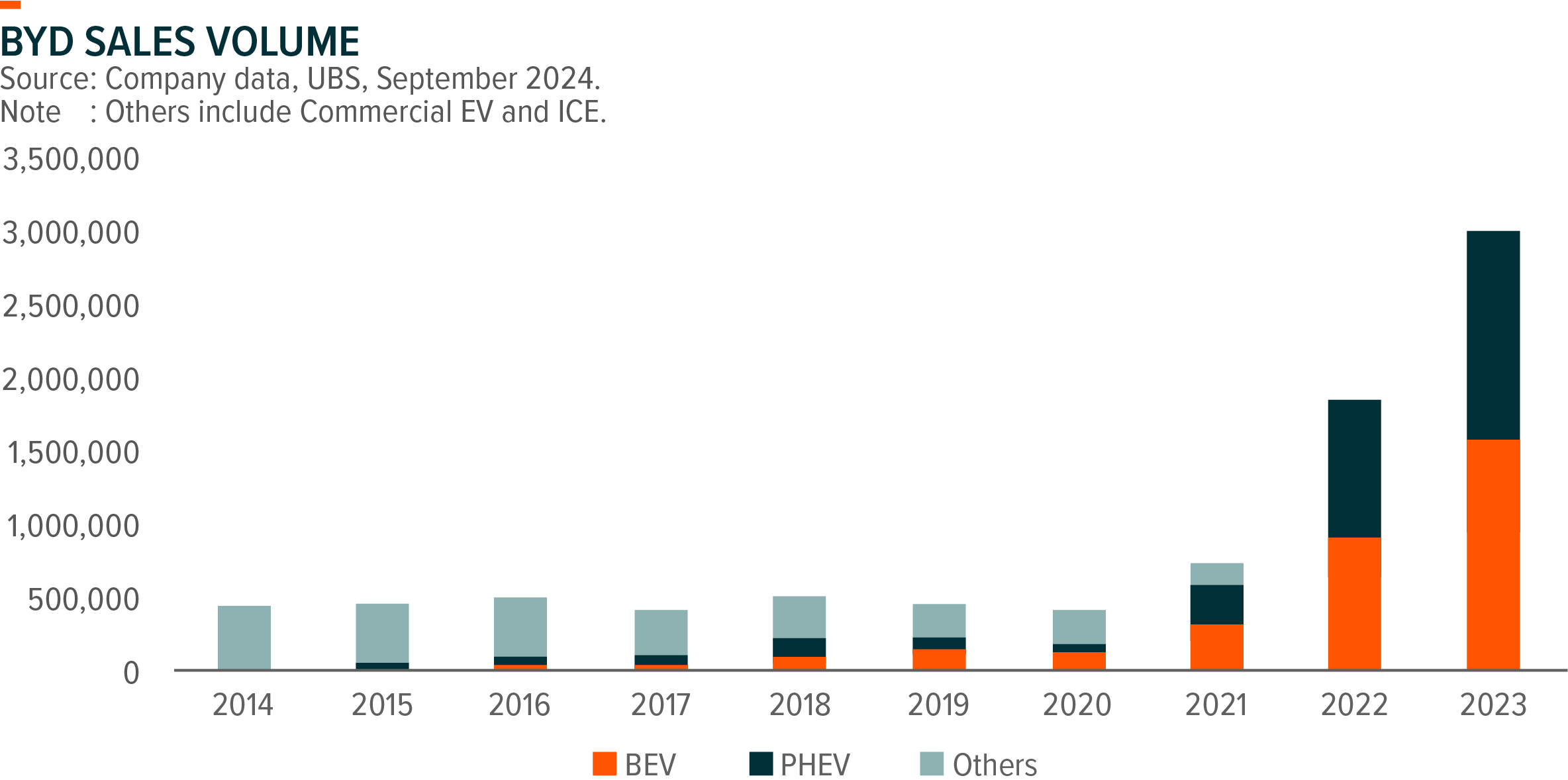

On the back of the surging NEV demand in China, BYD sold over 3mn units of NEVs (including 1.4mn units of PHEVs and 1.6mn units of BEVs) in 2023, and is on track to reach its 4mn units sales target in 2024, making it the largest NEV company (by volume) globally. Starting as a mass-market automaker, BYD’s superior cost basis and strong vertical integration helps the company capture the window of opportunities at the initial stage of EV transition, while its leading proprietary technology, improving brand recognition, and ongoing premiumization trajectory should support BYD to further capture global EV market share in a more profitable manner going forward.

