Electric Vehicles: Driving the Future of Power Semiconductors

Power semiconductors are becoming increasingly important, as the rise of electric vehicle (EV) and automation is expected to create strong demand for power semiconductors. In this field, Chinese companies are relatively small but gaining market share, supported by local EV and electronics companies. This article explains the basics of power semiconductors and how Chinese semi companies are positioned to capture the new opportunity.

Power semiconductors, a key component in all electronic devices, are mainly used to change the physical characteristics of the circuit such as voltage and to manipulate the circuit. The rapid development of EV, industrial automation, clean energy and smart grid results in increasing demand for more power semiconductors with better performance. IHS estimated the global power semiconductors to be a US$40bn industry in 2019, around 10% of the overall semiconductor industry. (IHS 2020)

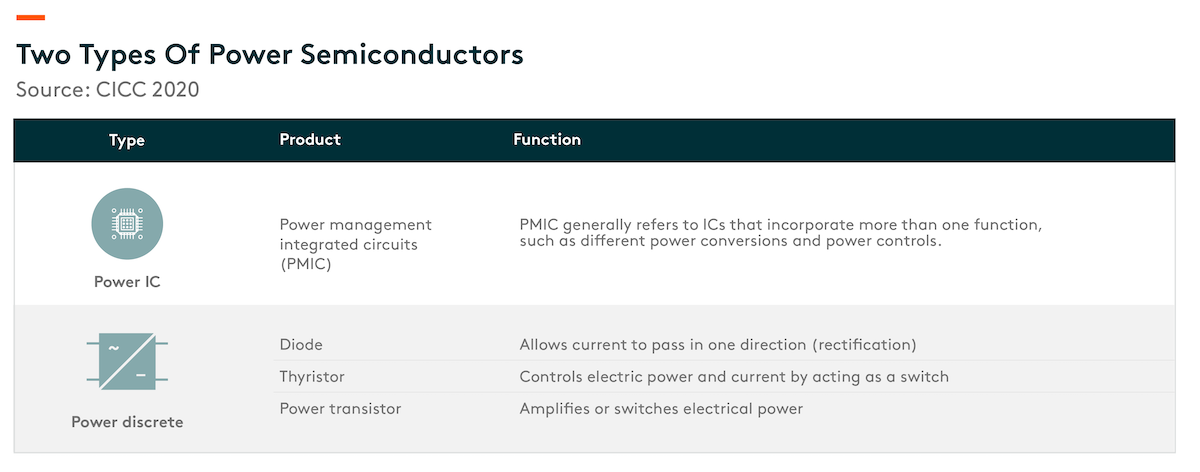

There are two types of power semiconductors, namely power discrete and power integrated circuit (IC), and each accounts for around half of the total market. Under power discrete, the three main products are diode, thyristor and power transistor. Power transistor is the largest segment, accounting for around 75% of the power discrete market. (CICC 2020) The three main designs for power transistors are insulated-gate bipolar transistor (IGBT), metal–oxide–semiconductor field-effect transistor (MOSFET) and bipolar junction transistor (BJT). MOSFET and IGBT are widely adopted in all kinds of electronic devices, with IGBT typically used for higher voltage applications such as industrial and auto.

