Important Information

Investors should not base investment decisions on this content alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X China Electric Vehicle and Battery ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Electric vehicle companies invest heavily in research and development which may not necessarily lead to commercially successful products. In addition, the prospects of Electric vehicle companies may significantly be impacted by technological changes, changing governmental regulations and intense competition from competitors.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X Hang Seng TECH ETF (the “Fund”) seeks to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Hang Seng TECH Index (the “Index”).

- The Fund’s investments are concentrated in companies with a technology theme. Technology companies are often characterised by relatively higher volatility in price performance. Companies in the technology sector also face intense competition, and there may also be substantial government intervention, which may have an adverse effect on profit margins. These companies are also subject to the risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences.

- The Fund’s investments are concentrated in securities listed on the Stock Exchange of Hong Kong (the “SEHK”) of companies that are active in technology sector may result in greater volatility in the value of the Fund than more diverse portfolios which comprise broad-based global investments. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the technology sector.

- The Index is subject to concentration risk as a result of tracking the performance of securities incorporated in, or with majority of revenue derived from, or with a principal place of business in, the Greater China region. The Fund’s NAV is therefore likely to be more volatile than a broad-based fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- The trading price of the Fund unit (the “Unit”) on the SEHK is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- Dividends may be paid from capital or effectively out of capital of the Fund, which may amount to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment and result in an immediate reduction in the Net Asset Value per Unit of the Fund.

- Global X China Clean Energy ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Many clean energy companies are involved in the development and commercialization of new technologies, which may be subject to delays resulting from budget constraints and technological difficulties. Obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants and general economic conditions also significantly affect the clean energy sector.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Consumer Brand ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- The performance of companies in the consumer sector are correlated to the growth rate of the global market, individual income levels and their impact on levels of domestic consumer spending in the global markets, which in turn depend on the worldwide economic conditions, which have recently deteriorated significantly in many countries and regions and may remain depressed for the foreseeable future.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Robotics and AI ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Robotics and artificial intelligence sector is sensitive to risks including small or limited markets for such securities, changes in business cycles, world economic growth, technological progress, rapid obsolescence, and government regulation. These companies rely on significant spending on research and development and tend to be more volatile than securities of companies that do not rely heavily on technology.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Cloud Computing ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Companies in the internet sector may face unpredictable changes in growth rates and competition for the services of qualified personnel. The products and services offered by internet companies generally incorporate complex software, which may contain errors, bugs or vulnerabilities.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Semiconductor ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Semiconductor industry may be affected by particular economic or market events, such as domestic and international competition pressures, rapid obsolescence of products, the economic performance of the customers of semiconductor companies and capital equipment expenditures. These companies rely on significant spending on research and development that may cause the value of securities of all companies within this sector of the market to deteriorate.

- China is an emerging market. The Fund invests in Chinese companies which may involve increased risks and special considerations not typically associated with investments in more developed markets, such as liquidity risk, currency risks, political risk, legal and taxation risks, and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X China Little Giant ETF’s (the “Fund’s”) objective is to provide investment results that, before fees and expenses, closely correspond to the performance of the Solactive China Little Giant Index (the “Index”).

- The Index is a new index. The Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history.

- The Fund may invest in small and/or mid-capitalisation companies which may have lower liquidity and their prices are more volatile to adverse economic developments than those of larger capitalisation companies in general.

- The Fund’s investments are concentrated in companies which are characterised by relatively higher volatility in price performance. The Sub-Fund may be exposed to risks associated with different sectors and themes including semiconductor, industrial, pharmaceutical, energy and technology. Fluctuations in the business for companies in these sectors or themes will have an adverse impact on the net asset value of the Sub-Fund.

- Some of the companies classified as the Little Giants have a relatively short operating history. Such companies also face intense competition and rapid changes could render the products and services offered by these companies obsolete, which may have an adverse effect on profit margins.

- They may be more susceptible to risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences affecting those companies.

- The Mainland China is an emerging market. The Fund invests in Mainland Chinese companies which

- may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risk, currency risks or control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk and the likelihood of a high degree of volatility.

- Securities exchanges in the Mainland Chinese markets typically have the right to suspend or limit trading in any security traded on the relevant exchange. The government or the regulators may also implement policies that may affect the financial markets. All these may have a negative impact on the Fund.

- Listed companies on the ChiNext market and/or STAR Board are subject to higher fluctuation on stock prices and liquidity risk, over-valuation risk, less stringent regulation risk, delisting risk and concentration risk.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Fund.

- The trading price of the Shares on the SEHK is driven by market factors such as the demand and supply of the Shares. Therefore, the Shares may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Share of the Fund and will reduce the capital available for future investment.

Monthly Commentary on China Thematic ETFs – Aug 2024

Global X China Electric Vehicle and Battery ETF (2845 HK)

Industry Update

- Solid July EV Sales; NEV penetration close to 50%: According to CPCA estimate, July passenger NEV wholesale volume reached 950k, +29% YoY.1 Individual auto brands reported divergent July Sales. BYD reported July NEV sales of 341k units, +31% YoY, with PHEV continuing to record strong growth. Overseas sales reaccelerated to 30k units from 27k units last month.2 Li Auto delivered 51k units in July, +49% YoY and reaching a historical high level. Nio (flat YoY) and Xpeng (+1% YoY) recorded softer sales momentum in July. (for reference only, abovementioned stocks are not necessarily in the constituent list of the ETF). Based on insurance registration, new energy vehicle (NEV) penetration was 48% in the last week of July.3

- Auto trade-in program upgraded: The trade-in stimulus has been doubled to Rmb20k (from Rmb10k) per NEV, and Rmb15k (from Rmb7k) per eligible ICEV,4 following central government’s indication that long-term government bonds could be used to fund consumer goods trade-in.5 More than 113k vehicles sold from 26 April to 25 June applied for the trade-in subsidy, according to Ministry of Commerce.

