Asia’s Dominance in the Semiconductor Industry

Overview

Asia’s presence in the global semiconductor industry cannot be ignored – the region accounts for 60% of global semiconductor sales. (Deloitte, 2020)

While the production of semiconductors has fallen in the West, the Asia region has cultivated dominant industry leaders from South Korea, Japan, China and Taiwan.

South Korea’s Market Dominance

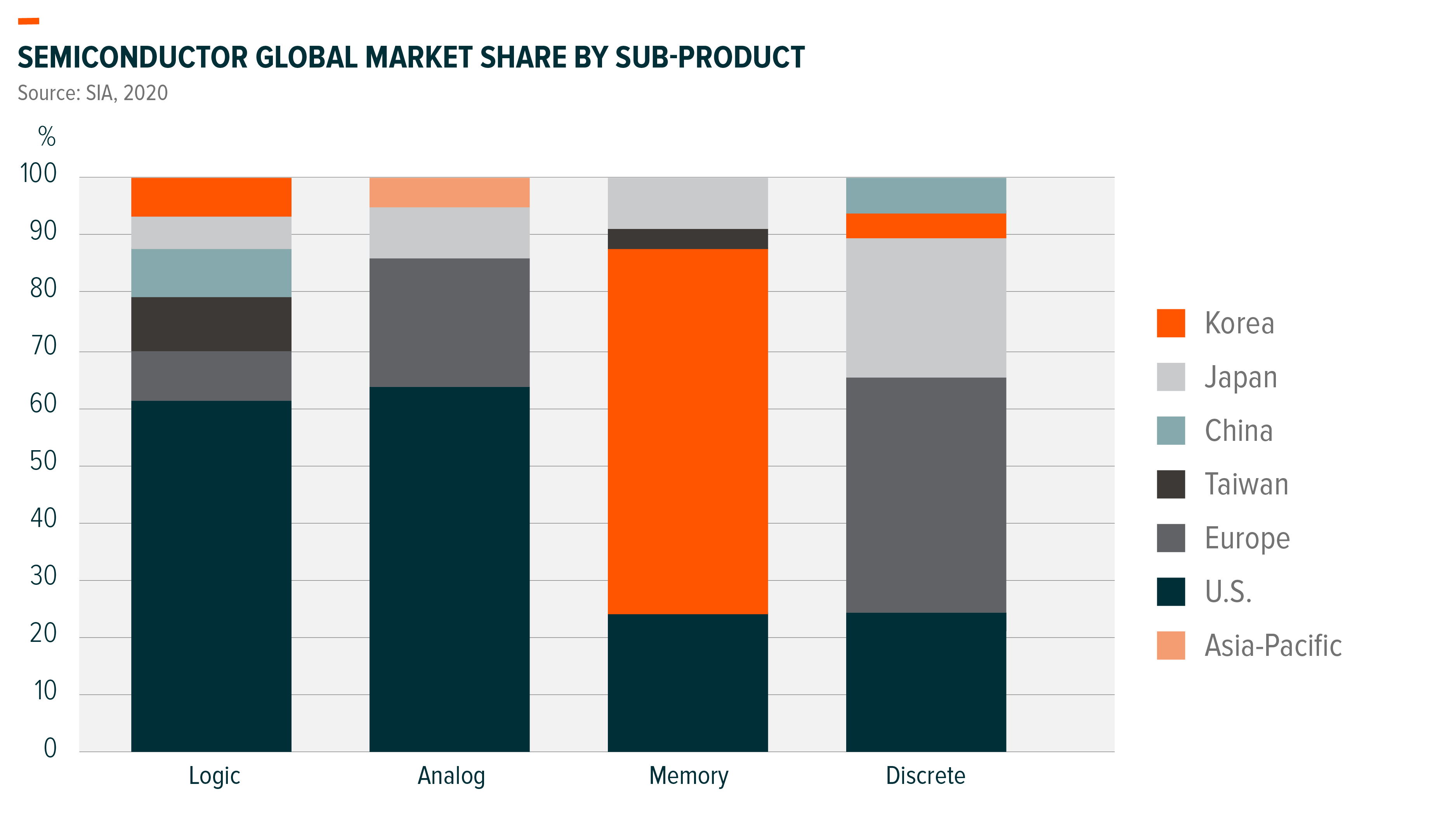

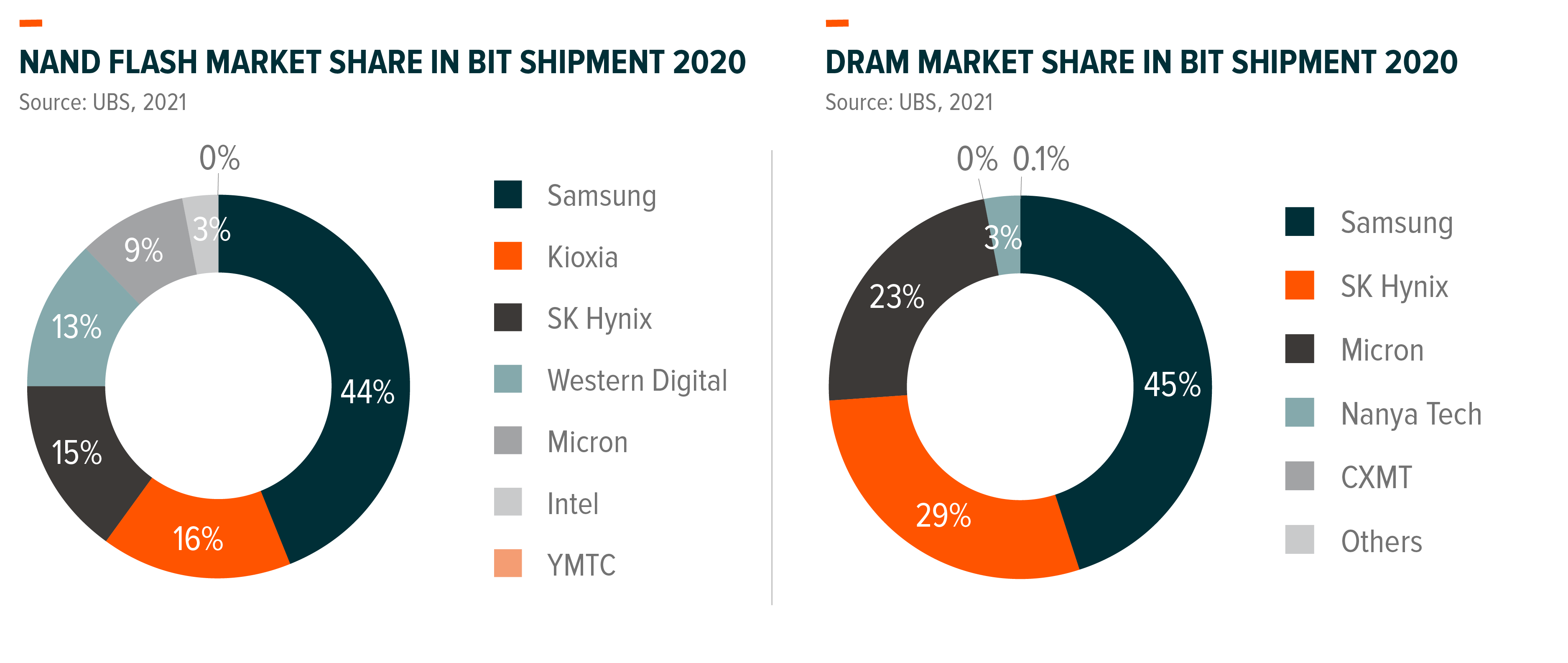

South Korea has built up a dominant market share in memory, leading the effort to migrate memory technology and cutting cost per bit. In 2020, Samsung and SK Hynix combined accounted for 74% of DRAM (dynamic random access memory) market by bit shipments, and 59% market share in NAND (UBS 2021). South Korea also has a sizable foundry business and domestic industry supply chain to support the local ecosystem.

Taiwan’s Progression to Top Chip Maker

Taiwan has developed a well-connected manufacturing supply chain that incorporates semiconductors to hardware. The region’s competitive edge involves chip manufacturing, raw wafer production, integrated circuit (IC) design, outsourced semiconductor assembly and test (OSAT) companies that offer third-party testing services.

