Important Information

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. There is no guarantee of the repayment of the principal. Investors should note:

- The investment objective of Global X K-pop and Culture ETF (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive K-pop and Culture Index (the “Index”).

- The Index is a new index. The Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history.

- The Fund is subject to concentration risk as a result of tracking the performance of a single geographical region or country (South Korea). The Fund may likely be more volatile than a broad-based fund, such as a global equity fund, as it is more susceptible to fluctuations in value of the Index resulting from adverse conditions in South Korea. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the South Korean market.

- The Fund’s investments are concentrated in companies in various industries and sectors including entertainment, communication services, internet, gaming, consumer staples, consumer discretionary as well as food. The business performance of these industries or sectors are subject to a wide range of risks. Fluctuations in the business for companies in these industries or sectors will have an adverse impact on the Net Asset Value of the Fund.

- The Fund may invest in small and/or mid-capitalisation companies. The stock of small-capitalisation and mid-capitalisation companies may have lower liquidity and their prices are more volatile to adverse economic developments than those of larger capitalisation companies in general.

- Underlying investments of the Fund may be denominated in currencies other than the base currency of the Fund. In addition, the base currency of the Fund is KRW but the trading currency of the Fund is in HKD. The Net Asset Value of the Fund and its performance may be affected unfavourably by fluctuations in the exchange rates between these currencies and the base currency and by changes in exchange rate controls.

- The borrower may fail to return the securities in a timely manner or at all. The Fund may as a result suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests. As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund.

- The trading price of the Shares on the SEHK is driven by market factors such as the demand and supply of the Shares. Therefore, the Shares may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Share of the Fund and will reduce the capital available for future investment.

