Wind Turbines Ride the Wave of Chinese Renewable Energy

In recent years, there has been a global shift towards an eco-friendly lifestyle. Wind energy has been gaining popularity and competitiveness.

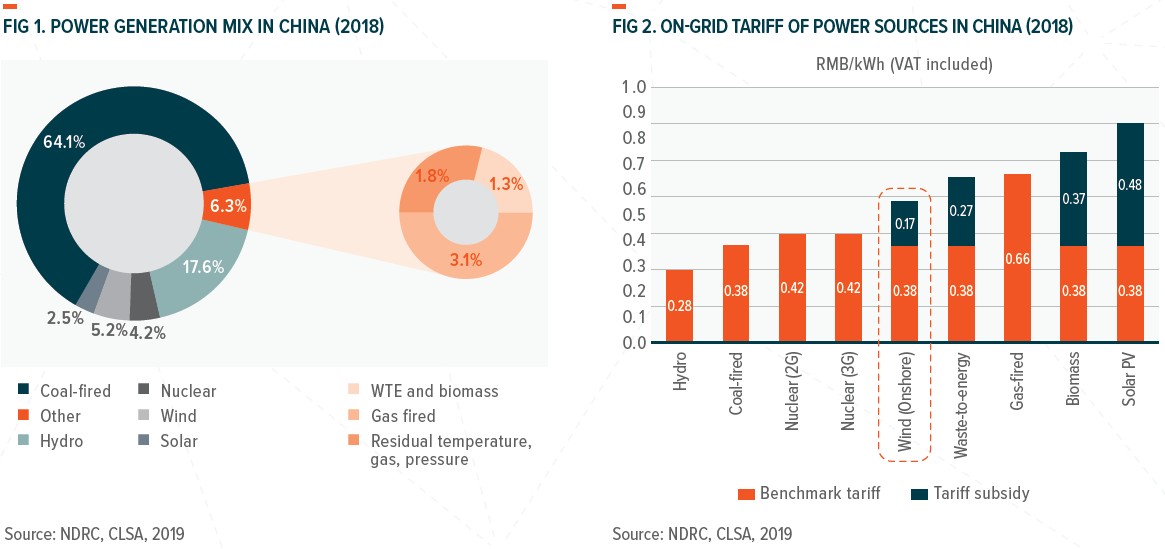

At the end of 2018, China’s total power capacity reached 1,900 gigawatts (GW), including thermal power of 1,147GW (60.4%), hydropower of 350GW (18.4%), wind power of 184GW (9.7%), solar power of 175GW (9.2%), and nuclear power of 45GW (2.3%). Total electricity generation in 2018 was 6,990bn Kilowatt (kWh), of which non-fossil fuel generation accounted for 30.9%, contributed mainly by hydropower, wind, nuclear, and solar at 17.9%, 5.2%, 4.2%, and 2.5%, respectively.

China’s Clout in the Global Wind Power Landscape

China, one of the world leaders in wind power generation, has the largest installed capacity out of any nations coupled with continued rapid growth in new wind facilities. Benefiting by its large landmass and long coastline, China has abundant wind power resources. It is estimated that the country has about 2,500GW of exploitable capacity on land and 200GW at sea. China is expected to produce 250GW of wind capacity by 2020 as part of the government’s pledge to manufacture 15 percent of all electricity from renewable resources by year-end. The Chinese government has planned a wind power road map leading up to the year 2050. The production capacity of wind power aims to reach 400GW by 2030 and 1,000GW by 2050, respectively.

In China, the Northern region has a vast potential for wind capacity, while offshore wind energy in the Southeast is abundant. Inner Mongolia, situated in Northern China, processes a vast potential for wind power development with an estimated capacity of 1,300GW as well as makes a significant contribution to wind power in China.

The China National Energy Administration initially set a goal for installing of 5GW offshore wind capacity by 2015 as well as 30GW by 2020. However, the plan was executed slower than expected, resulting from the rise of domestic turbine manufacturers with limited experience. Offshore projects are around 2-3 times more expensive than onshore, but they could generate more power due to sufficient wind resources and high-quality turbines. Many industry analysts believe the costs of offshore wind power can come down significantly over the next few years, becoming comparable with solar and onshore wind facilities. Many local authorities in China have been expanding the installation capacity of offshore wind power in recent years, as part of the country’s efforts to tackle pollution and further increase the portion of clean energy in the country’s energy mix. The key offshore wind regions in China are Jiangsu and Guangdong province, where Jiangsu is expected to deliver 10GW offshore wind power by 2020, known as ‘Three Gorges on Sea,’ while Guangdong is forecasted to produce 12GW offshore wind capacity by the end of 2020.

