Important Information

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including product features and the risk factors. Investment involves risks. Past performance is not indicative of future performance. There is no guarantee of the repayment of the principal. Investors should note:

- Global X Innovative Bluechip Top 10 ETF (the “Fund’s”) seeks to provide investment results that, before deduction of fees and expenses, closely correspond to the performance of the Mirae Asset Global Innovative Bluechip Top 10 Index (the “Index”).

- The Index is a new index. The Index has minimal operating history by which investors can evaluate its previous performance. There can be no assurance as to the performance of the Index. The Fund may be riskier than other exchange traded funds tracking more established indices with longer operating history. The Index is an equal weighted index whereby the Index constituents will have the same weighting at each rebalancing (but not between each rebalancing) regardless of its size or market capitalisation based on the methodology of the Index.

- The Fund’s investments are concentrated in companies with a technology theme. Many of the companies with a high business exposure to a technology theme have a relatively short operating history. Technology companies are often characterised by relatively higher volatility in price performance when compared to other economic sectors. Companies in the technology sector also face intense competition, and there may also be substantial government intervention, which may have an adverse effect on profit margins. Rapid changes could render obsolete the products and services offered by these companies. These companies are also subject to the risks of loss or impairment of intellectual property rights or licences, cyber security risks resulting in undesirable legal, financial, operational and reputational consequences.

- The Fund’s investments are concentrated in companies in the technology sector. The Fund’s value may be more volatile than that of a fund with a more diverse portfolio. The value of the Fund may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory event affecting the technology sector.

- The number of constituents of the Index is fixed at 10. The Fund by tracking the Index may have a more concentrated investment portfolio than it would have held if tracking an index with a higher number of constituents, leading to higher risks of volatility.

- Underlying investments of the Fund may be denominated in currencies other than the base currency of the Fund. In addition, the base currency of the Fund is USD but the trading currency of the Fund is in HKD. The Net Asset Value of the Fund and its performance may be affected unfavourably by fluctuations in the exchange rates between these currencies and the base currency and by changes in exchange rate controls.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from redemption requests.

- The trading price of the Units on the SEHK is driven by market factors such as the demand and supply of the Units. Therefore, the Units may trade at a substantial premium or discount to the Fund’s Net Asset Value.

- Payments of distributions out of capital or effectively out of capital amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction in the Net Asset Value per Unit of the Fund and will reduce the capital available for future investment.