- Battery material costs further declined in July: China’s spot lithium carbonate price declined by 6% MoM to around RMB 87 k/t at the end of June.6 Battery materials prices have decreased by over 80% from its peak in 2022, supporting the continued cost optimization for battery makers and EV manufacturers.7

Stock Comments

- CATL’s share price was up 3.5% in July, a positive contributor to the ETF. CATL reported solid 2Q24 results on 27 July. Net profit of Rmb12.3bn was +13% YoY7 on both battery sales and margin expansion, with unit profit for both EV and ESS batteries remained stable QoQ. New products Shenxing and Qilin are taking up 30-40% of total EV battery sales volume, and management expect the ratio to rise further. 8

Preview

We remain positive on the long term growth potential for EV and battery value chain, along with the upward EV penetration trajectory. Domestic old car replacement demand, as stimulated by scaled-up auto trade-in program, together with export sales, should support China’s resilient auto momentum and benefit leading domestic brands. We expect the China auto market to stay competitive in 2024 with strong new product line-up and technology innovations from leading EV and battery brands, and new entrants such as Xiaomi. Geopolitical tensions remain the key risks, but China EV models will still remain competitive under new tariff landscape thanks to its cost advantages. Localized production will be the longer term solution for Chinese brands.

Global X Hang Seng TECH ETF (2837 HK)

Industry Update

- Hang Seng TECH Index recorded a 0.8% loss in July 2024, after rallying over 30% from the troughs in January to the highs in mid May. EV startup brands recorded solid returns thanks to solid volume growth and share gain, while OTA recorded underperformance due to slowing travel demand growth on the high base last year. Weak domestic consumption sentiments also weigh on performance of consumption brand in July.

Stock Comments

- Alibaba recorded return of +9.7% in July, a key contributor to the index. Taobao Tmall Group GMV growth should reaccelerate in 2Q thanks to its low price strategy with Alibaba’s continued investments, and international commerce business should maintain solid growth momentum.9 On 26 July, Taobao Tmall announced several new monetization announcement, including charging a new 0.6% service fee on net GMV and removing annual fixed fee for Tmall merchants. The new regulation should accelerate Alibaba’s monetization on Tmall merchants, and attract more new merchants to Tmall platform.10 Potential inclusion into Stock Connect Scheme in September is also a catalyst for Alibaba share price performance.

- Baidu recorded return of 2.9% in July, as supported by the heated discussion on its Robotaxi business over the past few weeks. Baidu launched its 6th-generation Robotaxi in May, and is recording increasing order volume and improving unit economics, thanks to operational efficiency improvements and increasing mix of fully driverless order. Fully driverless order mix increased to 70% in Wuhan in April, and is expected to rise to 100% in the coming quarters.11

Preview

Although China internet sector is entering a mature stage with the already high online penetration and peaking timespent, there are still emerging themes driving re-accelerating growth across different subsectors, on the back of a normalizing domestic regulatory environment on internet platforms. A robust game pipeline and solid new game performance is driving more positive online gaming outlook. Ad tech upgrades and the emergence of more effective ad formats should support the continued market share gain by key online advertising platforms, and the applications of AI across cloud, games, ads, and other key sectors is driving new demand and enhancing operational efficiency. Continued execution of upsized share repurchase program increases shareholder returns and should provide supports for future share price performance.

Global X China Clean Energy ETF (2809 HK)

