Important Information

Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- The investment objective of Global X China Biotech ETF’s (the “Fund”) is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive China Biotech Index.

- The Fund is exposed to concentration risk by tracking a single region or country.

- The Index constituents may be concentrated in a specific industry or sector, which may potentially more volatile than a fund with a diversified portfolio.

- Biotech companies invest heavily in research and development which may not necessarily lead to commercially successful products, and the ability for biotech companies to obtain regulatory approval (for example, product approval) may be long and costly.

- Investment in Emerging Market, such as A-share market, may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The Stock Connect is subject to quota limitations. Where a suspension in the trading through the Stock Connect is effected, the Sub-Fund’s ability to invest in A-Shares or access Mainland China markets through the programme will be adversely affected.

- Listed companies on the ChiNext market and/or STAR Board are usually subject to higher fluctuation in stock prices and liquidity risks, over-valuation risk, differences in regulation, delisting risk, and concentration risk.

- There are risks and uncertainties associated with the current Mainland China tax laws, regulations and practice in respect of capital gains realized via Stock Connect on the Fund’s investments in Mainland China. Any increased tax liabilities on the Fund may adversely affect the Fund’s value.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy may invest up to 50% of its net asset value in financial derivative instruments (“FDIs”), which may expose the Fund to counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. The Fund may suffer losses from its usage of FDIs.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

- The Fund may suffer from a losses or delays when recovering the securities lent out. This may potentially affect its ability to meet payment and redemption obligations. Collateral shortfalls due to inaccurate pricing or change of value of securities lent, may cause significant losses to the Fund.

China Biotech Update

From Fast Follower to Global Leader

2025 Review

For the China biotech industry, 2025 was a transformative year, marked by its emergence as a fast leader rather than merely a fast follower. This leap occurred despite a challenging domestic VC funding landscape and U.S. regulatory pressure.