Obesity Medication: A Duopoly Led by Novo and Lilly

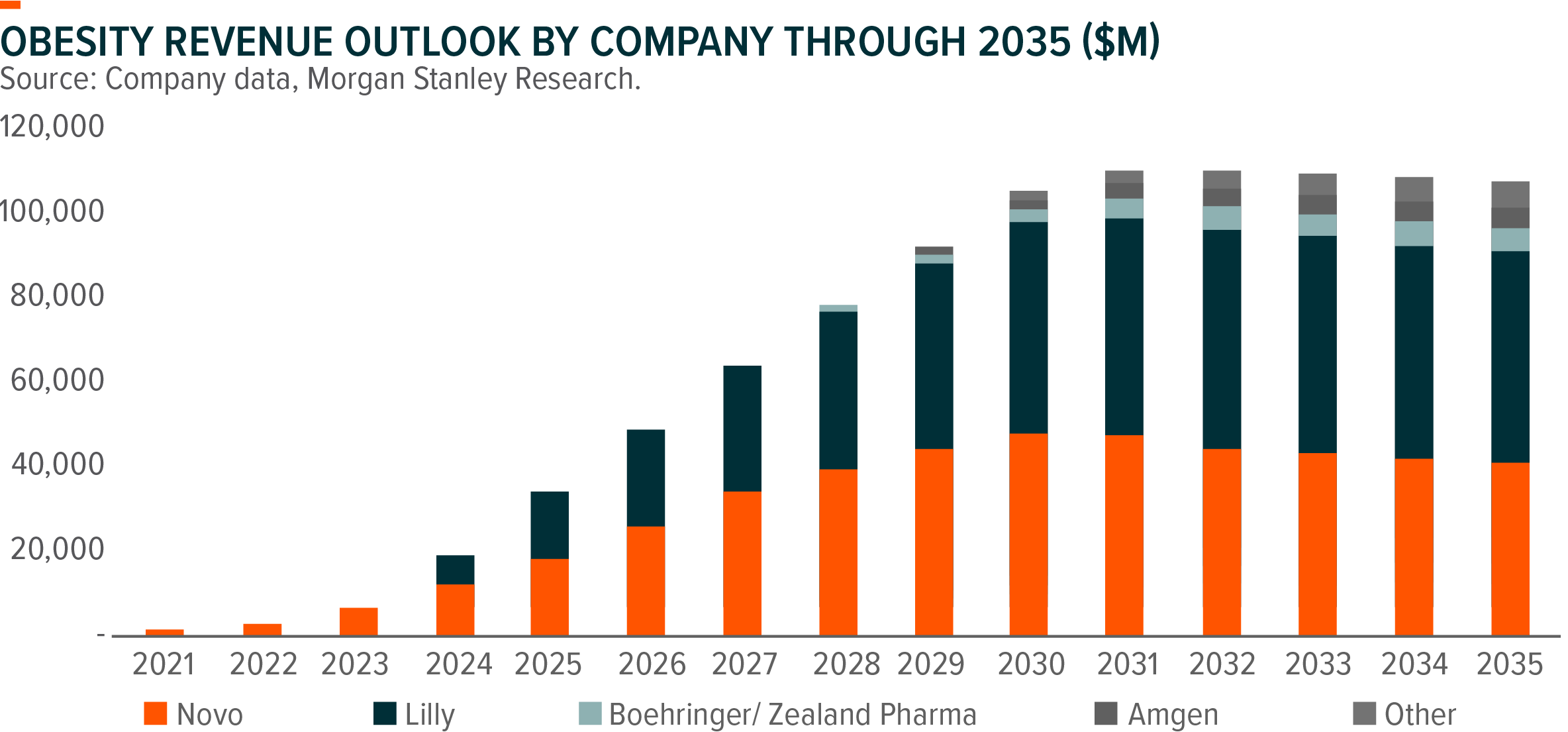

Currently, more than a billion people around the globe are affected by obesity, and 54% of adults will be overweight or obese by 2035. This rising global prevalence of obesity, coupled with the expanding use of obesity medications for related chronic diseases, presents substantial growth potential for the obesity market, which is anticipated to exceed $100bn by 2030. GLP-1 is the leading treatment in this space, with Novo Nordisk (NVO US) and Eli Lilly (LLY US) positioned as two major players. We believe these two companies will continue to dominate the market for the foreseeable future with 80%+ shares combined, primarily supported by their robust pipelines and significant capital expenditures.