Government-led Disruptions

The Chinese government has committed to reducing the portion of fossil fuel consumption. It aims to increase the generation of non-fossil fuel to 50% by 2030, which is under “The revolution strategy of energy production and consumption (2016-2030)” that was announced in December 2016. We expect China to continue to cut new thermal power capacity during 2021-30, and add more wind and solar capacity, which is more economical and flexible, also less controversial than developing hydropower and nuclear power.

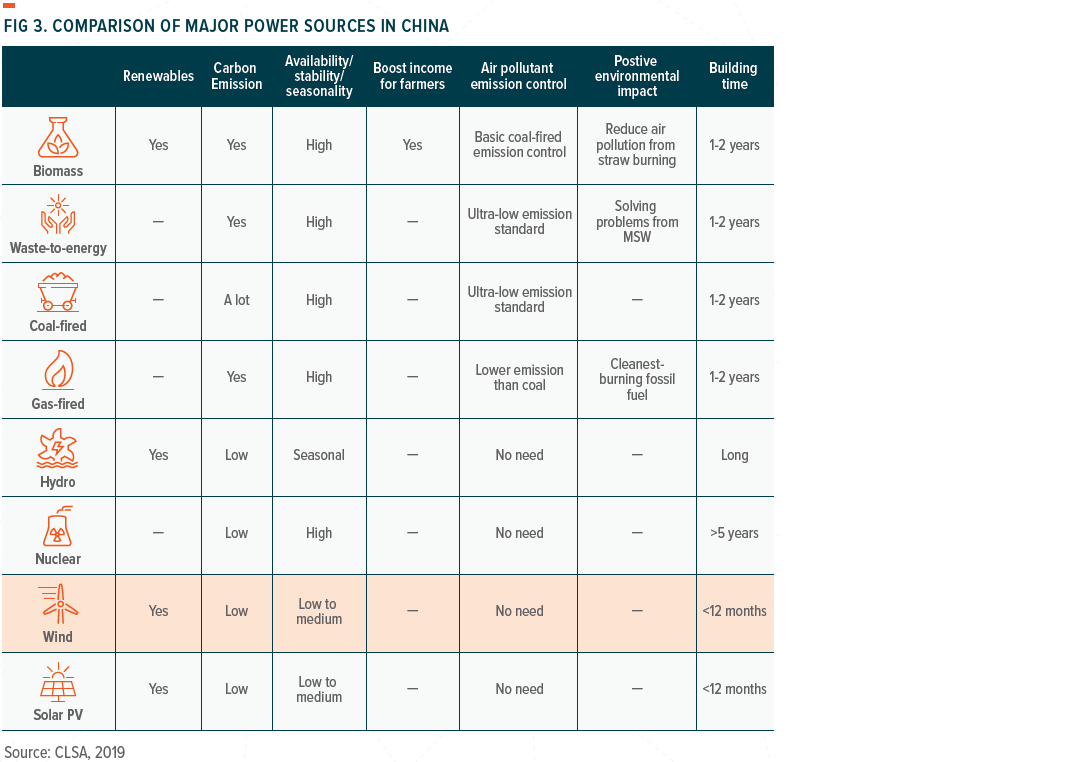

The Chinese government initiated the four-tier Feed-in-Tariff (FiT) mechanism for onshore wind in 2009, and the setting of the tariff tier is mainly based on wind resources. The general principle is that the better the wind resource, the lower the FiT. The difference between the FiT and the local coal-fired benchmark tariff is called the renewable energy subsidy. It is compensated by the renewable energy fund under administration by the Ministry of Finance.

Three-North Regions

Three-North Regions, the provinces in Northern and Western China, have abundant wind resources and plenty of land supplies. The renewable energy subsidy is higher in those regions, considering a lower coal power benchmark tariff and slower power demand growth.

The regions with a shortage of wind resources are those provinces in central, coastal, and Southern China, where have relatively lower wind speed and high land scarcity. Local economic development and power demand are better in those provinces. Lower renewable energy subsidies are given relative to the higher the coal benchmark tariff.

As a result of a mismatch between grid infrastructure construction and wind farm installation, there has been a serious wind curtailment issue in a few Three-North Region provinces. Much of the newly installed wind turbines either could not be connected to the grid or were unable to be used in full capacity. The issue gradually emerged towards the end of 2010, and as a result, the number of China’s new wind connections fell in 2012, mainly in the Three-North Regions. To take advantage of business opportunities in the wind equipment industry, the majority of small wind turbine manufacturers competed aggressively on price in 2010 and reduced wind turbine tender prices.

Recent Hurdles

A proposal for onshore wind tariff adjustments was announced in October 2014 by the National Development Reform Commission (NDRC) with the final tariff, adjustment officially announced in December 2014.