Industry Update

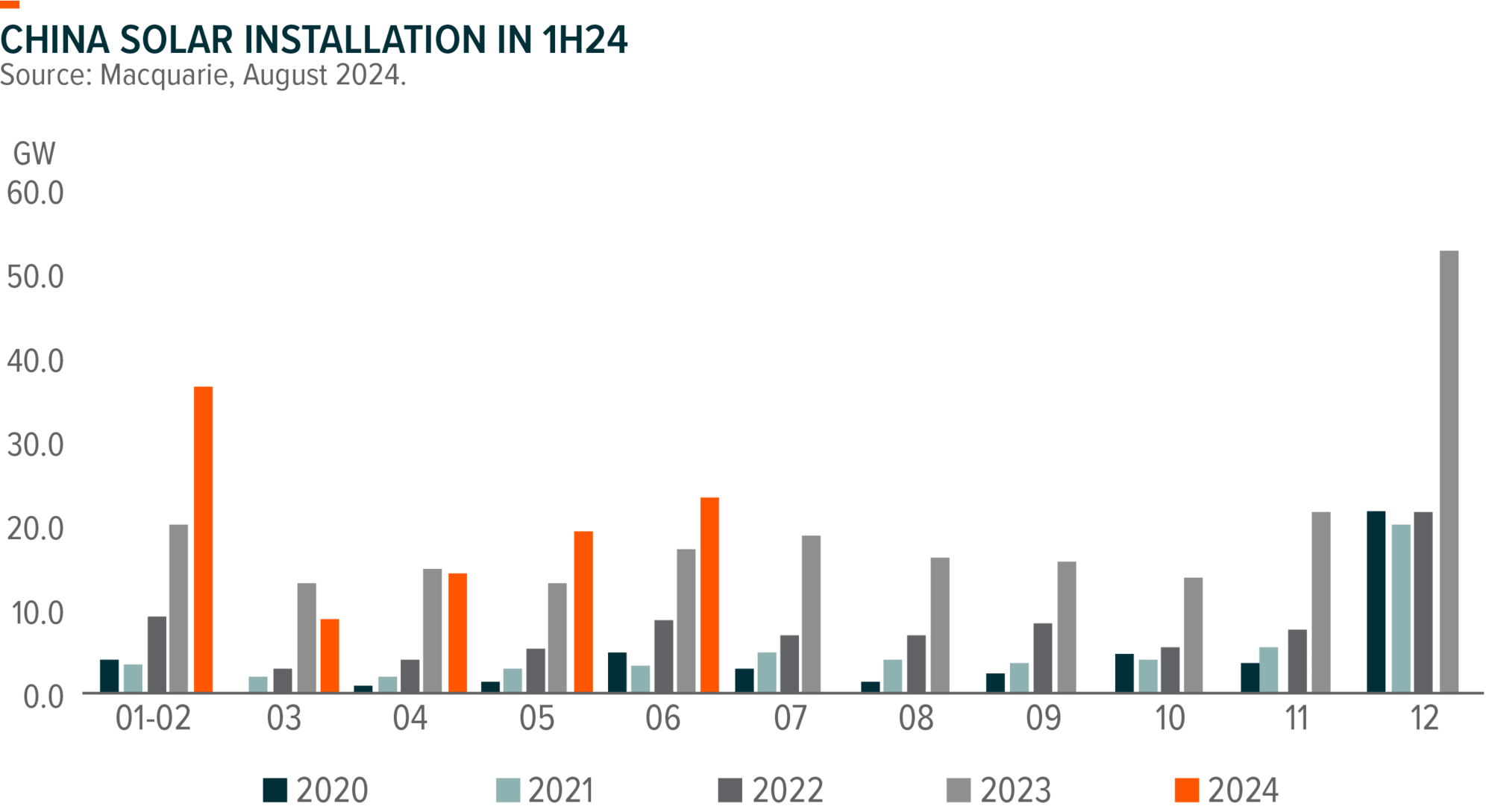

- China power demand growth rose by 8.1%yoy to 4,658bn KWh in 1H24, while China added 153GW of power capacity, +14%yoy including 102.5GW solar and 25.8GW wind, +31%yoy and 12%yoy, respectively. China also significantly increased the investment in power grids to Rmb600bn in 2024, to better utilize the power generation by renewables.We witnessed wind sector rally due to positive progress on the multiple offshore wind projects recently. Most of the offshore wind farms in the pipeline are in deep and far sea areas which are likely to start construction over the 15th Five-Year Plan(2026-2030E). On solar side, supply chain prices remain sluggish due to oversupply. Polysilicon, wafer, cell and module players are still bleeding, despite strong volume growth. We have seen some small players start to exit and more new capacities plan get deferred or cancelled.

Stock Comments

- Ningbo Deye Technology: The company is one of the key exporters who are selling residential solar inverters to Europe and other major overseas market. Thus, company benefits from global solar installation accelerating, especially after destocking in Europe. In 1H24, company still maintained solid revenue and earnings YoY growth.

- China Three Gorges Renewables: The company is a leading wind farm operator in China, who benefits from wind manufacturing cost decline. It was also seen as a defensive play with power generation output growth as utilities name.

- TCL Technology Group: The company was one of the top two solar wafer makers in China who suffered from severe wafer oversupply currently. Gross margin in wafer end turns negative this year. It takes time for small players to exit

Preview

We remain constructive on the global clean energy growth and the trend of energy transition. However, we also must admit the near-term broad mismatch between supply and demand along solar/wind supply chains, which led to poor earnings for a couple of months or maybe even longer. It takes more time than expected for the small players to exit and demand to catch up, especially when China solar value chain are faced with geopolitical pushback from the United States. On the bright side, we have seen strong demand from some emerging markets like ASEAN, Middle East regions, Africa and South America, but it still needs more time.

Global X China Consumer Brand ETF (2806 HKD)