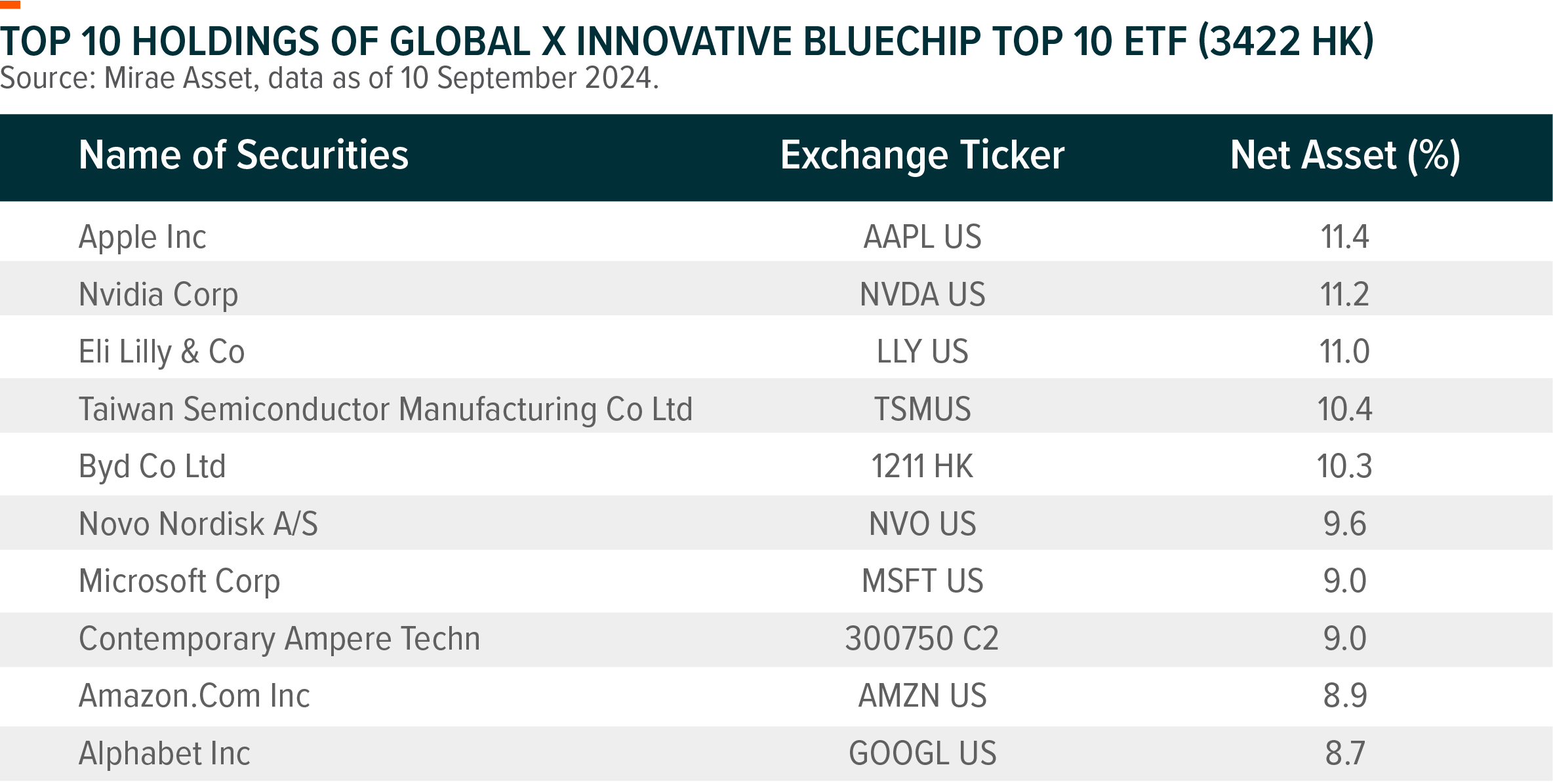

For investors looking to capitalize on opportunities within the obesity market, the Global X Innovative Bluechip Top 10 ETF (3422 HK) offers a strategic investment avenue, with Novo and Lilly making up approximately 20% of the fund’s holdings.

Rosy Outlook of Obesity Medication: $100bn+ Market by 2030

The global prevalence of obesity has more than doubled since 1990, according to WHO. Currently, over a billion people worldwide are living with obesity, and 54% of adults are expected to be overweight or obese by 2035, up from 38% in 2020 (World Obesity Atlas 2024). Obesity is a significant contributor to more than half of all diabetes cases and is linked to over 200 other chronic conditions. The increasing rates of obesity, combined with rising life expectancy, suggest a growing financial burden on healthcare systems. This underscores the importance of early screening and prevention strategies.

GLP-1 is becoming a major treatment option in this arena and have demonstrated high efficacy and safety. Initially approved for diabetes management, injectable GLP-1 medications have been shown to help individuals lose 15-25% of their body weight by reducing appetite.

Furthermore, recent findings indicate that obesity medications may not only address obesity itself but also prevent associated diseases. For instance, SELECT, Novo Nordisk’s landmark trial for its obesity medicine Wegovy, reported a 20% reduction in the risk of heart attacks, strokes, and cardiovascular-related deaths in non-diabetic patients with obesity and pre-existing cardiovascular conditions.

In 2023, sales of branded obesity drugs reached $6 billion. The global obesity market is expected to exceed $100 billion by 2030, driven by increasing adoption rates, extended treatment durations, and enhanced supply chains.

Competition Landscape: Two-player Story to Remain

Novo and Lilly are poised to maintain their dominant duopoly in the obesity market, holding a combined market share of over 80% for the foreseeable future. This strong position is supported by their robust pipelines, enormous supply chain investments, and compelling clinical data. Additionally, their significant marketing expenditures to reach target patient populations, along with their first-mover advantage, further reinforce their market dominance, all backed by multi-year, multi-billion dollar capital expenditures