From 2016, wind operators shifted more of their investment focus to regions with low wind speed facilitated by fast-developing wind turbine technology appropriate for regions with lower wind speed and high altitude. As a result of the severe wind curtailment issue, the National Energy Administration (NEA) banned development in six provinces within the Three North Regions. The ban led to new capacity in the Three-North Regions to fall sharply in 2016 as a result of over-investment in 2015 and the halt of new capacity in 2017.

However, preferential policies, including the expansion and improvement of the transmission infrastructure, guaranteed minimum purchases, monitoring, and warning mechanisms, etc. offer an improvement in curtailment rates. The average wind curtailment rate in China dipped below 5% in 1Q19, which is considered a relatively healthy level.

For 2021-30, we expect Chinese power plant developers to force a shift in coal-fired power stations investment to renewables and accept a relatively lower return under grid parity. This is given the Chinese government aims to increase in non-fossil fuel generation aggressively to 50% in 2030, up from 30% in 2020.

Tailwinds for Wind Power in China

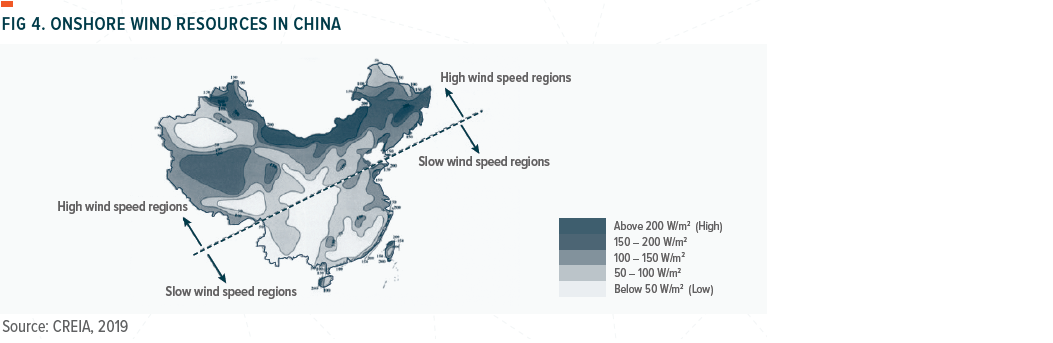

Wind power provides many benefits in terms of establishing energy independence. Emission from wind is negligible vs. coal or gas, while the time required to build is relatively faster than other forms of power generation at a timeframe of fewer than 12 months. While the cost of production ranks on the high side, among other forms of renewable energy, it is also coming down fairly quickly. Wind turbines installation began to boom in 2008, with the majority of new turbines installed being 1.5-2MW. Nowadays, new installations are likely to be 2-2.5MW, while offshore wind turbines have a capacity of 4-5MW.

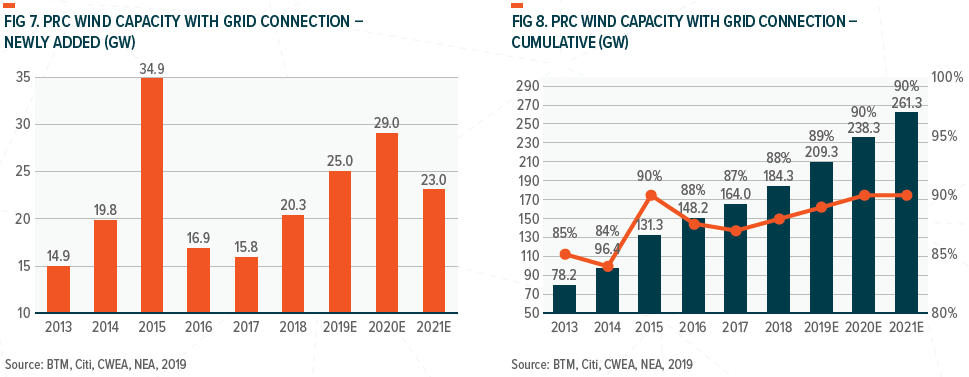

PRC wind farm installations with grid connections are expected to rise to 25GW in 2019E and 29GW in 2020E, from 20.3GW in 2018. Wind farms approved for construction before the end of 2018 have to be completed with a grid connection before 2020 year-end to be entitled to tariff subsidies. Those approved in 2019-20 have to be completed before 2021 year-end. So far, PRC wind power CAPEX was up 79.4% year on year to Rmb70.8bn in October 2019, while public bidding prices of 2.5-3.0MW and 3.0MW wind turbine generator units were up 13-17% in September 2019.

Click here to download the full report.

Related ETFs