Important Information

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X MSCI China ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer specific factors.

- The Fund has a portfolio investing in companies whose operations are primarily in the PRC and therefore is subject to emerging market risks such as risks associated with uncertainty concerning PRC laws and regulations and government policies. Generally, investment in emerging markets such as the PRC are subject to greater risks than developed markets due to greater political, economic and taxation uncertainty and risks linked to volatility, market liquidity, foreign exchange, legal and regulatory risks.

- The Fund is subject to concentration risk as a result of tracking the performance of a single geographical region i.e. the PRC. The value of the Fund may be more volatile than that of a fund having a more diverse portfolio of investments.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- Global X Hang Seng TECH ETF (the “Fund”) seeks to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Hang Seng TECH Index (the “Index”).

- The Fund’s investments are concentrated in companies with a technology theme. Technology companies are often characterised by relatively higher volatility in price performance. Companies in the technology sector also face intense competition, and there may also be substantial government intervention, which may have an adverse effect on profit margins. These companies are also subject to the risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences.

- The Fund’s investments are concentrated in securities listed on the Stock Exchange of Hong Kong (the “SEHK”) of companies that are active in technology sector may result in greater volatility in the value of the Fund than more diverse portfolios which comprise broad-based global investments. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the technology sector.

- The Index is subject to concentration risk as a result of tracking the performance of securities incorporated in, or with majority of revenue derived from, or with a principal place of business in, the Greater China region. The Fund’s NAV is therefore likely to be more volatile than a broad-based fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

- The trading price of the Fund unit (the “Unit”) on the SEHK is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- Dividends may be paid from capital or effectively out of capital of the Fund, which may amount to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment and result in an immediate reduction in the Net Asset Value per Unit of the Fund.

China Internet – Interoperability is Coming Closer

On 5 September, Taobao issued a proposal to include WeChat Pay as an additional payment channel, and indicated that WeChat Pay will gradually open to all Taobao & Tmall merchants starting 12 September. The announcement comes after the completion of Alibaba’s three-year Antitrust rectification work, and is preceded by several rounds of small scale testing as reported over the past 2 years. This could mark the further opening of China internet ecosystems as the results of industry dynamics changes and regulatory push.

Implications

The new partnership could be a win-win deal for both Alibaba and Tencent, though direct impact is likely to be marginal at current stage. For Alibaba, the inclusion of WeChat Pay offers optionality for Taobao & Tmall to tap into new users, especially in lower tier cities, which also sustains its effort to drive GMV growth under current competitive market. This also aligns with its strategy to enhance user experience through offering more flexible payment options. For Tencent, the collaboration could support the transaction volume for WeChat Pay, potentially mitigating the headwinds on its Fintech revenue amid soft consumer sentiments.

Potential further partnerships between both parties should have more significant impact. Taobao and Weixin have been collaborating on advertising over the past few quarters, and the direct access to Taobao through Weixin ads brings incremental high quality user traffic to the eCommerce platform, especially during key shopping festival such as D11 last year. The new partnership in payment might pave way for further opening of ecosystem to each other, with possibility for Taobao & Tmall to open mini-program in Weixin. This could help Alibaba tap into over 1bn users in Weixin, among which c.247mn users do not have Taobao APP installed in China (Goldman Sachs, Questmobile). For Tencent, this could lead to higher payment and advertising revenue from Taobao merchants.

Industry-wide, we believe the collaboration marks a milestone for the interoperability among China internet ecosystems. Historically, major internet companies have been building walled garden to keep traffic, user, and data in a closed ecosystem, starting from 2008 when Taobao prohibited Baidu from indexing its content. This approach gave rise to a number of ‘Super Apps’ with comprehensive functions and hundreds of millions of users in China, but at the expense of user experience and a fair competition environment, which led to user complaints and regulatory attention. In September 2021, MIIT hosted a meeting with major communication services apps providers and required opening up direct access to external links within platforms, calling for a more open China Internet. In addition to regulations, the peaking of internet users in China also urge companies to seek for incremental traffic, arguably from other ecosystems, thus accelerating interoperability among Chinese internet ecosystems. Ultimately, we believe a more open internet and more benign environment should be beneficiary for major internet platforms in a slower growth market.