Industry Update

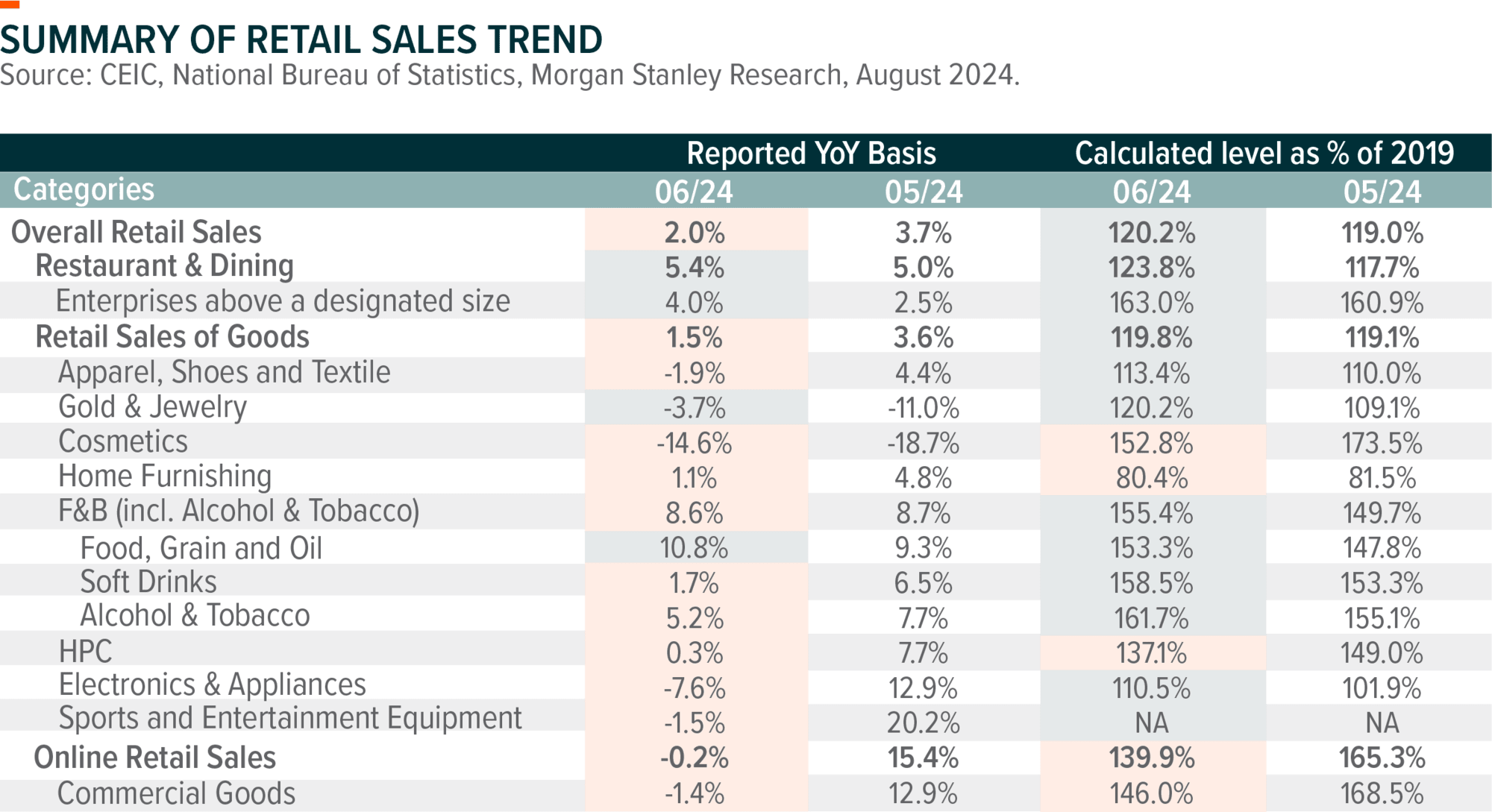

In June, China’s retail sales growth slowed to +2% YoY, compared to a rebound of 3.7% YoY in May. Sectors such as Cosmetics, Sports & Entertainment Equipment, and Electronics & Appliances exhibited noticeable deceleration in YoY growth, possibly due to growth normalization post an earlier 618 online shopping festival and subdued consumption sentiment. Restaurant & Dining and Food, Grain, and Oil experienced a slight acceleration in growth. The YoY decline in Gold & Jewelry also narrowed as gold prices stabilized.

In July, we observed positive indications in policy trends. The NDRC and MoF jointly announced to support the trade-in of appliances and large industrial equipment (such as trucks, buses, ships, etc.) with ultra-long-term special treasury bonds amounting to Rmb300billion. In the July Politburo meeting, boosting consumption was highlighted as a key priority in the second-half policy directives. The announcement emphasized a shift in policy focus towards bolstering household livelihood support and promoting service consumption.

Stock Comments

- Techtronic Industries recorded gain of 6% in July. Techtronic’s well-diversified capacities and strategic battery procurement position it well to navigate potential trade frictions effectively. Coupled with a seamless CEO transition, Techtronic’s fundamentals remain intact on its leadership in cordless technology transformation.

- Li Auto recorded gain of 9% in July thanks to robust sales and order performance, particularly with its L6 model since late June. Li Auto could further enhance its market presence in lower-tier cities through channel growth and the competitive pricing, especially as its primary competitor, BBA, grapples with issues related to channel management and price war. Additionally, Li Auto enhanced its NOA feature in July, which is now accessible on all roads nationwide, significantly narrowing the gap with industry leaders.

- Trip.com Group corrected 16% in July, underperform HSTECH of 1% decrease. This is mainly due to deteriorating domestic RevPAR and concerns about the impact spreading to its outbound business.

Global X China Robotics and AI ETF (2807 HK)

