Important Information

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. There is no guarantee of the repayment of the principal. Investors should note:

- Global X Asia Semiconductor ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Semiconductor industry may be affected by particular economic or market events, such as domestic and international competition pressures, rapid obsolescence of products, the economic performance of the customers of semiconductor companies and capital equipment expenditures. These companies rely on significant spending on research and development that may cause the value of securities of all companies within this sector of the market to deteriorate.

- Some Asian securities exchanges (including Mainland China) may have the right to suspend or limit trading in any security traded on the relevant exchange. The government or the regulators may also implement policies that may affect the financial markets. Some Asian markets may have higher entry barrier for investments as identification number or certificate may have to be obtained for securities trading. All these may have a negative impact on the Fund.

- The Fund invests in emerging markets which may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risks, currency risks/control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk, currency devaluation, inflation and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

Global X Asia Semiconductor ETF (3119) Review: Bottoming out of the Semiconductor Cycle

Listen

Global X Asia Semiconductor ETF delivered solid performance YTD

The Global X Asia Semiconductor ETF provide diversified exposure to the entire semiconductor supply chain here in Asia. Asian companies are global leaders in a number of subsegments in the industry such as foundry, memory and semiconductor equipment. The fund’s positive return year-to-date1 can be attributed to two main factors: One, bottoming out of the cycle in most semiconductor categories including logic and memory. Two, the accelerated commercialization of AI consequently brought incremental demand for AI-related semiconductors.

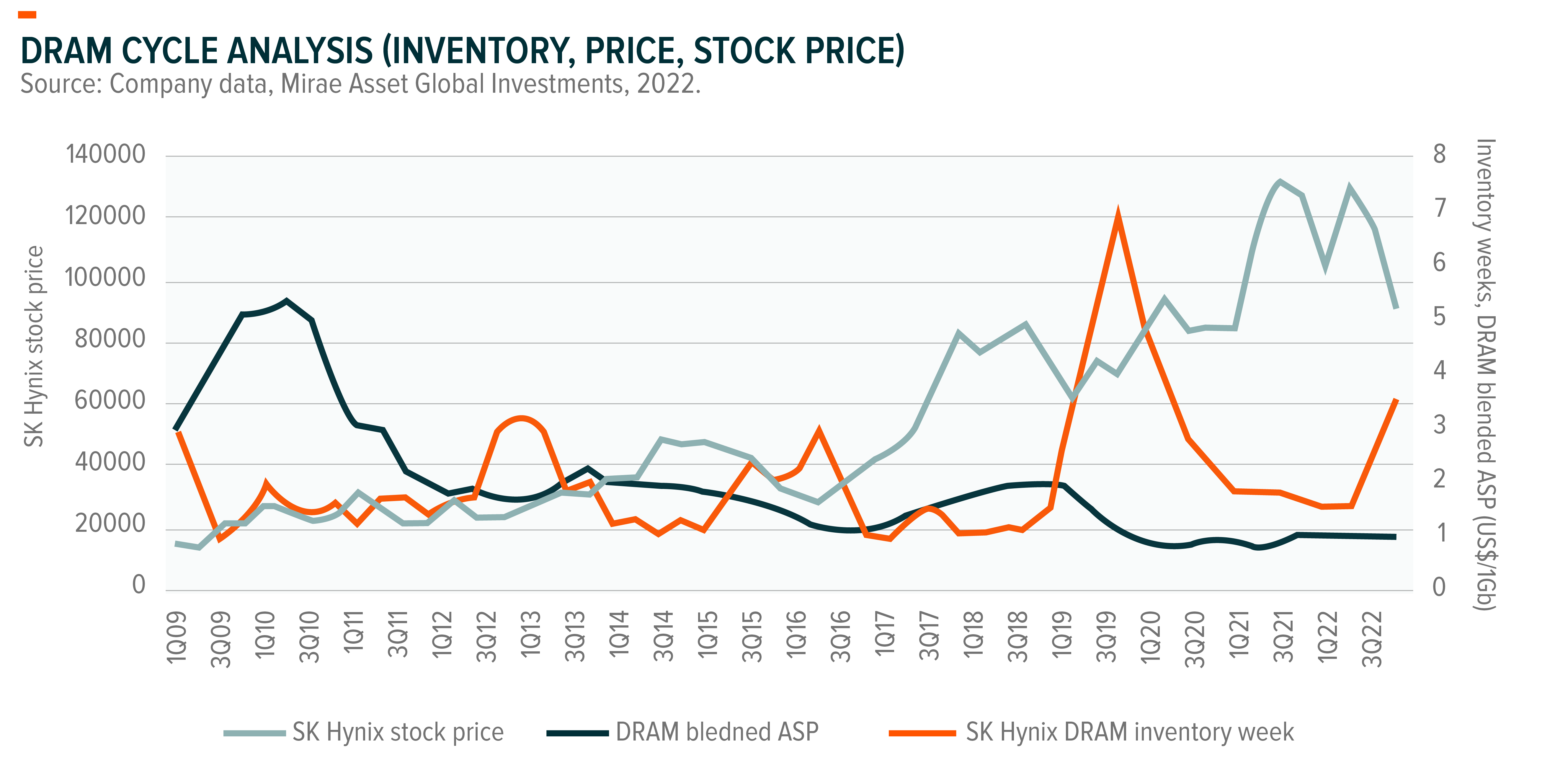

Memory cycle bottom out

Analyzing the past 4 cycles, memory stock prices usually bottom before/at inventory peaks while DRAM prices bottom after inventory peaks. The strength in memory share prices is driven by 1) better visibility of cycle bottom as memory makers expect their inventory to peak in 2Q23. DRAM prices already hit cash cost 1H23 investors see limited downside from the current level.1 2) Production cut from all three major DRAM suppliers. Micron announced over 20% production cut at the end of last year, followed by SK Hynix and Samsung this year.2 Lower bit supply growth from producers will help speed up the normalisation of inventory levels. 3) The increasing penetration in DDR5 (Double Data Rate) and AI server adoption of HBM (High Bandwidth Memory) improve memory demand and blended pricing.1