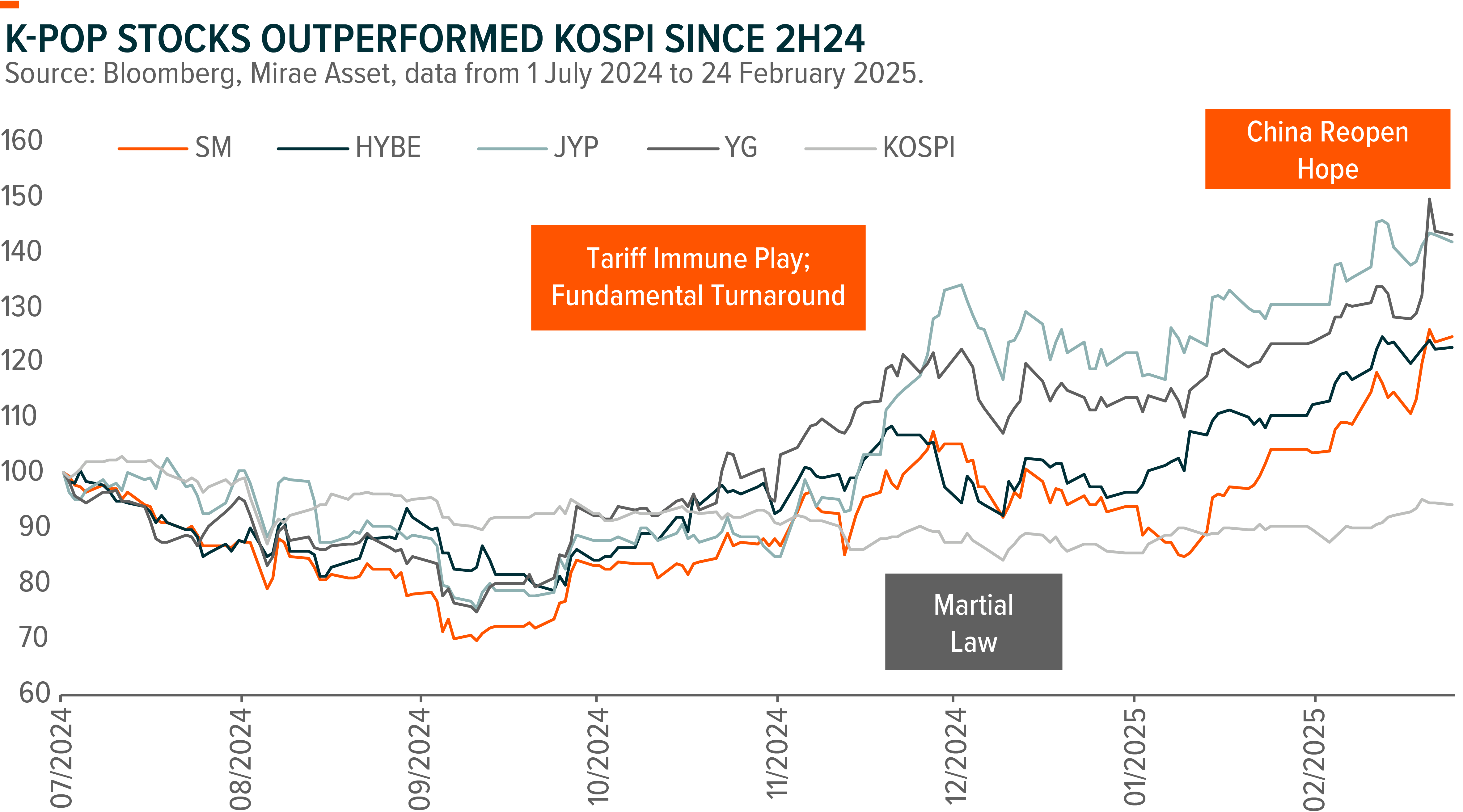

Growing Hope on China Market Reopen

A Potential Boon for the K-Pop

Starting around 2016-2017, China had “Hallyu” ban on K-pop due to political tensions over THAAD, affecting K-pop concerts, TV shows, and other cultural exports. However, after 8 years, the situation is likely to end as Korea Economic Daily reported on 20 Feb that China may lift its ban on K-pop culture as early as May. K-pop stocks rallied on the growing hope of the reopen of China market.

Following our previous articles on the K-pop industry (Capturing the Rally of K-pop; Korea Entertainment – Ready for Revival), we will further analyze the potential impact of China market reopening. In the short term, China’s reopening will directly boost profit through offline concerts, while the long-term upside is substantial driven by further penetration into this large population market. Our Global X K-pop and Culture ETF (3158) has significant exposure to K-pop content sector, with 4 leading entertainment companies accounting for 37% of its holdings.

China Used to Be a Focused Market Before the ‘Hallyu’ Ban

Prior to the ban, China is a crucial target market for K-pop companies. Among leading entertainment companies, SM was more heavily reliant on China market, with groups like EXO (featuring 4 Chinese members out of total 12 members) and sub-units such as Super Junior-M and EXO-M specifically targeting Chinese audiences. SM also collaborated with China tech giants – Tencent and Alibaba – for distribution. Similarly, JYP had groups like Miss A (2 Chinese out of 4) and Got7 (Jackson Wang) with Chinese members. YG’s BigBang and 2NE1 also enjoyed strong fan base in China with BigBang joined major Chinese TV shows and charted top on QQ Music. HYBE (formerly Big Hit) has relatively less exposure pre-ban since BTS blew up more globally post-2017. Another example is cosmetics companies Amorepacific, whose brands, such as Laneige and Innisfree, once enjoyed substantial success in China with China market accounting for 19%/24% of revenue in 2016/2017 (vs 10% in 2024E).

Post-ban, K-pop companies shifted focus to other markets like Southeast Asia, US, and Japan. This period witnessed an unprecedented expansion of K-pop’s global influence. If China reopens, we believe the direct impact will be focused on offline concerts as even during the ban, companies remained actively engaged online by promoting artists to acquire fans and monetizing through eCommerce such as album sales, contents, merchandise and membership.