Industry Update

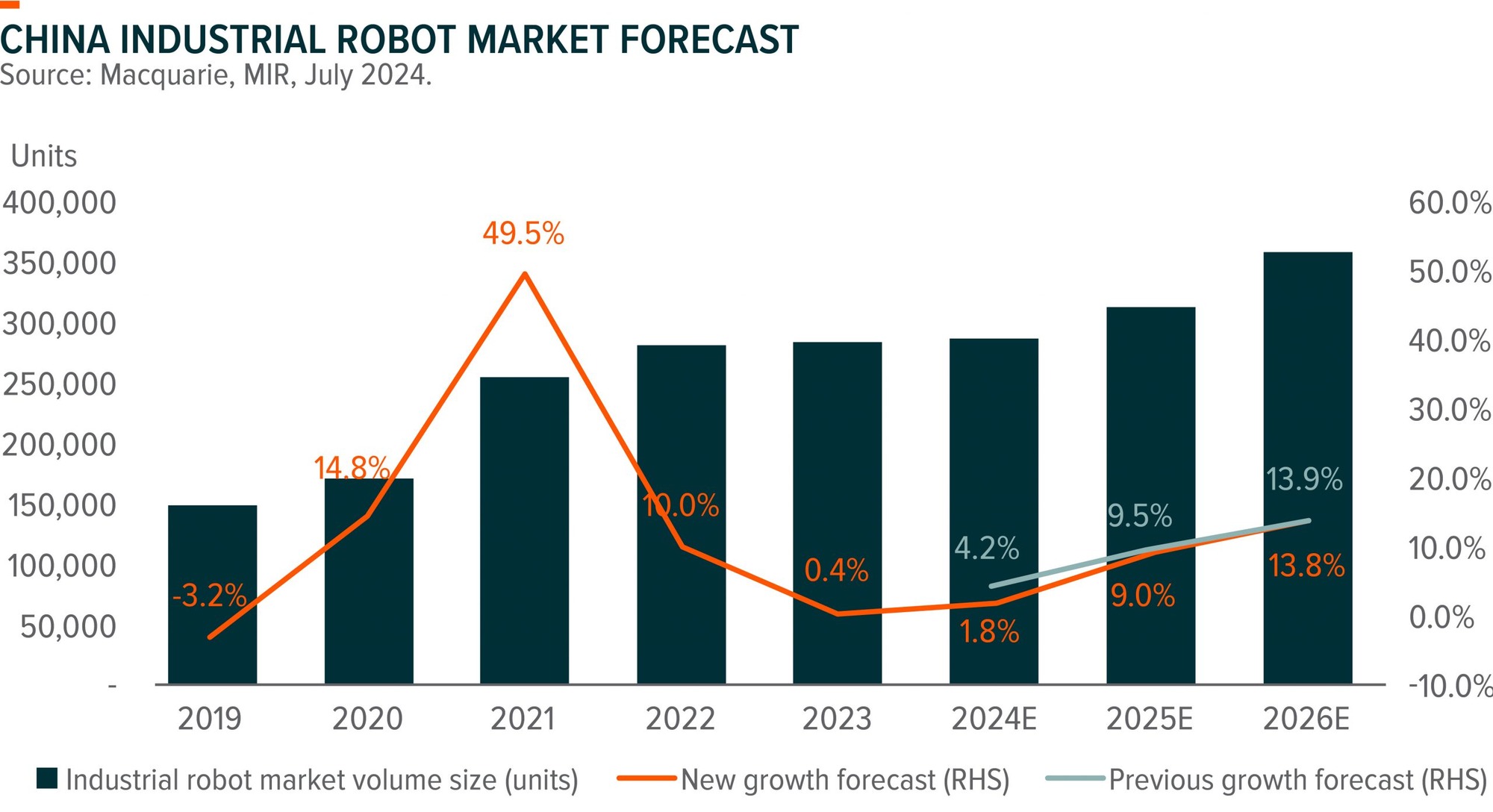

Industrial robot sales volume grew 5.4%yoy in 2Q24 vs 4.8%yoy in 1Q24. Robot demand from home appliance, 3C, autos, metals, semiconductor, chemicals and F&B grew significantly in 1H24 which offset the decline from lithium battery and PV robotics. MIR, a market intelligence agency, estimates industrial robot demand remains soft in 2H24 with the whole year demand growing by 1.8%yoy. Yet, they also expect some upside from the downstream if seeing any signs of China macro recovery. For example, some factories in mining and manufacturing sectors who actually have strong cash flow and material upgrading/replacement demand for automation, have delayed the order place and been waiting for clear policy stance due to lack of confidence in China economy. Thus, we remain constructive on the long-term demand.