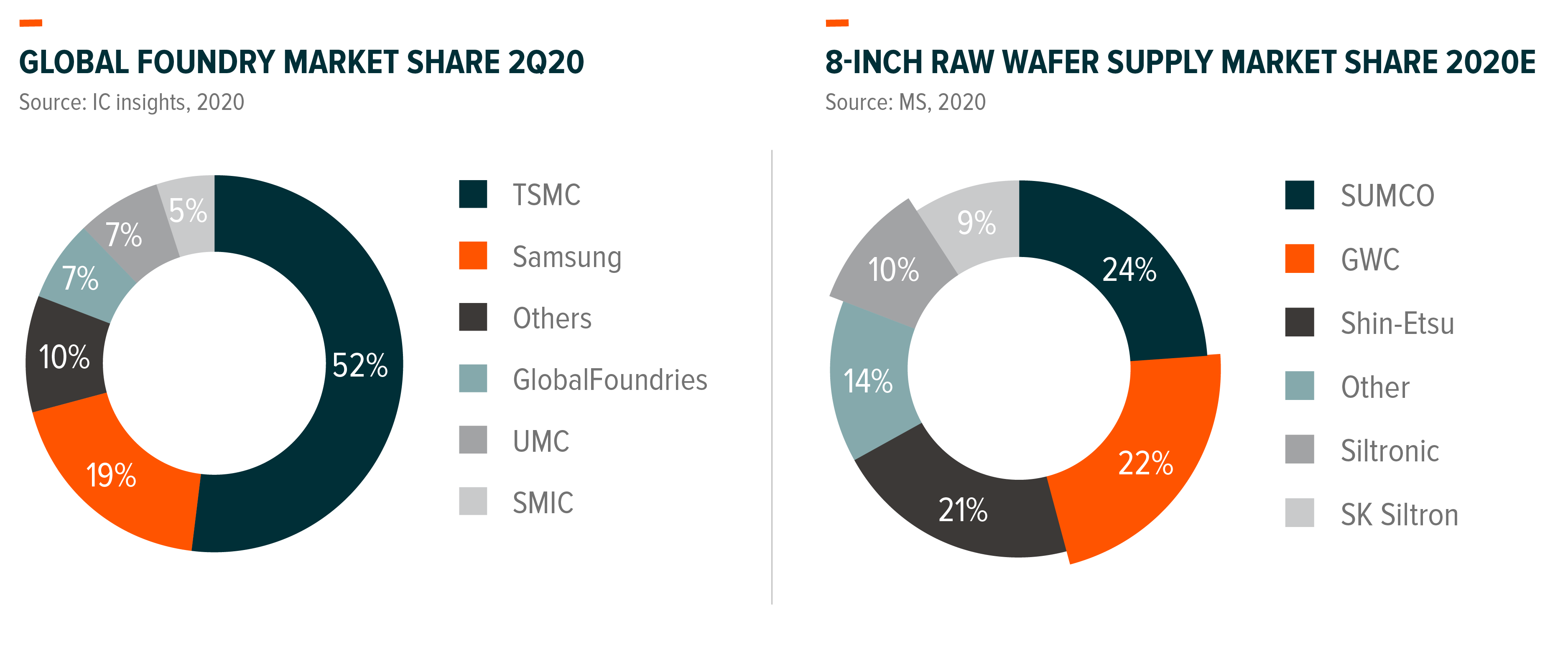

One of the most notable leaders is Taiwan Semiconductor Manufacturing Company (TSMC), which has gained the largest market share in the foundry business and continues to be the technology leader in node migration. MediaTek is one of the two major suppliers in smartphone SoC (system on chip). GlobalWafers, after the acquisition of Siltronic, will have a 25% market share in the raw wafer market, the second-largest globally behind SUMCO in Japan. (MS, 2020)

A Turning Point for China’s Semiconductor Industry

Although China’s global market share in the semiconductor space remains relatively low at the moment, supportive government measures will likely give China the backing to catch up with its competitors. China has already invested RMB 650 billion since 2014 through its state-owned sector investment fund, the National IC Industry Investment Fund (“The Big Fund”). We see a continuous flow of funding and talents to support foundries, fabless companies and other semiconductor companies in China.

Japan Becomes Upstream Specialist

Japan’s strengths in the semiconductor industry include raw materials and equipment.. Upstream semiconductor companies that involve chip fabrication plants and designers like Shin-Etsu and HOYA are global leaders. Tokyo Electron is one of the top three semiconductor equipment makers globally, while Sony remains a leader in image sensor technology.

