Important Information

Investors should not base investment decisions on this material alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- The investment objective of Global X Gold Covered Call Active ETF (the “Fund”) is to generate income by primarily providing exposure to gold futures and/or exchange traded funds tracking the price of gold (collectively, the “Gold Performance”) with a covered call strategy. The Fund will use a synthetic investment strategy by investing up to 100% of its Net Asset Value in fully funded total return swaps.

- This synthetic investment strategy exposes the Fund to counterparty risk including under collateralisation risk, default risk, intra-day counterparty risk, early termination of swaps risk and change of swap fees risk.

- The Fund invests more than 50% and up to 100% of its Net Asset Value in FDIs. Associated risks include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk.

- The Fund employs an actively managed investment strategy. The Fund may fail to meet its objective as a result of the implementation of investment process which may cause the Fund to underperform as compared to direct investments in the constituent equity securities of the Reference Index.

- The Fund’s opportunity to benefit from the increases in the Gold Performance will be limited the strike price of the referenced Gold Call Options plus the notional premium. In rapidly rising markets, this limitation may result in the Fund underperforming the Gold Performance. Conversely, the Fund remains exposed to declines in the Gold Performance, as the covered call strategy embedded in the swap does not provide full downside protection.

- If the fund is unable to obtain sufficient exposure to Gold Performance due to the limited availability of swaps, the Fund may suspend creations, which could cause the Fund to trade at a significant premium or discount.

- The investments of the Sub-Fund are concentrated in the performance of gold generally and will result in large concentration risk.

- Potential conflicts of interest may arise as the Manager and one of the Swap Counterparties are members of the same group.

- The markets on which the gold futures, Gold ETFs and listed Gold Call Options are traded and the SEHK may have different trading hours. The Fund’s value may change on days when investors will not be able to purchase or sell the Fund’s Shares.

- The trading price of the Fund’s unit on the SEHK is driven by secondary market trading factors, which may lead to a substantial premium or discount to the Fund’s net asset value.

- The Fund may be terminated early under certain circumstances (e.g., if NAV falls below HK$50 million), which could result in a loss of investment.

- The Manager may at its discretion pay dividends out of the capital of the Fund. Distributions paid out of capital, represent a return of an investor’s original investment or its gains and may potentially reduce the Fund’s Net Asset Value per Share as well as the capital available for future investment.

Global X Gold Covered Call Active ETF (3533): FAQ

Q: what is the fund for?

This is a covered call strategy focused on gold. To executing the strategy, we use synthetic contract with swap partners who hold gold future in long position and gold futures call option in short position.