Amid fierce competition, we see better sustainability for BYD with its healthy cash positions and strong R&D capabilities as compared to other loss-making peers, positioning the company as one of the best options to help investors capture the structural trend of vehicle electrification globally.

Technology leadership is the core to BYD’s dominance. Company expect R&D expenses in 2024 to continue ramp up vs 2023 (Rmb40bn) and R&D/Revenue will remain stable, as supported by the solid cash position (Rmb 68bn Net Cash in 2023) and strong FCF generated (Rmb 47bn FCF in 2023). BYD’s dedicated investments in R&D foster its leading technology (Proprietary cell-to-pack Blade batteries and DM-i technology) and rich product pipeline. Further roll out of DM-i 5.0 to more models and improving product mix should improve profitability outlook even in a highly competitive market.

Though still facing tariff uncertainty, overseas expansion should remain a key driver for BYD thanks to its established core battery technologies, model platform, and improving brand recognition. BYD’s strategy to invest in local production facilities should mitigate tariff uncertainty, and BYD will have 3 wholly-owned overseas factories with total annual capacity of 450k units by end-2025. BYD has entered into over 70 countries and regions, and we see potential for BYD to further penetrate into emerging markets such as Southeast Asia and South America as its price-competitive and quality products should cater to local consumer preference. Brazil, Thailand and Israel remain the top 3 export destinations for BYD YTD.

With persistent range anxiety among consumers and a shortage of rapid-charging stations, PHEV models are seeing booming demand and have become the key driver for NEV growth. BYD’s latest DM-i 5.0 technology brings greater fuel efficiency, longer range, and higher engine thermal efficiency, further enhancing the competitiveness of its PHEV models. Amid fierce competition, many mass-market JVs have been loss making in China since 2024, which could accelerate a strategic retreat by global carmakers from China market. This leaves BYD an opportunity to further gain market share driven by its product and price competitiveness, as well as rising brand equity.

CATL – Global Leader with Superior Battery Products

Overcapacity drove a deteriorating landscape in battery industry over the past 2 years, but we could be seeing an inflection point as supply-demand dynamics continue to improve. On supply side, Capex for Chinese battery makers decreased by over 50% from the peak, and planned annual Capex of key players for 2024/25E have also been revised down substantially. Continued Capex deceleration should drive a subsequent decrease in capacity. On demand side, China battery domestic shipment grew by c.40% YoY in 1H24, according to CABIA, as supported by resilient EV demand and growing ESS demand. Improving supply-demand dynamics should drive a gradual recovery in capacity utilization rate and support improving margin for key players.