The Rise and Fall of Japan’s Technology Journey (1970-2000)

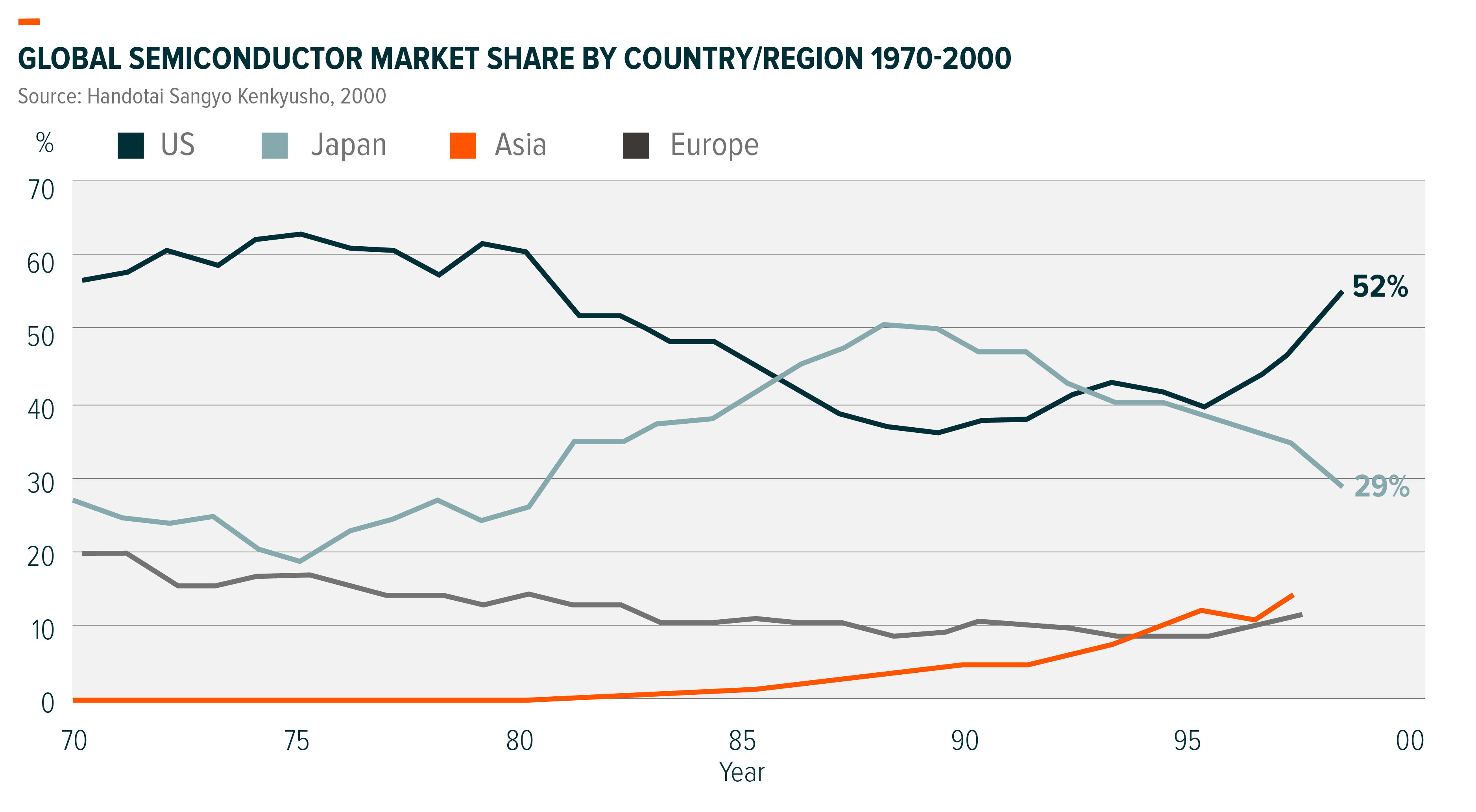

Under the guidance of the Japanese government between 1987 and 1979, Japan began to implement the VLSI (very large-scale integrated circuit) research project. The project was led by the five largest semiconductor companies in Japan (Hitachi, Mitsubishi, Fujitsu, Toshiba, and NEC) along with a 72 billion yen investment. As a result, the top-level research project made industry-first breakthroughs in core generic technology, Japan became a leader in in DRAM technology with the launch of 64Kb, 256Kb, and 1Mb DRAM products in the 1980s. Japan had over 80% of DRAM market share in 1987 (Global Times, 2019), while also surpassing the US in global semiconductor market share – at 48% for Japan vs 39% for the US. (Handotai Sangyo Kenkyusho, 2000)