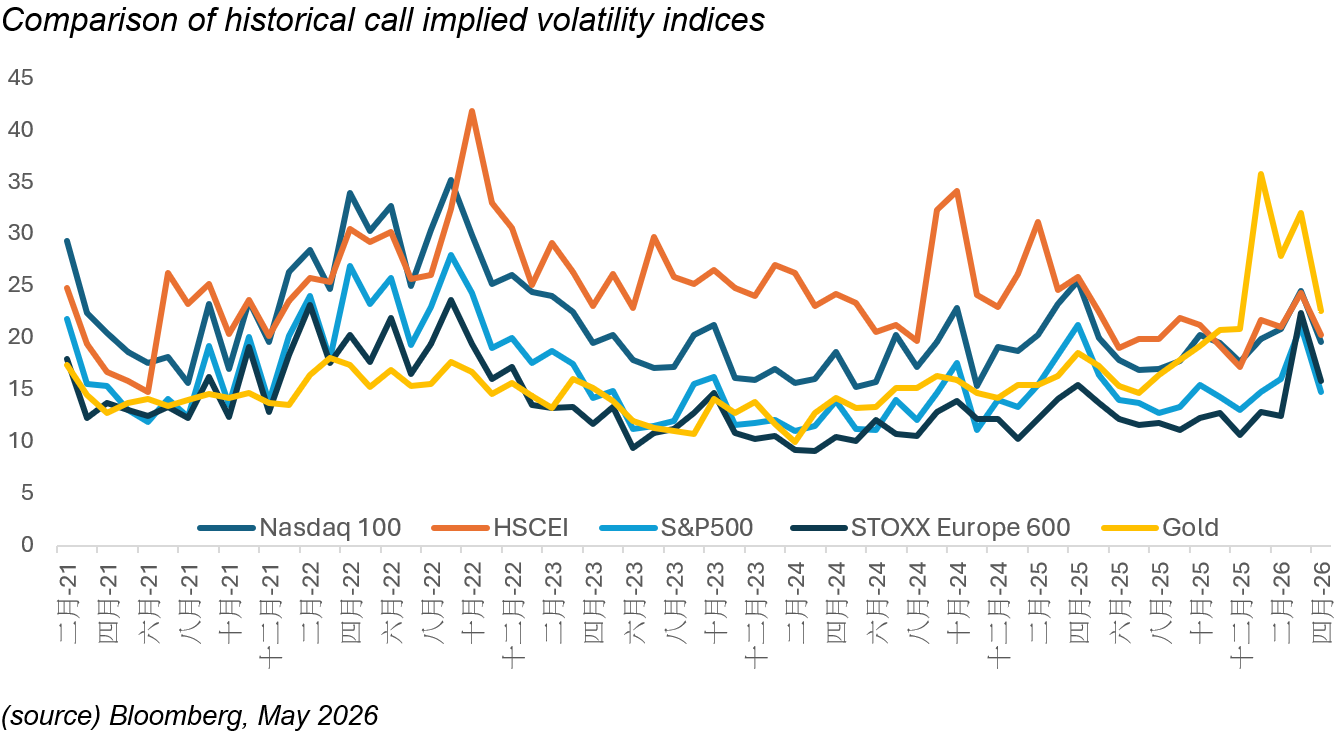

Q: Isn’t gold a low-volatility asset?

Historically, gold was viewed as a “low-volatility” asset compared to equity indices. Yet, even during calmer market regimes, annualized gold call option premiums remained remarkably robust, averaging 18% over the past 15 years.

Recently, gold’s market dynamics have shifted significantly. In the last 12 month till April 2026, gold’s call implied volatility has surged to 21.7% on average, occasionally exceeding that of major equity indices like S&P500. This elevated volatility makes selling options an increasingly attractive strategy for generating yield.

Gold historical call implied volatility

| historical call implied volatility | |

|---|---|

| May 2011~ April 2026 | 18.1 |

| May 2025 ~April 2026 | 21.7 |

(source) Bloomberg, May 2026

Q: Why has gold transitioned into a high-volatility asset?

The structural catalyst for this volatility regime shift is the proliferation of gold ETFs. By democratizing access to the precious metal, these vehicles have empowered retail investors to exert a disproportionate influence on intraday price discovery. This influx of speculative retail capital introduces high-velocity momentum trading, triggering significantly sharper and more frequent price swings than traditional, institutional-led market behaviours historically generated.