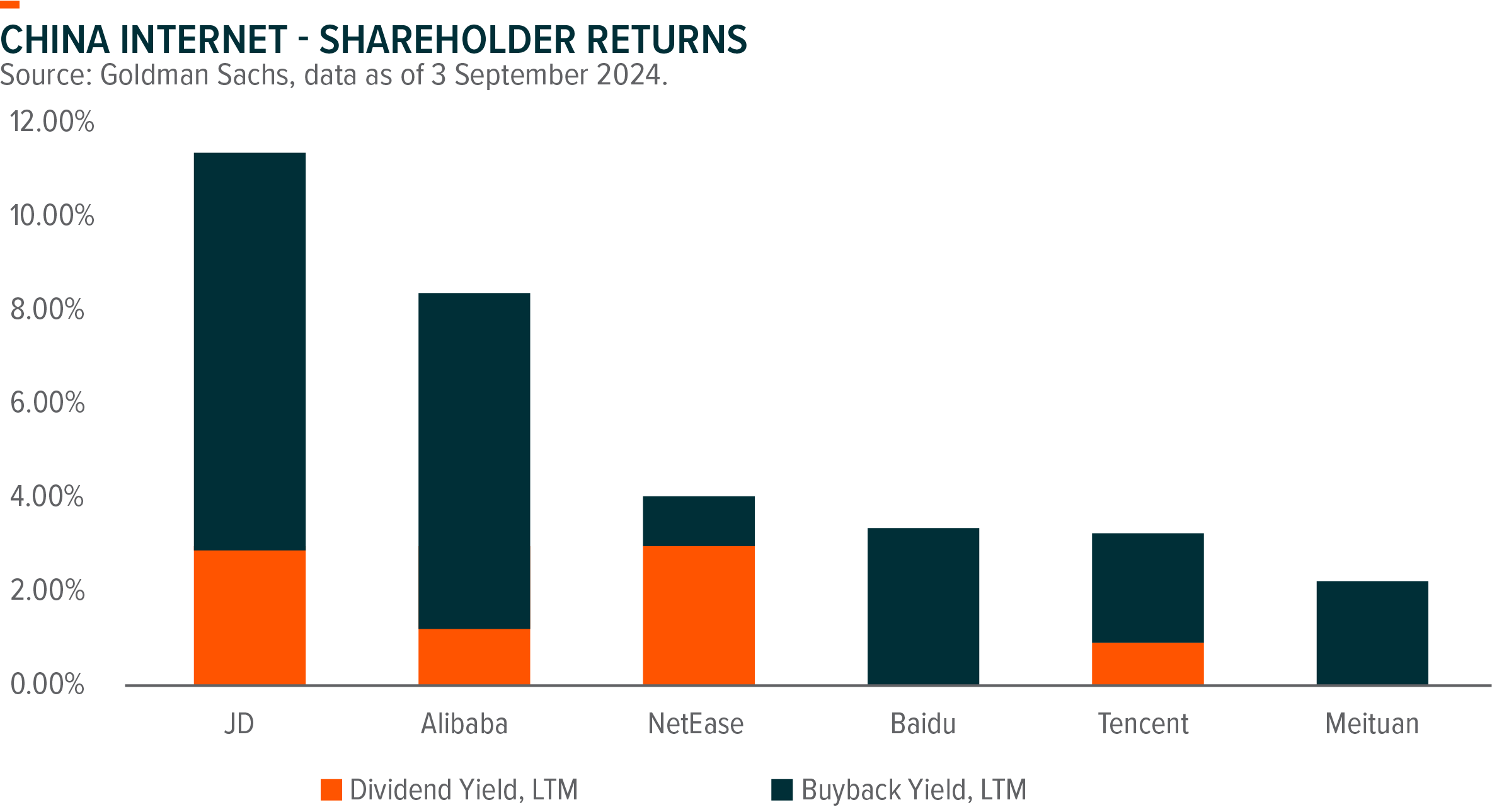

Though soft macro and slowing traffic continue to weigh on revenue growth, rapid ramp up in shareholder returns, expanding margin, and undemanding valuation define the unique positioning of Chinese internet stocks. Tencent, Alibaba, and other major internet platforms are key holdings in Global X MSCI China ETF (3040 HK) and Global X Hang Seng TECH ETF (2837 HK).

Related Global X ETFs’ Product1

| Global X MSCI China ETF (3040 HK) | Global X Hang Seng TECH ETF (2837 HK) | ||

|---|---|---|---|

| Inception Date | 17 June 2013 | 30 March 2023 | |

| Reference Index | MSCI China Index2 | Hang Seng TECH Index2 | |

| Primary Exchange | Hong Kong Stock Exchange | Hong Kong Stock Exchange | |

| Ongoing Charges Over A Year | 0.18% p.a. | 0.44% p.a. | |

| Product Page | Link | Link |

Ongoing Charges Over A Year: The Fund adopts a single management fee structure, whereby a single flat fee will be paid out of the assets of the Fund to cover all of the costs, fees and expenses of the Fund. The ongoing charges figure is an annualised figure based on the ongoing expenses of the Fund, expressed as a percentage of the Fund’s average Net Asset Value of the Listed Class of Units of the Fund over the same period. This figure may vary from year to year. The Fund adopts a single management fee structure, whereby a single flat fee will be paid out of the assets of the Fund to cover all of the costs, fees and expenses of the Fund. The ongoing charges of the Fund is equal to the current rate of the management fee of the Listed Class of Units of the Fund. For the avoidance of doubt, any ongoing expenses of the Fund exceeding the ongoing charges of the Fund (i.e. the management fee) shall be borne by the Manager and shall not be charged to the Fund. Please refer to the Key Facts Statement and the Prospectus for further details.