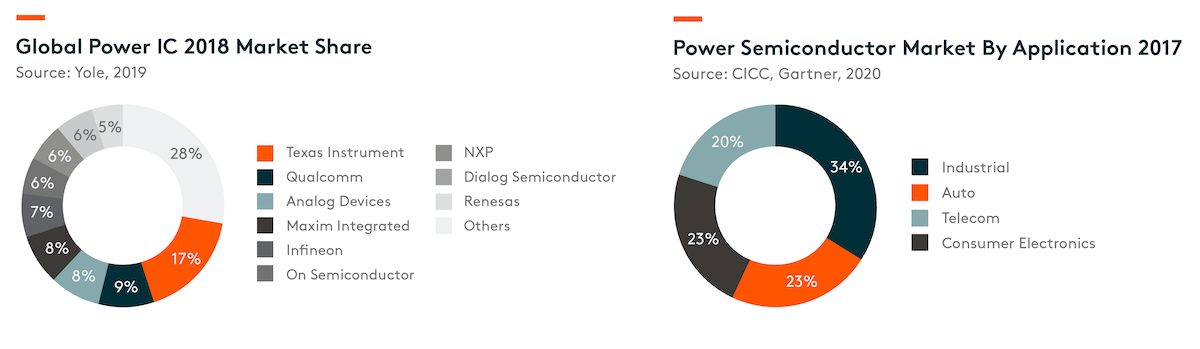

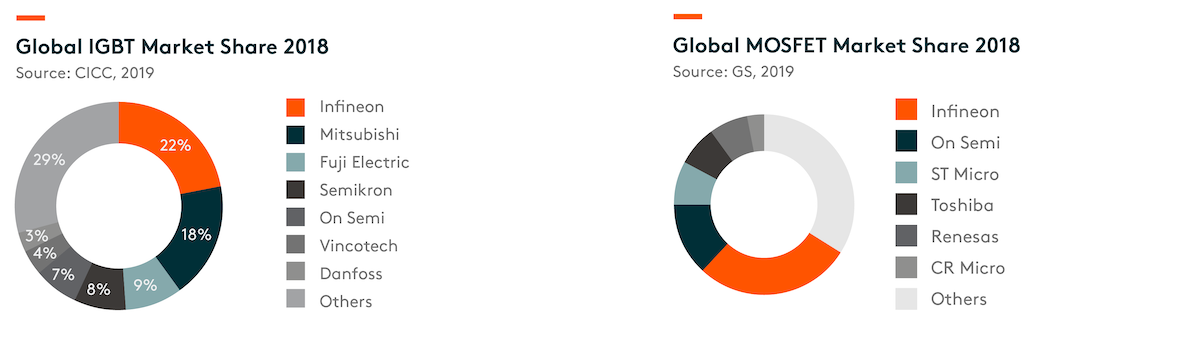

The power integrated circuit (IC) market was US$18.5bn in 2019 (Yole 2019), with the majority being power management IC. Yole expects the power IC market to reach US$22.7bn by 2023. The majority of the global leaders in power semiconductors are integrated device manufacturer (IDM), as technology migration in power semiconductors is relatively slower and less capital intensive. Texas instruments had the largest market share in power IC at 17% in 2018 (Yole 2019), followed by Qualcomm and Analog Devices. Infineon, which was spun off from Siemens in 1999, dominated the power discrete market with the largest market share in both IGBT and MOSFET.