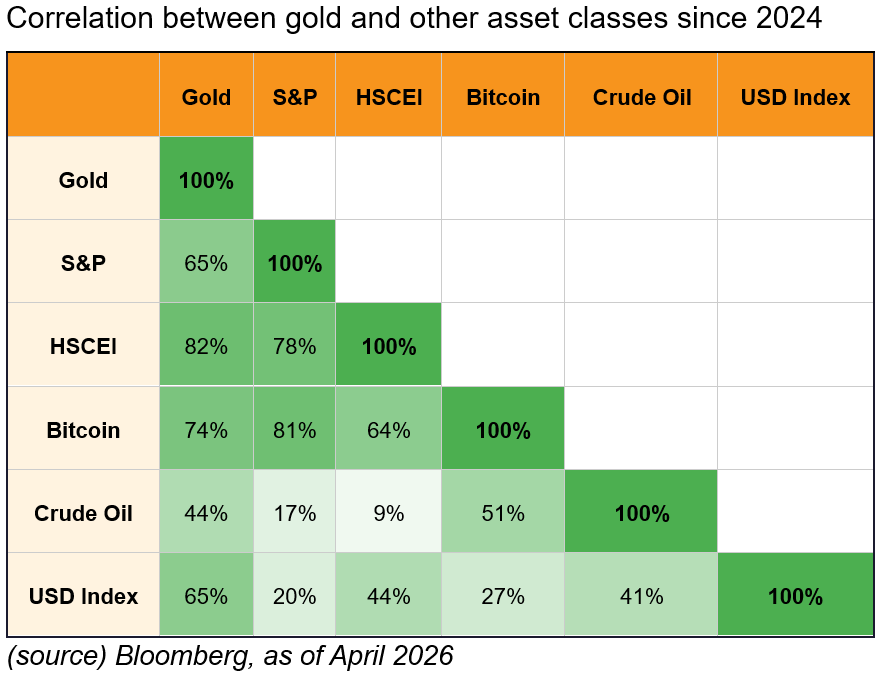

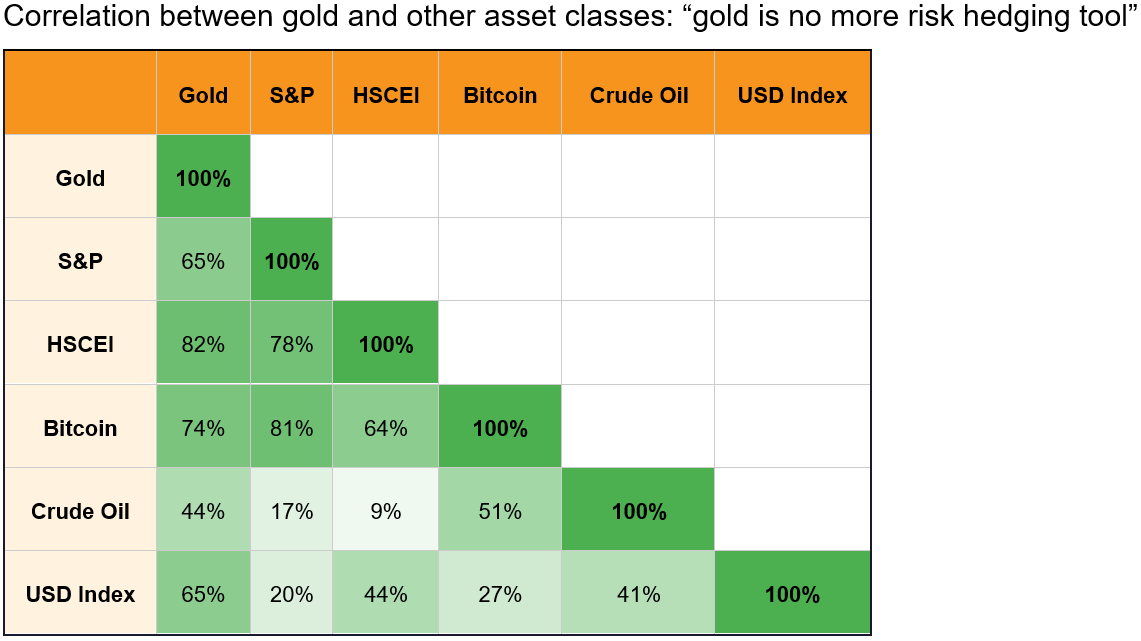

Q: Is gold changing its status as an asset class?

Gold’s traditional negative correlation with equities and the USD seemed weakened (see below table), as it now frequently moves in tandem with other asset classes. In this environment, “pure” gold no longer provides the same diversification benefits.

Q: What are the key investment points of this ETF?

Point 1: High Income Generation through Option Premiums

This ETF is designed as an income-generating product. By utilizing a covered call strategy, it targets an annualized premium income of approximately 20~22%, based on data from COMEX (under CME group). It provides a consistent yield component—monetizing gold’s volatility in a way that traditional “buy-and-hold” gold ETFs cannot.

Point 2: offering cushion to other asset volatility

The traditional inverse correlation between gold, equities, and the USD has shifted, with gold now frequently moving in tandem with other asset classes. In this environment, “pure” gold no longer provides the same diversification benefits.

The covered call strategy may provide diversification tool to general asset classes; the gold option premium collected acts as a defensive buffer, offering a “cushion” against market volatility that traditional gold exposure currently lacks.