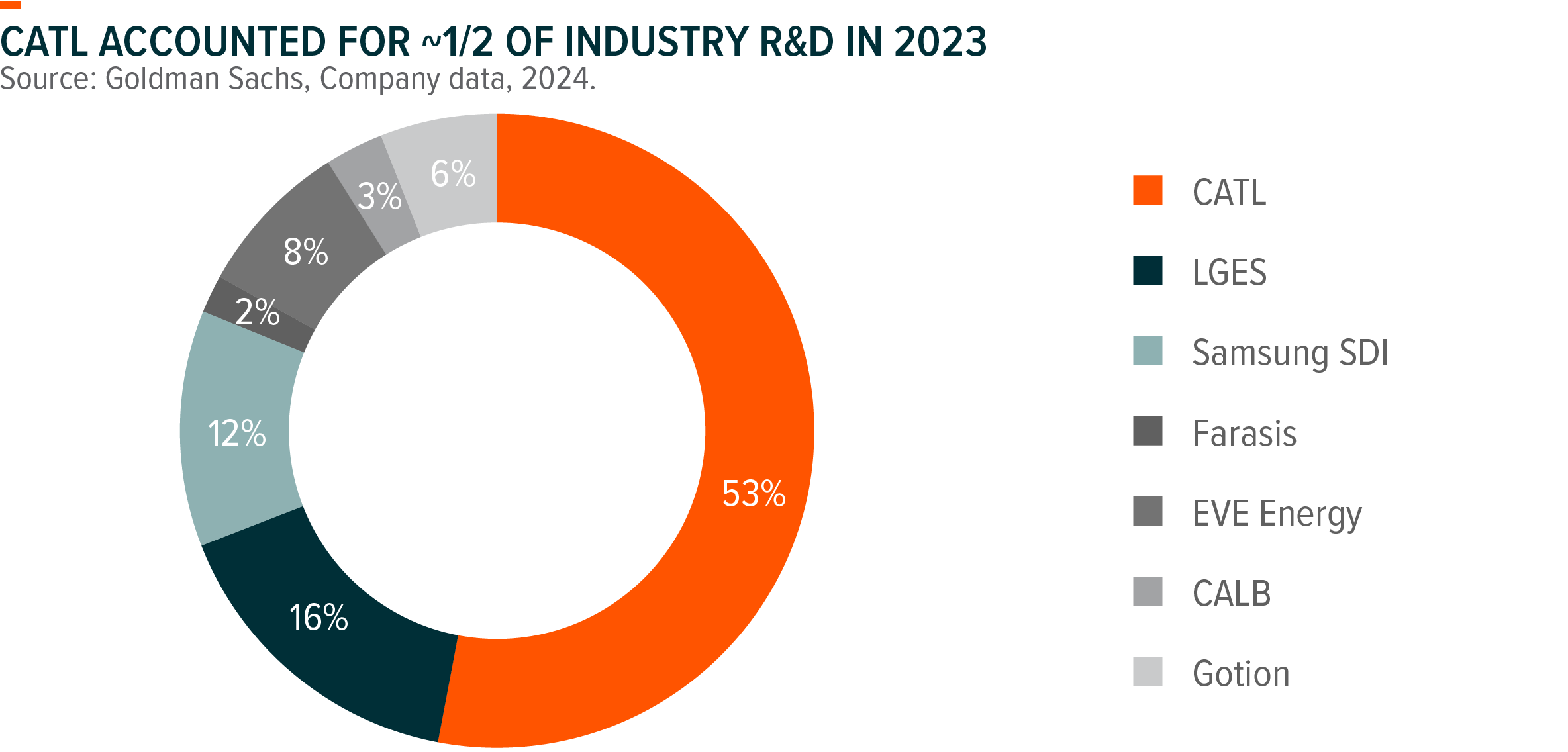

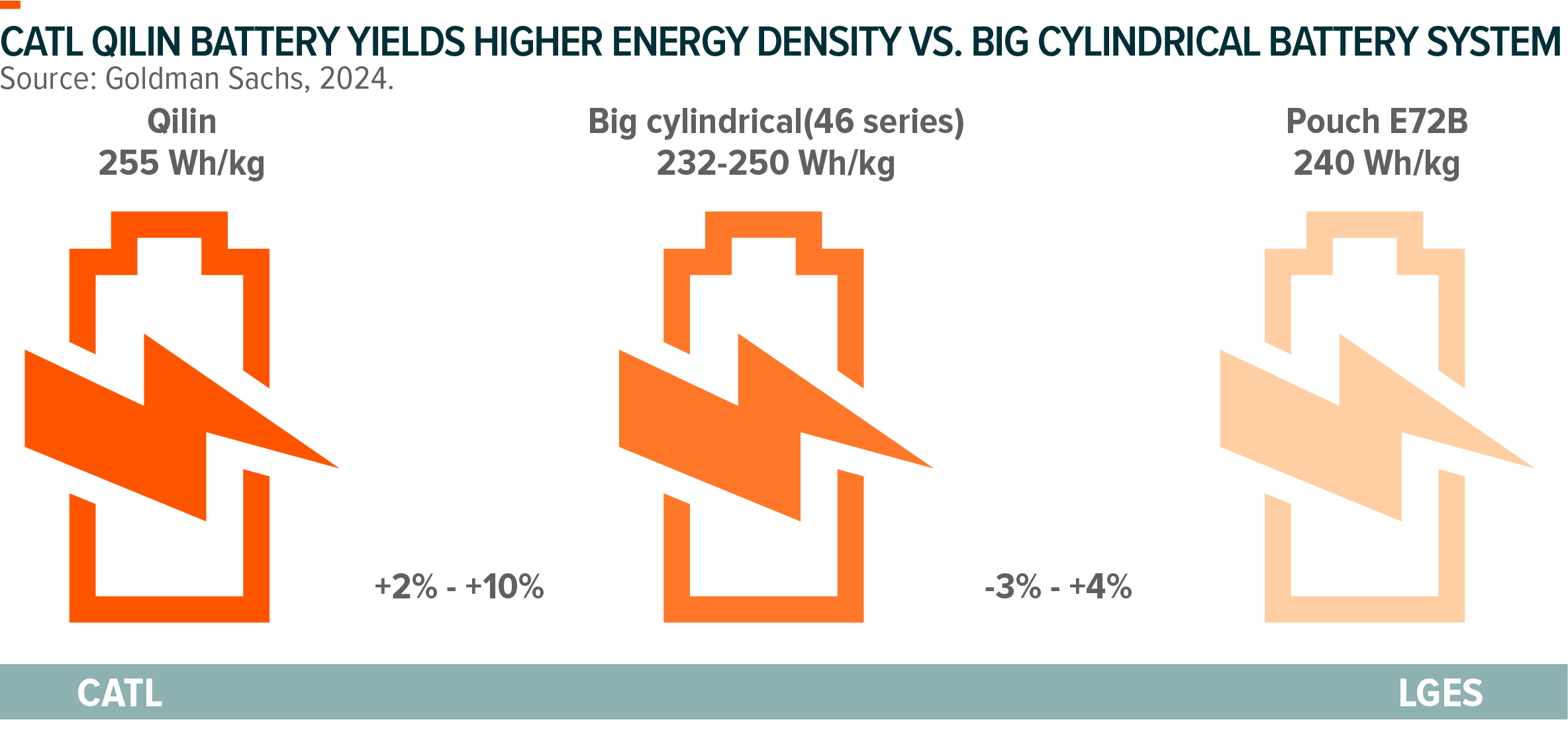

CATL is the largest battery maker globally, commanding c.40% global battery market share. CATL’s dominant position is bolstered by its superior battery products, featuring higher energy density and better quality, and the company enjoys a well-diversified client base covering leading EV OEMs globally. CATL’s battery yields higher energy density in both NCM space (Qilin Battery) and LFP space (Shenxing Plus Battery), thus enjoying price premiums compared to peer products. In addition, CATL battery offers better reliability, as evidenced by its lower warranty compensation ratio among peers. CATL’s solid cash positions and commitment in R&D should help sustain its competitive advantages in the long run.

CATL’s superior energy density brings both cost savings and price premiums for its battery, leading to better profitability compared to peers. CATL remains its dominant position in mid-high end market, and ongoing product premiumization trajectory through higher adoption in Energy Storage, Commercial Vehicles, Premium PV and Overseas should also contribute to profitability expansion. CATL expects its GP/unit to stay stable at around ~Rmb200/kWh, a substantial premium compared to peers.

Volume outlook remains solid at 20%+ YoY in 2024E as driven by solid ESS growth and resilient domestic EV demand. Overseas landscape is improving, with CATL’s Hungarian plant is on track for production in 2025, and its LRS cooperation in the US is also progressing steadily. CATL remains confident in the Europe market, stating that it will be the major supplier to European core OEMs’ new EV pipelines. ESS growth is expected to further accelerate in 2025E as US will step up tariffs on ESS batteries in 2026.

Related Global X ETFs’ Product1

| Global X Innovative Bluechip Top 10 ETF (3422 HKD) |

|

|---|---|

| Listing Date | 24 Nov 2023 |

| Reference Index | Mirae Asset Global Innovative Bluechip Top 10 Index2 |

| Primary Exchange | Hong Kong Stock Exchange |

| Ongoing Charges Over A Year | 0.68% p.a. |

| Product Page | Link |

The Fund adopts a single management fee structure, whereby a single flat fee will be paid out of the assets of the Fund to cover all of the costs, fees and expenses of the Fund. As the Fund is newly set up, this figure is an estimate only and represents the sum of the estimated ongoing charges over a 12-month period, expressed as a percentage of the estimated average Net Asset Value of the Listed Class of Units of the Fund over the same period. It may be different upon actual operation of the Fund and may vary from year to year. As the Fund adopts a single management fee structure, the estimated ongoing charges of the Fund will be equal to the amount of the single management fee, which is capped at 0.68% of the average Net Asset Value of the Listed Class of Units of the Fund. Any ongoing expenses exceeding 0.68% of the average Net Asset Value of the Listed Class of Units of the Fund will be borne by the Manager and will not be charged to the Fund. Please refer to the Key Facts Statement and the Prospectus for further details.