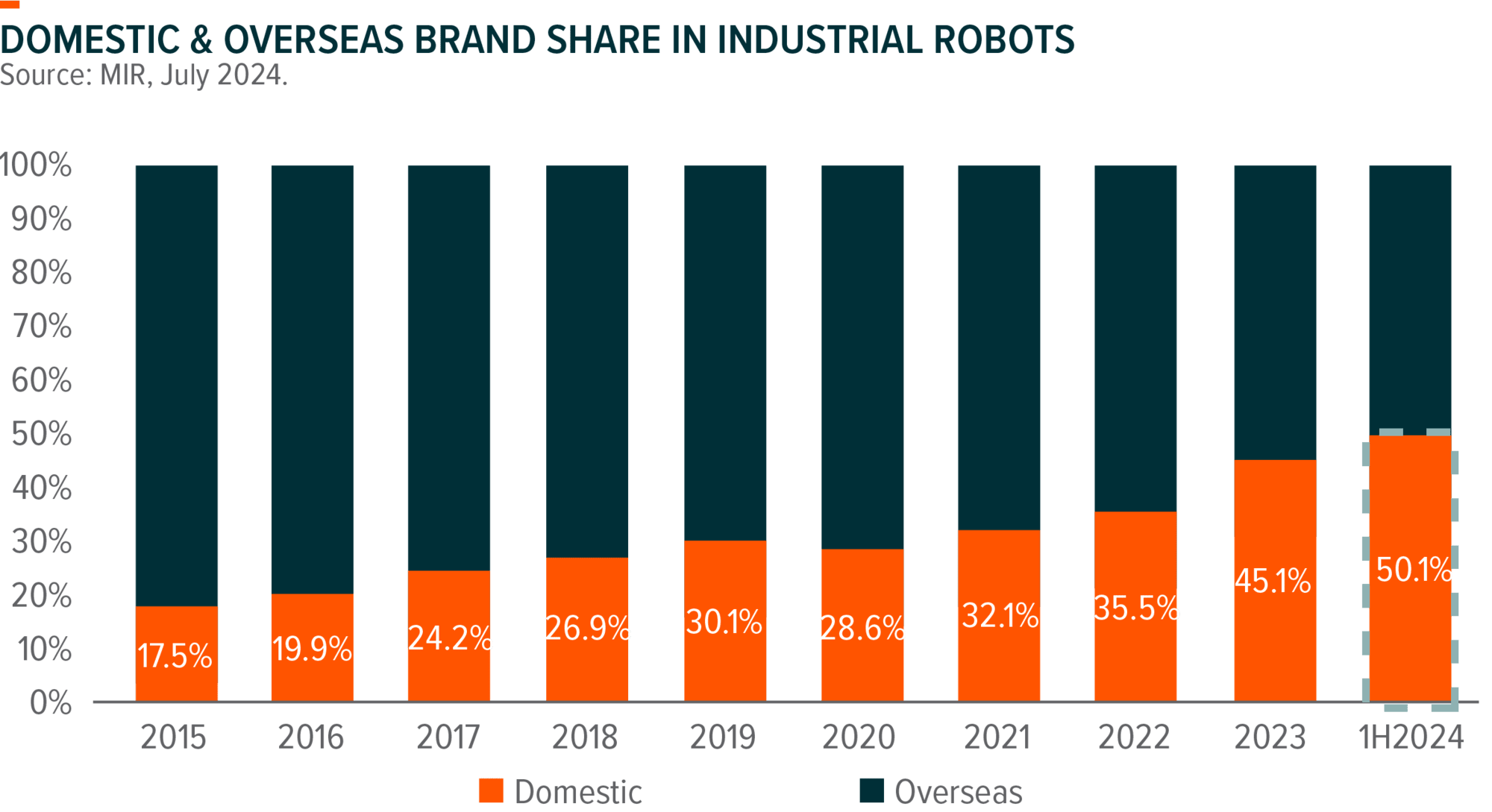

FANUC, Estun, Inovance and KUKA remained the top-four suppliers in China. Domestic manufacturers continue gaining market share on the back of customized products across emerging industries, fast delivery and advanced post-sale services. Our channel checks show that major players from Europe, the United States and Taiwan are significantly losing market share in China, while Japanese players’ sales remain solid due to high-end technology moat. Some domestic brands are cutting ASPs by 10-15% to their key customers, while for overseas brand, destocking in wholesalers’ end is close to the end. Consequently, we may see pricing bottom by the year end.

Stock Comments

- Suzhou TFC Optical Communication supplies key components in optical transceiver and is currently in the Nvidia supply chain. Company is traded as one of the Nvidia’s domestic play.

- Montage Technology is a leading player in DDR5 interface chips. Montage is the proxy for DDR5 chips in Greater China, and now leads the interface for DDR5 Gen 3. Inventory digestion completed and the traditional server market is expected to grow in 2024.

- Shenzhen Inovance Technology posted 1H24 preliminary results with bottom line in a range of -5%~5%yoy, which is a miss versus consensus. Additionally, China automation demand remains sluggish mainly dragged by weak demand from renewables. We may expect a little better traditional automation demand recovery in the second half to the year.

Preview

We didn’t change the view that China industrial automation market remained at the bottom before seeing any signals of out. The current stimulus policies on large-scale equipment replacement are definitely very positive for automation demand. However, it takes time to see the funding really flow into the industries and people have more confidence in China economy recovery or policymakers’ stance on economy growth. We remain constructive on the industrial robot demand growth in the long term, but cautious on the short term. Additionally, demand across different automation segments are a little diverged, driven by different downstream applications. Some domestic players with broad customized product offerings and cost competitiveness have proven the capabilities to gain market share in the down cycle, who we will attach more attention to.