Point 3. A First-of-its-Kind Product in Greater China exchanges

Despite the Greater China region (Mainland bourses and HKEX) hosting over 20 Gold ETFs with an AUM exceeding $40 billion USD, there is no differentiated gold ETF.

This is the first and only Gold Covered Call ETF in the region, offering a sophisticated, differentiated alternative for investors seeking more than just spot price exposure.

Q: Is the impact of ETFs on gold price volatility significant?

While ETFs hold only 2% of global gold stocks, they have become the primary drivers of market momentum in 2026, serving as a high-velocity “liquidity engine.”

Notably, ETF trading now accounts for 3.5% of total volume compared to just 1% a decade ago. While this may seem minor, it represents a meaningful structural shift.

Unlike the opaque Over-the-Counter (OTC) market—which accounts for 50–70% of total volume—ETFs trade in real-time on public exchanges. This creates a “public signal” that triggers automated algorithmic selling in the much larger futures and OTC markets, establishing a “price discovery” benchmark that amplifies global price movements.

Similarly, unlike cash-settled futures—which represent 30–40% of daily trading—physically backed ETFs must hold bullion to match their share count. When demand spikes, they must source physical bars from a relatively “thin” physical market, competing directly with central banks and jewelry makers for a limited supply, which forces spot prices higher.

The structural rise of 2x and 3x leveraged ETFs adds further volatility by necessitating massive rebalancing in the final hour of the trading day.

Gold trading volume mix

| Segment | Daily Vol | % of Total Volume | Note |

|---|---|---|---|

| Over-the-Counter | $270~$375 bn | 50%~70% | Predominantly institutional and opaque; centered in London (LBMA) |

| Futures & Options | $160~210 bn | 30%~40% | Mostly cash-settled; dominated by COMEX and SHFE |

| ETFs | $20 bn | ~3.5% | High-velocity, real-time price discovery and physically backed |

| Total | ~$536 bn | Total observable liquidity across all global venues |

(Source) WGC, London bullion Market Association, CME

Q: what’s the risk of the fund?

The primary risk is the capped upside potential. Because this is a covered call strategy, the fund will underperform “pure” gold during a sharp bull market, as the gains are limited by the strike price of the written options.

Regarding downside risk, while the option premiums provide a “cushion” that reduces losses compared to a standard gold position, this protection is limited. In a significant market sell-off, the premium income may not be sufficient to offset the decline in the gold price, which can still result in a negative total return.

Additionally, as the fund deals in gold futures, it is subject to market volatility and liquidity risks inherent in the derivatives market.

Q: while it is an actively managed fund, what is the soft guidance on how Global X HK will manage the ETF, regarding the call option cover ratio and moneyness?

Regarding moneyness and coverage, the fund targets a 100% cover ratio at launch and will write monthly call options close to At-the-Money.

Post-launch, the portfolio management team may dynamically scale the cover ratio between 50% and 100% depending on market situation. Additionally, the team may write further Out-of-the-Money options when market indicators flag strong upside momentum, allowing the fund to capture greater capital appreciation from the gold price.

Q: Why does the fund utilize COMEX gold futures and options?

COMEX (under CME group) serves as the global benchmark for gold derivatives by offering deep liquidity. Its status as the largest institutional order book worldwide ensures minimal transaction costs and low slippage for fund allocations.

Q: Why use a swap structure? Wonder it could cause any additional cost to investors? Who are the counterparties?

The fund uses a total return swap structure to optimize operational efficiency and reduce trading costs. The swap passes complex tasks like managing futures margins, daily settlements, and options assignments directly to our brokers, allowing the fund to cleanly receive the net performance.

The swap shifts execution to prime brokers, who use internal liquidity and global desks to hedge more efficiently. This will help our portfolio management team to focus strictly on strategy optimization.

Investors do not bear any additional costs from this setup, as the fund’s total expense ratio (TER) is capped at 75 basis points, and any cost overrun will be borne entirely by Global X HK

To mitigate counterparty risk, the fund partners with institutional leaders including J.P. Morgan, Citi, and Mirae Asset Securities, with possibility to add more partners in the future.