We think several factors contribute to the decline of Japan’s semiconductor industry in the 90s: 1) The ongoing US-Japan trade war and the US-Japanese Semiconductor Agreement in 1986 brought unfavourable tax rates and currency impact to Japanese DRAM makers, 2) Semiconductor companies in Japan did not have a diversified product portfolio, with a high concentration in DRAM. As downstream demand in PC took off, other semiconductor products like CPU (central processing unit) and GPU (Graphics processing unit), became more important. 3) Memory producers continued to close the cost gap with Japanese makers.

South Korea and Taiwan Build Semiconductor Legacy, Chip by Chip (1990-2020)

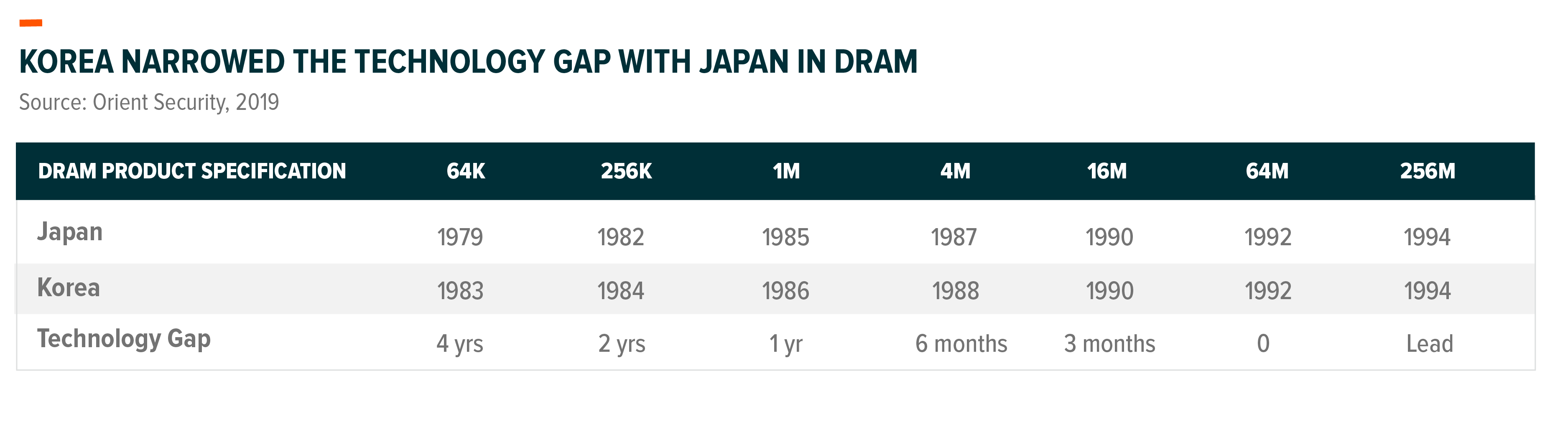

South Korean companies invested heavily in research and development (R&D) in an attempt to catch up with Japan’s advancements in memory technology. Samsung, for example, had an average capital expenditure over revenue ratio at around 40% between 1987-1992, compared to the industry average of 21%. (Monolithic, 2011) The technology gap between South Korean and Japanese companies narrowed from four years in 1983, to zero in 1992 with the launch of 64M DRAM, which was typically used in large-capacity multimedia systems at the time.

Before TSMC was founded in 1987, most integrated circuit companies operated an IDM (integrated circuit manufacturer) business model that involved the design and manufacturing process all under one roof. TSMC and other foundries later established a developed business model that involved separating the chip design process from manufacturing. Over time, Taiwanese companies have been able to leverage the region’s relatively lower labour costs to ramp up semiconductor manufacturing.