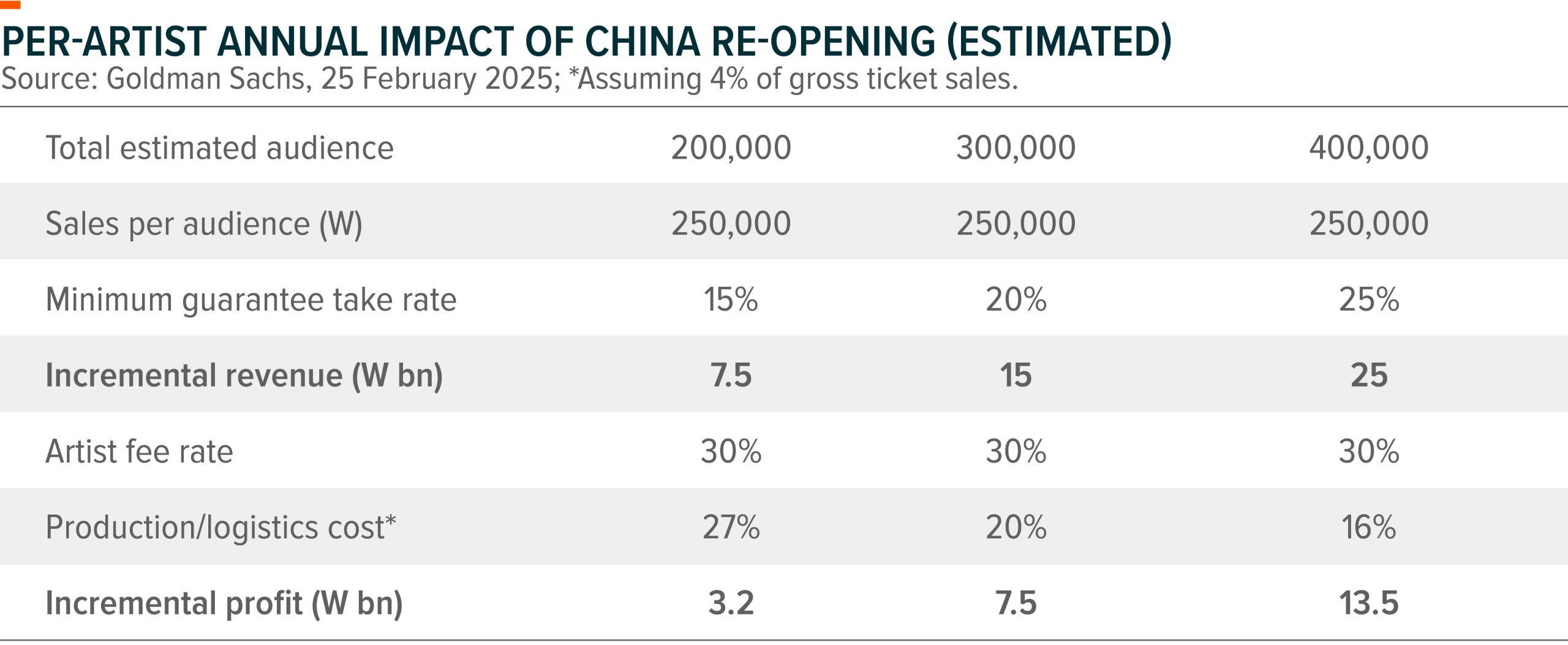

Quantifying the Impact of China Reopen

To gauge the potential impact, we can analyze Bigbang’s large scale tour during 2015-2016, with c.200k/450k attendees in 2015/2016 in mainland China. Projecting a similar scale for top-tier artists upon the China market’s reopening, with an estimated audience ranging 200-400k per artist annually, we can estimate incremental revenue and operating profit.

Considering a mid-range scenario (300k audience per artist), and identifying number of top artists across the four major agencies – HYBE (4 – BTS, Seventeen, Enhypen, TXT), JYP (2 – Twice, StrayKids), SM (2 – Aespa, NCT), YG (1 – Blackpink) – China concerts alone could generate HSD to teens growth in OP level.

Further Upside over Long-Term

The impact extends beyond immediate offiline concert revenue. Increased media exposure will foster fanbase growth, driving sales of merchandise, digital content, and memberships. Furthermore, the cultural phenomenon of K-pop could generate significant synergies with other Korean industries, such as K-beauty and K-food. The reopening of China market is not simply a return to past successes but potentially a springboard for even greater expansion within China and beyond.

| Global X K-pop and Culture ETF (3158) |

|

|---|---|

| Listing Date | 19 Mar 2024 |

| Reference Index | Solactive K-pop and Culture Index |

| Primary Exchange | Hong Kong Stock Exchange |

| Total Expense Ratio | 0.68% p.a. |

| Product Page | Link |

Source: Mirae Asset; Data as of February 2025.