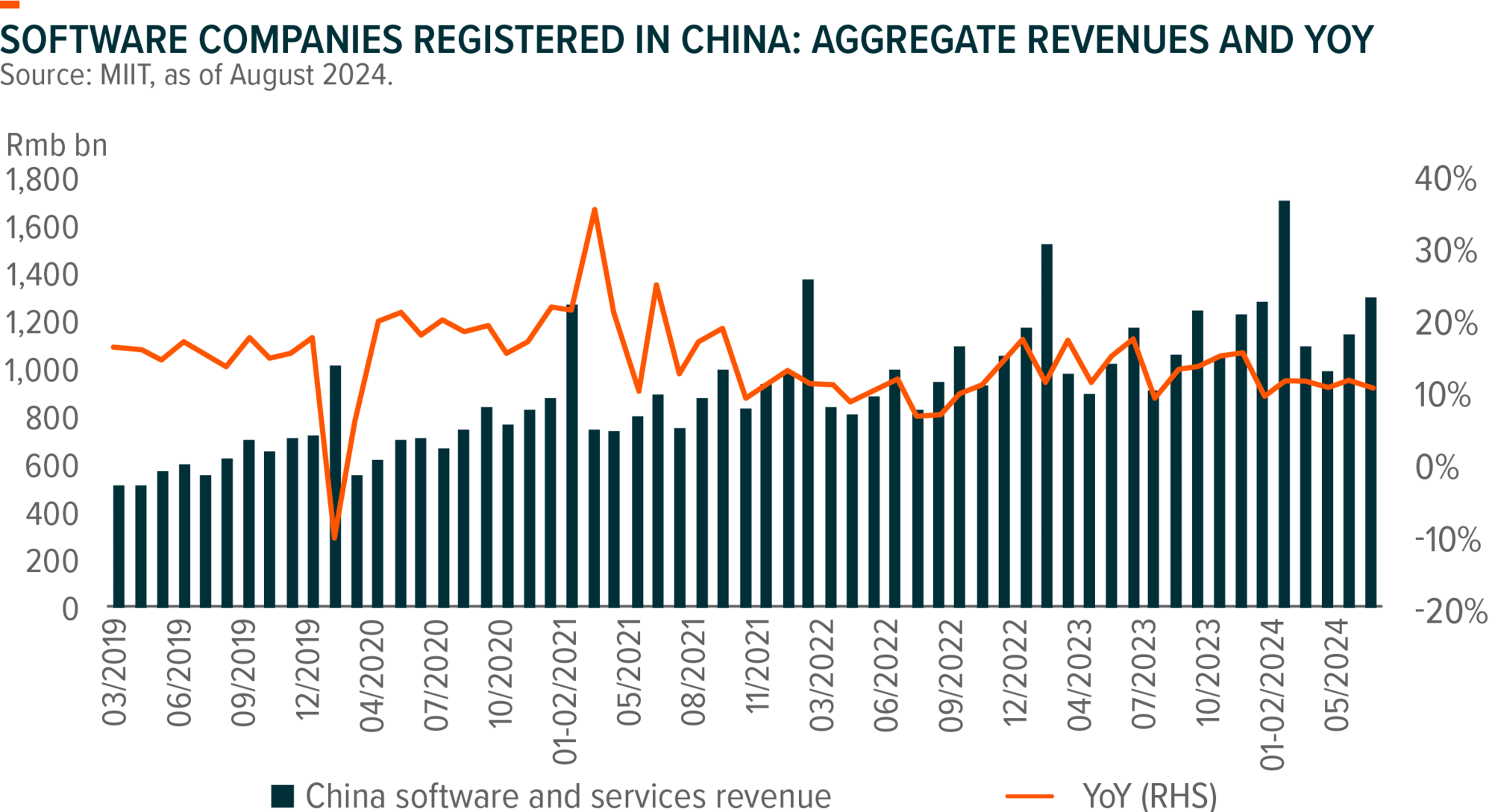

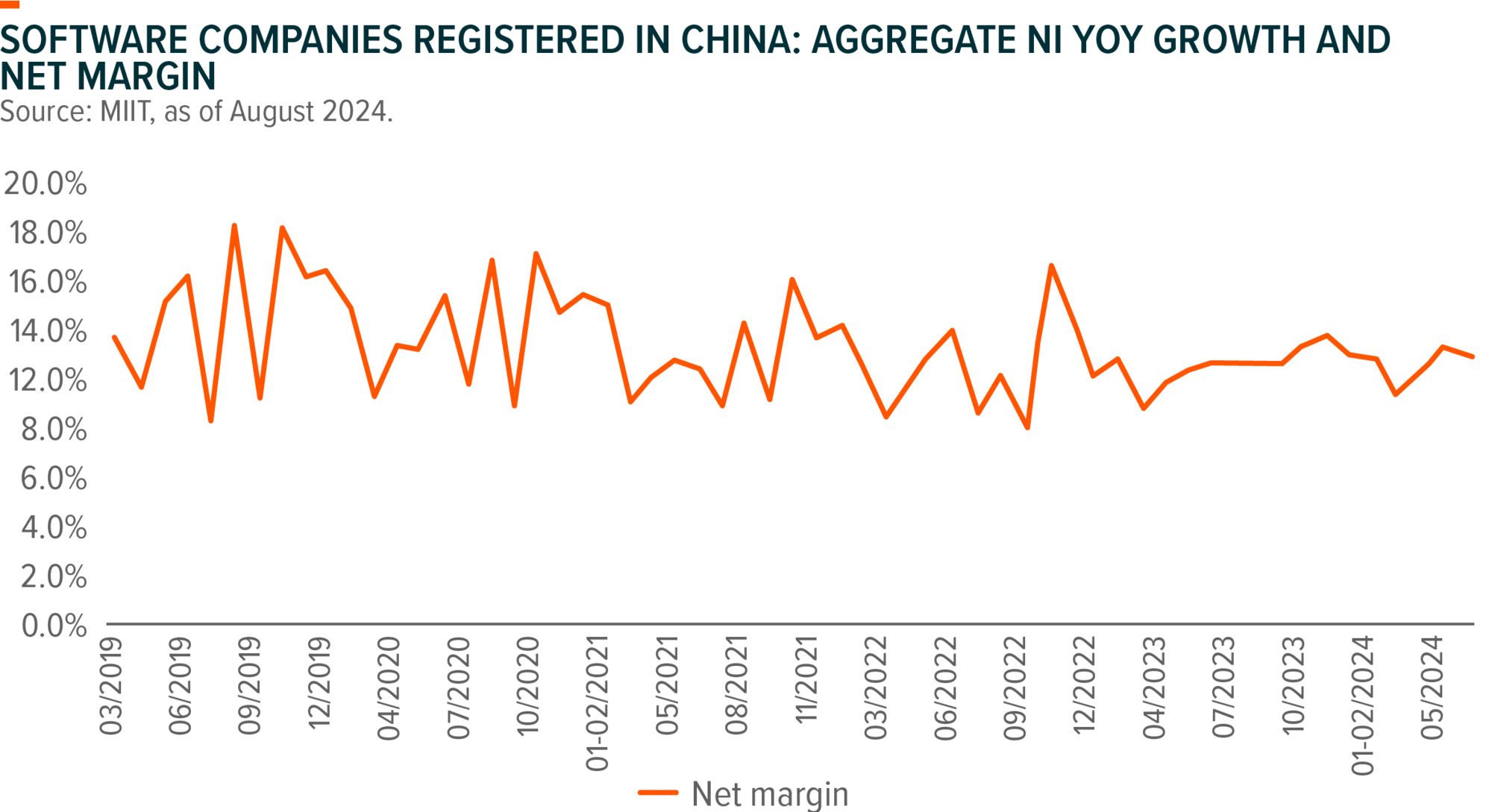

Global X China Cloud Computing ETF (2826 HK)