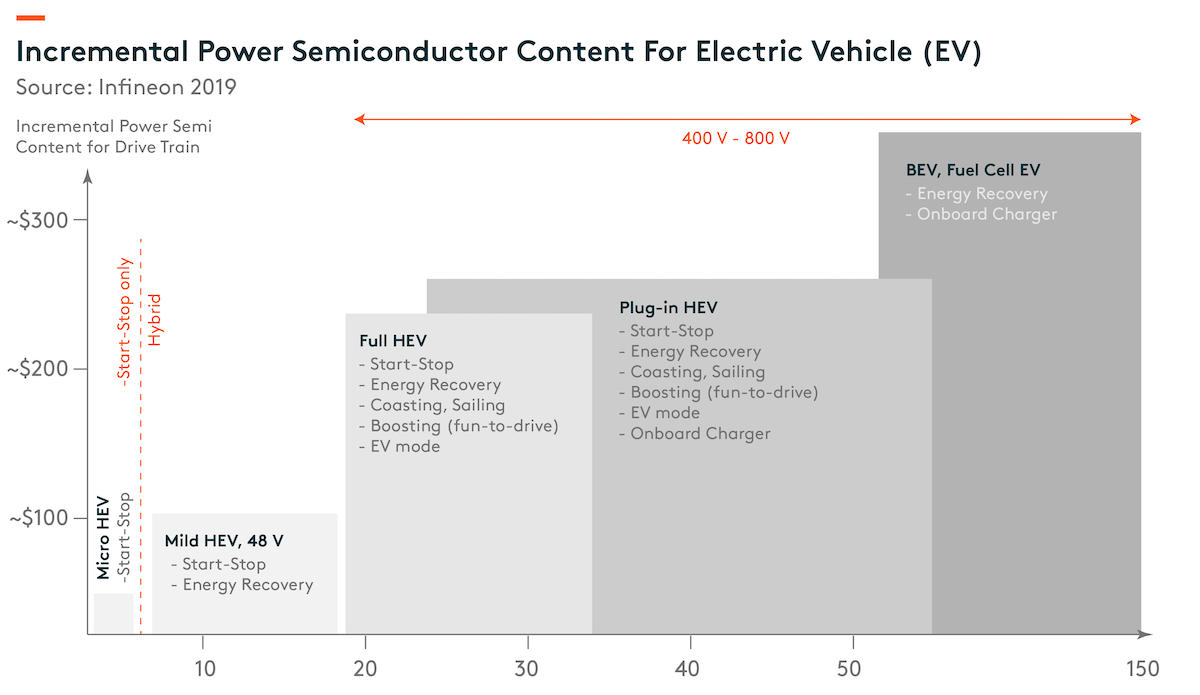

EV and automation drive demand for power semiconductors

Infineon (2020) estimates semiconductor bill of materials (BOM) of a full EV today to be US$834, compared to around US$350 in an average internal combustion engine car. Power semiconductors are one of the key upgrades in semiconductor under the switch from internal combustion engines to electric motors. For example, Tesla’s three-phase AC asynchronous motor uses 28 IGBTs per phase (total 84 IGBTs), plus another 12 IGBTs for other components. Tesla uses a total of 96 IGBT, with a value of around US$400. (Guoxin 2021) We expect demand for power semiconductors to grow as EV continues to penetrate the overall auto market.

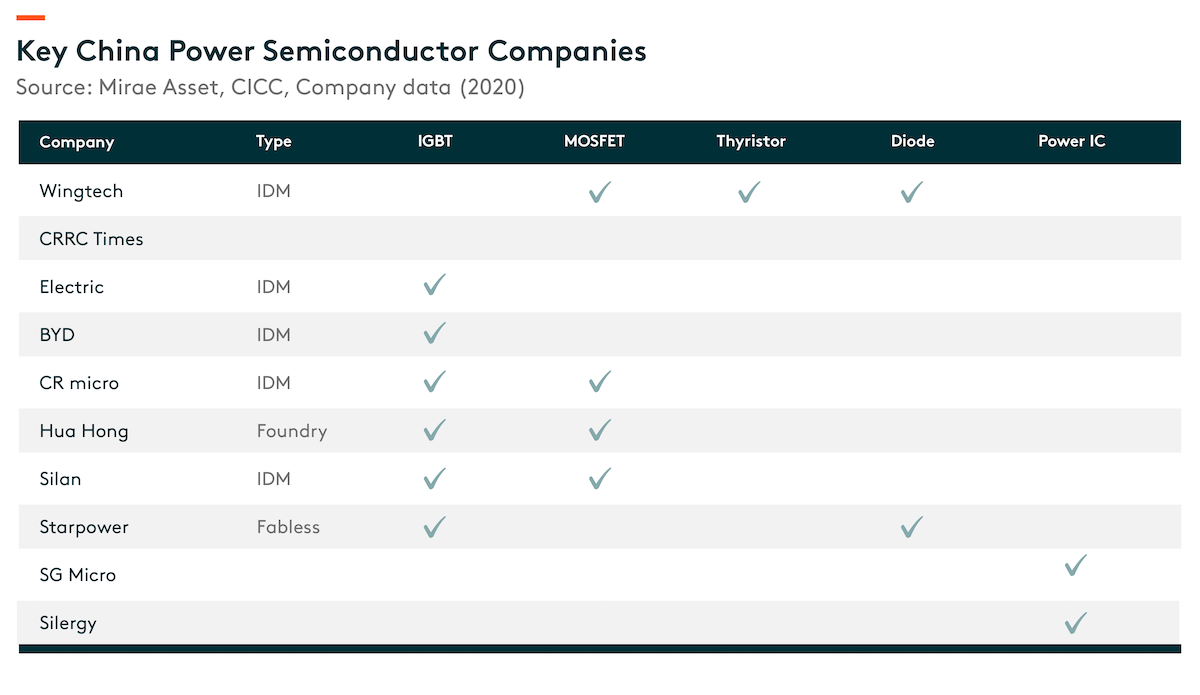

Chinese companies gain market share

The development of the local EV industry will drive local power semiconductor supply chain, similar to how domestic smartphone brands support China’s semiconductor industry. Although domestic power semiconductor players are relatively small compared to global leaders, China has formed a local supply chain in power semiconductor with a combination of fabless, foundry and IDM. In power management IC, Silergy and SG micro are domestic leaders. For diode under power discrete, Wingtech acquired Nexperia which has the largest market share in small signal diodes and transistor globally. In MOSFET, Wingtech also has a strong presence in low-voltage auto products. Hua Hong works with domestic fabless like CR micro to supply MOSFET. In IGBT, Starpower has around 2% (CICC 2020)market share globally, and is gaining market share in industrial and auto applications. CRRC Times operates an IDM model supplying high voltage IGBT for railway and industrial applications.