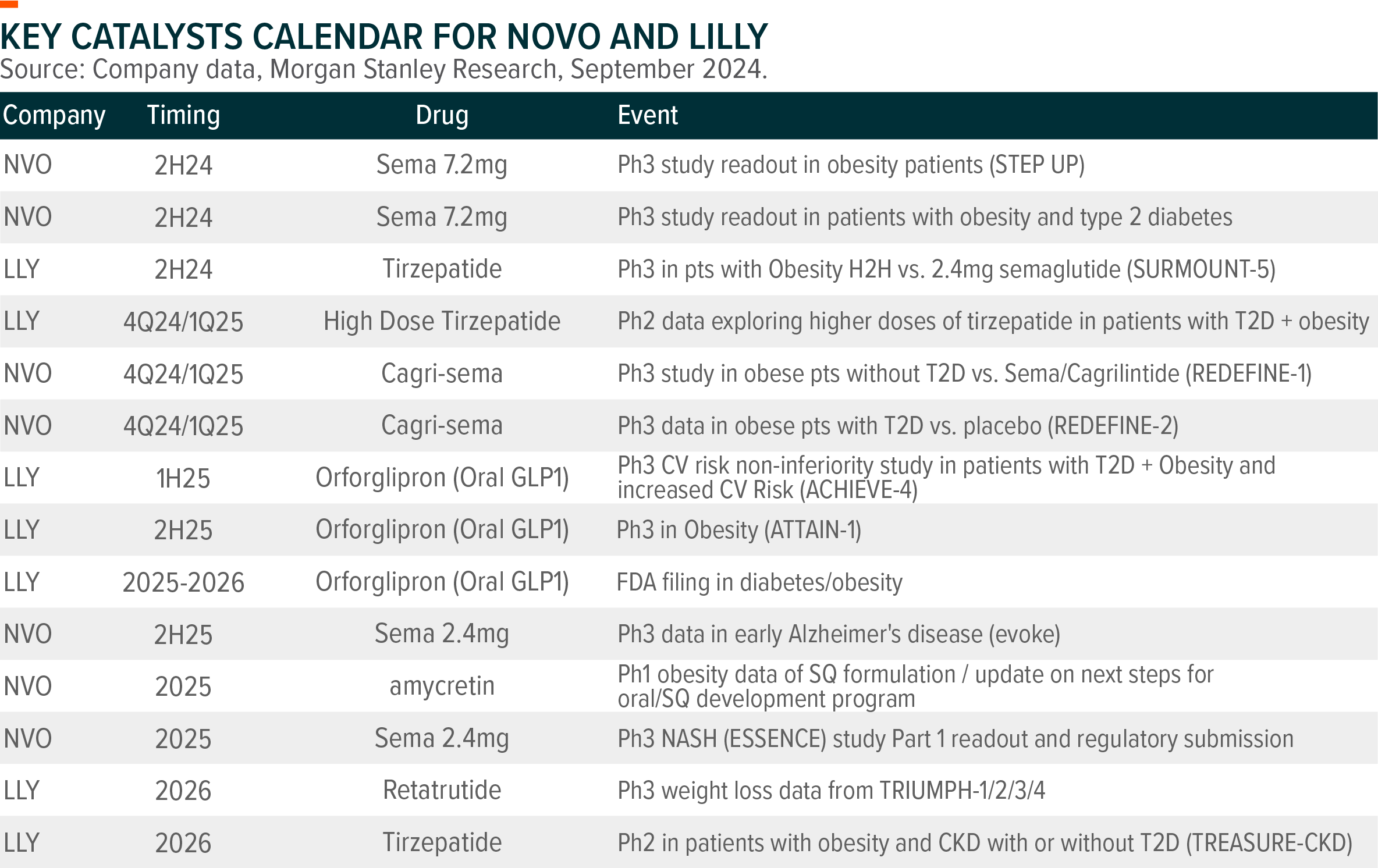

Novo and Lilly are expected to invest over $50 billion combined from 2022 to 2028 to bolster the supply chain supporting their GLP-1-based obesity franchises. While potential competition poses a challenge in the obesity market, the recent developments in their pipelines remain encouraging. In 2H24, there are several key diabesity pipeline readouts, including data from Novo’s Phase 3 REDEFINE 1 trial for its next-generation obesity asset, CagriSema, as well as results for high-dose Semaglutide.

Given the significant potential scale of the obesity market and the heightened interest from investors, there are compelling incentives for other companies to enter this lucrative market. Major players, including Roche, AstraZeneca, Pfizer, Novartis, Amgen, and Regeneron, have expressed interest in the obesity market and are developing related assets. For instance, Roche and AstraZeneca entered this space through acquisitions in 2023, while Amgen and Pfizer are advancing their diabesity pipeline drugs. However, it is crucial to note that these companies lag significantly behind Novo and Lilly in terms of innovation and infrastructure for obesity treatments. Novo and Lilly’s substantial head start, strong brand recognition, and positive clinic data may provide a protective buffer against competitive pressures. As a result, we expect the duopoly established by Novo and Lilly to continue thriving in the market.

Related Global X ETFs’ Product1

| Global X Innovative Bluechip Top 10 ETF (3422 HKD) |

|

|---|---|

| Listing Date | 24 Nov 2023 |

| Reference Index | Mirae Asset Global Innovative Bluechip Top 10 Index2 |

| Primary Exchange | Hong Kong Stock Exchange |

| Ongoing Charges Over A Year | 0.68% p.a. |

| Product Page | Link |

The Fund adopts a single management fee structure, whereby a single flat fee will be paid out of the assets of the Fund to cover all of the costs, fees and expenses of the Fund. As the Fund is newly set up, this figure is an estimate only and represents the sum of the estimated ongoing charges over a 12-month period, expressed as a percentage of the estimated average Net Asset Value of the Listed Class of Units of the Fund over the same period. It may be different upon actual operation of the Fund and may vary from year to year. As the Fund adopts a single management fee structure, the estimated ongoing charges of the Fund will be equal to the amount of the single management fee, which is capped at 0.68% of the average Net Asset Value of the Listed Class of Units of the Fund. Any ongoing expenses exceeding 0.68% of the average Net Asset Value of the Listed Class of Units of the Fund will be borne by the Manager and will not be charged to the Fund. Please refer to the Key Facts Statement and the Prospectus for further details.