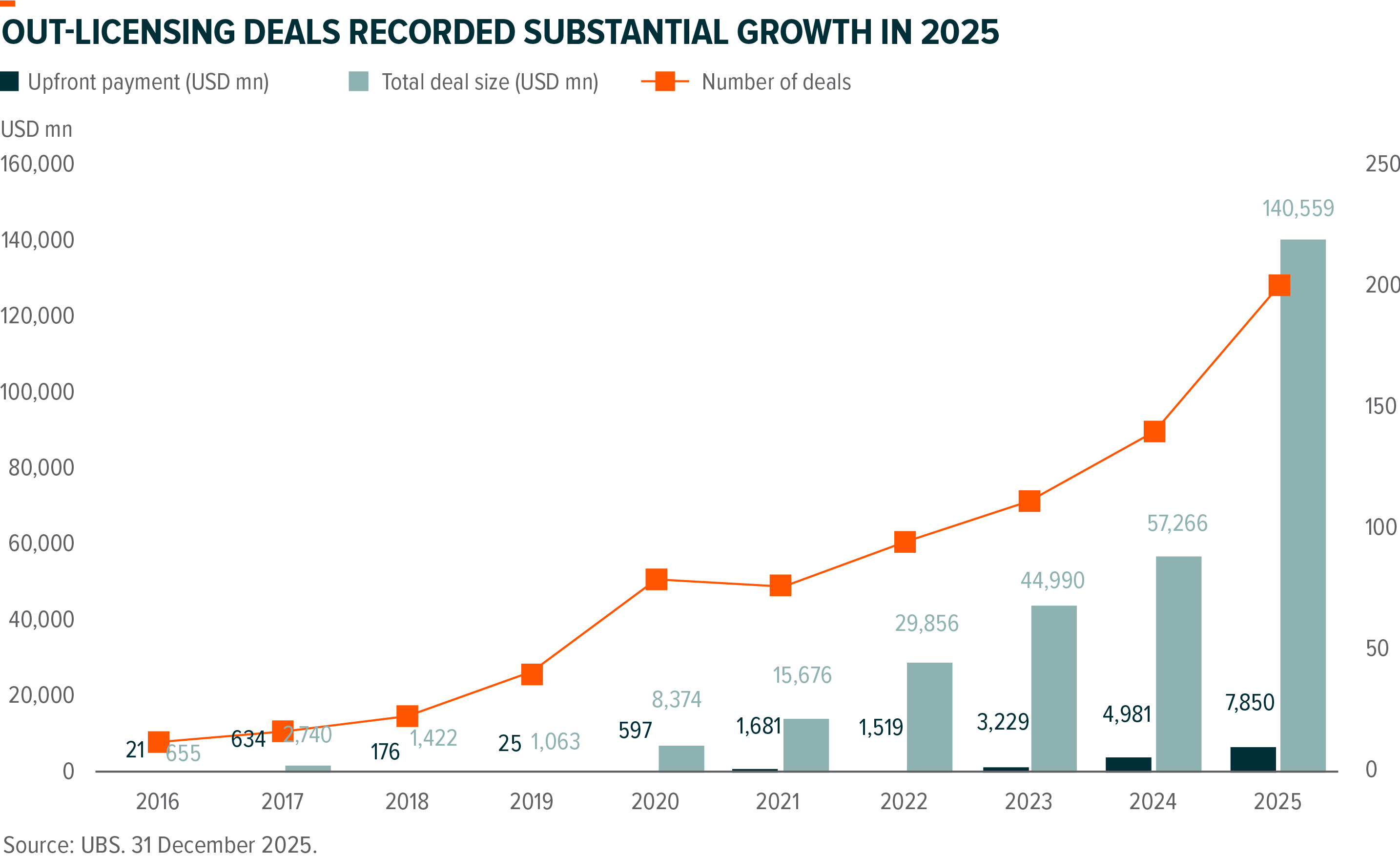

The Out-licensing Explosion

The most defining characteristic of 2025 was the boom in out-licensing of novel drugs. Total deal value reached a record $135.7 billion, more than doubling the $51.9 billion recorded in 2024. Global giants, including GSK, Merck, and AstraZeneca, became increasingly dependent on the Chinese pipeline, particularly in the ADC (Antibody-Drug Conjugate) and bispecific antibody sectors. The biotech VC funding was still far behind the 2021 peak.

The ‘DeepSeek’ Moment in Biotech

The ‘DeepSeek’ Moment in Biotech was buzzword in 2025. Akeso’s Ivonescimab defeated the world’s best-selling drug, Keytruda, the current best-selling drug in the world, in a head-to-head lung cancer trial. This DeepSeek moment for biotech proved that Chinese innovation wasn’t just cheaper—it was better. This caused a fundamental shift in how Western capital perceives Chinese R&D.

The US BIOSECURE Act

The U.S. BIOSECURE Act was enacted into law on December 18, 2025, as part of the FY26 National Defense Authorization Act. The final version was less prescriptive than initial drafts, as it removed specific company names like Wuxi Apptec and Wuxi Bio from the statute itself, instead creating a process for the Office of Management and Budget (OMB) to publish a list of biotechnology companies of concern by December 2026. The Act includes a grandfather clause allowing existing contracts with any future listed companies to continue for up to five years after the prohibitions take effect.

The Wuxi group accelerated its Global Dual Sourcing strategy in response to these geopolitical concerns. WuXi Biologics’ Ireland plant turned a profit ahead of schedule, with high demand for its manufacturing services, demonstrating operational resilience through globally diversified infrastructure.

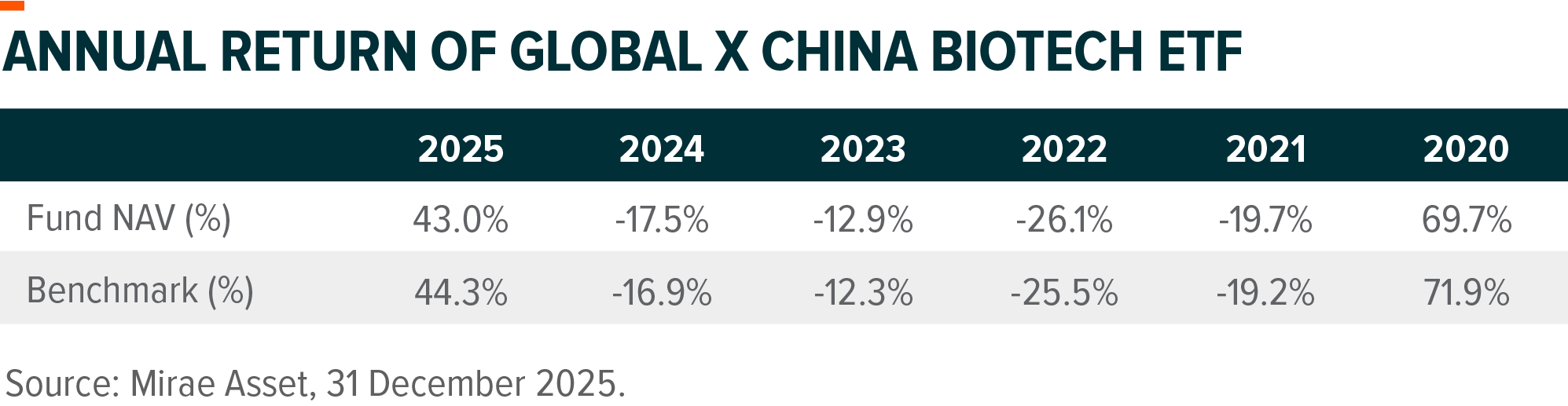

Past performance information is not indicative of future performance. Investors may not get back the full amount invested. The computation basis of the performance is based on the calendar year end, Net Asset Value to Net Asset Value. These figures show by how much the Fund increased or decreased in value during the calendar year shown. Performance data has been calculated in RMB including ongoing charges and excluding trading costs on SEHK you might have to pay. The Index of the Fund is Solactive China Biotech Index. Fund inception date: 24 July 2019.

Company Review & Outlook

Below is a review of key ETF holdings for 2025 and an outlook for 2026.

BeOne Medicines

Financial Milestone: In 2025, BeOne became the first Chinese-founded biotech to achieve sustainable profitability, reporting positive net income and strong free cash flow ($350m in Q3 alone).