Industry Update

China national online retail GMV grew 13% in May, largely driven by front-loaded sales due to an earlier start of the 618 Shopping Festival and cancellation of the pre-sales period this year. For the 618 Shopping Festival that concluded on June 20th, Leading platforms no longer report headline GMV growth but market expect mid-to-high single digit industry GMV growth, and a flattish to teens sales growth for individual traditional and livestreaming e-commerce platforms. Return rated edged up for categories including apparel as consumers become more price sensitive and cautious in terms of their purchasing behaviors. Competition remained intense with leading platforms offering traffic support and promotions to attract merchants (especially small to medium-sized merchants) and consumers.

Domestic demands for sportswear, baijiu, beer and restaurant were weaker than expected into the month of June. Macau’s gross gaming revenue (GGR) came in at MOP17.7bn in June at 74% of the pre-COVID19 level vs. 79%/78% in Apr/May, likely due to weaker seasonality.

Stock Comments

- Alibaba share price performance was solid driven by multiple factors: 1) Taobao-Tmall Group announced several merchant policy adjustments. Tmall waived annual fees for merchants and Taobao started to charge 0.6% software services fee, which is likely to result in a net positive impact to take rate and profitability, 2) market expect growth gap between GMV and CMR to further narrow for the upcoming quarters, and 3) potential inclusion to the Stock Connect as early as September 2024.

- Glodon Company share price moved up as it seems like previous correction was overdone and most of the negative headlines are already priced in. Overall demands from end-customers remained weak which will weight on revenue growth in the near-term, but the company continues to improve margin on better cost controls.

- iflytek posted 1H24 preliminary results with both sales and bottom line missing consensus. Worsened profitability in 1H24 was mainly due to LLM investments, increasing bad debt provisions and less other income. Spark LLM v4.0 was launched end June-24, with eight areas said to beat GPT-4 Turbo, according to the management.

- Kingdee International Software, market became increasingly concerned on 1H24 revenue and earnings heading into the results. ARR is likely to be under pressure as subscription among Medium enterprise and SME growth is weaker compared to previous quarters.

Preview

Most of the software companies reported earnings miss for 1H24 due to delayed IT spending by enterprises amid macro weakness. In particular, SMEs and private enterprises are seeing continuous IT spending decline whereas government and SOEs’ IT spending also slightly disappointed. Software companies have seen increasing account receivable days which negatively impacted working capital. Into 2H24, we see better seasonality of software business but the pace of recovery will be more or less gradual. On margin, software company’s cost control measures will gradually take effect on profitability.

Global X China Little Giant ETF (2815 HK)

Industry Update

- A-shares had a roller-coaster ride in July expecting policy more policy support ahead of third plenum and retreated afterwards, with CSI300/500/1000 recording -0.6%/-1.1%/-0.1%. A-share turnover eased to an average of cRmb0.66trn in July from cRmb0. 72trn in June. The much awaited Third Plenum concluded on July 18th while investors’ expectations moderated into the session. The area with the highest expectations for reform is regarding consumption tax and this indeed got mentioned with no expansion of currently taxed categories. Yet, market was still disappointed that no bazooka-like strong policy support were hinted from Third Plenum or from announced from Politburo meeting. Policy actions had some sector specific impact but failed to boost overall sentiment: a re-iteration of an around 5% GDP growth for 2024, the PBoC cut rates (10bps for 7-day repo rate/1Y LPR/5Y LPR and 20bps for MLF); NDRC’s 300bn yuan ultra-long CGB funding for equipment upgrades and consumer goods trade-ins; and SASAC’s 3trn yuan equipment renewal plan for central SOEs over the next five years. Rising odds of a possible Trump presidency have raised concerns for exporters in specific and market sentiment in general. Among the 11 Wind A-share Level-1 sector indices, Financials (+5%), Real Estate (+4%), and Utilities (+1%) ranked as the top-three performers, while Energy (-7%), Materials (-2%) and Staples (-2%) were the bottom three.

- China’s 2Q GDP growth moderated to 4.7% YoY, or 1.0% QoQ in 2Q. The June activity data continues to send mixed signals. IP came in above expectations, growing 5.3% YoY. Retail sales slowed to 2.0% YoY in June. FAI was in line with expectations, up 3.9% YoY in Ytd. The details show ongoing weakness in real estate investment with some support in manufacturing investment and a moderate easing in infrastructure investment growth. Exports continued the solid growth trend, with a modestly higher-than-expected growth rate at 8.6% YoY.

- Entering into earnings season, consensus estimates for CSI300/500/1000’s 2024 EPS growth have not seen too much revision yet. Of the 1,717 A-shares having announced 1H profit alerts, c47% were positive, with transportation infrastructure, IPP, electric utilities, auto components, healthcare equipment/supplies, telecom, electronics and semiconductors as outperformers.

- Technology sector relatively outperformed as better supporting technology innovation and supply chain safety was a key highlight of Third Plenum while rates cut expectation also boosted sentiment on healthcare, while we started to see those previous safe haven dividend names started to pull back, including Telco, Utilities, Financials and Oil.