Brukinsa: Its flagship BTK inhibitor, Brukinsa, officially reached blockbuster status with annual sales exceeding $3.5 billion (trending toward a $5bn+ annual run rate). It now leads the U.S. market in new-patient starts for Chronic Lymphocytic Leukemia (CLL), capturing significant share in a global BTK market valued at approximately $12 billion.

Production Localization: A primary focus for 2026 is the operational scale-up of its $800 million manufacturing and R&D flagship facility in Hopewell, New Jersey, which opened in July 2024. U.S.-based production will mitigate geopolitical risks associated with the BIOSECURE Act.

Pipeline Catalysts: Key milestones for 2026 include massive Phase 3 readouts for its PD-1 inhibitor, Tislelizumab (Tevimbra), in various combination therapies, as well as the potential commercial launch of Sonrotoclax (BCL2 inhibitor) following FDA Priority Review

Hengrui Pharma

Revenue Transformation: 2025 marked a historic pivot as innovative drugs accounted for over 60% of total revenue for the first time. (Company data, Mirae Asset, January 2026)

Strategic Out-Licensing: Hengrui secured a mega-deal milestone, capturing over $13 billion in potential payments through licensing agreements with GSK and Merck (MSD).

U.S. Market Entry: Hengrui is shifting from a Licensing-Out model to Direct Commercialization. Through its U.S. affiliate, Luzsana Biotechnology, it will attempt to market its own portfolio in the States—a bold, high-risk, high-reward strategy.

GLP-1 Catalyst: In the domestic market, the launch of its oral GLP-1 is expected to be a major revenue driver. Hengrui aims to capture the metabolic market by undercutting Western competitors’ prices by approximately 40%.

WuXi Biologics

Geopolitical Resilience: Despite being a focal point of the U.S. BIOSECURE Act, WuXi Biologics demonstrated remarkable stability.

Ireland as a Safe Harbor: Its Dundalk, Ireland facility became a strategic hub for Western clients, reaching full capacity and achieving profitability ahead of schedule.

Operational Decoupling: The company effectively de-coupled its manufacturing operations, ensuring that sensitive projects for U.S. clients were managed by non-Chinese entities within the global WuXi ecosystem.

Westernization Strategy: This may involve spinning off its European and Singaporean units into a separate, independent legal entity. Such a move would be a strategic necessity to retain Tier-1 Big Pharma clients who require a supply chain completely insulated from U.S.-China geopolitical tensions.

Akeso

Platform Validation: The success of Ivonescimab (AK112, partnered with Summit Therapeutics) provided definitive proof-of-concept for Akeso’s proprietary TETRA-Ig platform, establishing it as a world-leading technology in bispecific antibody engineering.

Clinical Success: The landmark HARMONi-2 trial against Keytruda generated significant buzz, positioning Ivonescimab as a potential best-in-class agent in PD-1/VEGF inhibition.

Pipeline Expansion: The primary goal for 2026 is expanding the clinical utility of Ivonescimab beyond non-small cell lung cancer (NSCLC) into new tumor types, including gastric cancer and triple-negative breast cancer (TNBC).

Innovent Biologics

Market Dominance: Innovent successfully transitioned from a pure oncology firm to a leader in metabolic diseases. Its GLP-1/GIP agonist, Mazdutide (IBI362), became a major brand name in China, generating unprecedented demand and establishing the company as a key player in the obesity and diabetes market.

Cash Flow Anchor: The PD-1 inhibitor Tyvyt (Sintilimab), partnered with Eli Lilly, continued to maintain its strong position on China’s National Reimbursement Drug List (NRDL), providing reliable cash flow.

U.S. Expansion: Leveraging the existing partnership with Eli Lilly, the company will initiate critical Phase 2/3 trials for Mazdutide in the U.S., aiming to position it as a compelling value-driven alternative to the market leaders, Zepbound and Ozempic.

WuXi AppTec

Financial Resilience: Despite the BIOSECURE Act headwinds, the company achieved record net profits by focusing on its core small-molecule CRDMO business, particularly its high-growth TIDES (peptide and oligonucleotide) platform.

Strategic Divestment: WuXi AppTec sold off its Advanced Therapy Unit (ATU)—its US-based cell and gene therapy business—to Altaris in early 2025. This removed a major target of U.S. legislative scrutiny.

AI: A key theme for 2026 is the transition toward Agentic AI in drug discovery. WuXi is leveraging its long-standing investments in AI firms like Insilico Medicine to offer high-margin research software and services.

Sino Biopharm

Modernizing the Portfolio: Sino Biopharm acted as a major market consolidator, acquiring LaNova Medicines in July 2025 for $500 million to secure world-class ADC and bispecific antibody platforms.

Revenue Milestone: The company reached a tipping point where innovative products became the primary growth engine, with innovative drug sales rising 27% year-on-year in the first half of 2025. (Company data, Mirae Asset, January 2026)

Cardiovascular Focus: In January 2026, Sino Biopharm acquired Hygieia Biomedical for RMB 1.2 billion, gaining its ultra-long-acting siRNA platform. The 2026 focus will be the commercialization of Kylo-11, a potential best-in-class Lp(a) inhibitor.