How Serious Are The Threats From Climate Change?

- Climate change is reshaping the energy industry

- The green electricity market is expanding

- The transport industry is ‘decarbonizing’

- Conservation is vital to solving the climate puzzle

- Hydrogen and biofuels will play an important role

Climate change is a dominant issue among policymakers, scientists and investors. It is re-shaping the future of the energy industry through financing, regulation, technological innovation and investor activism, with a seismic shift in the global capital-allocation landscape.

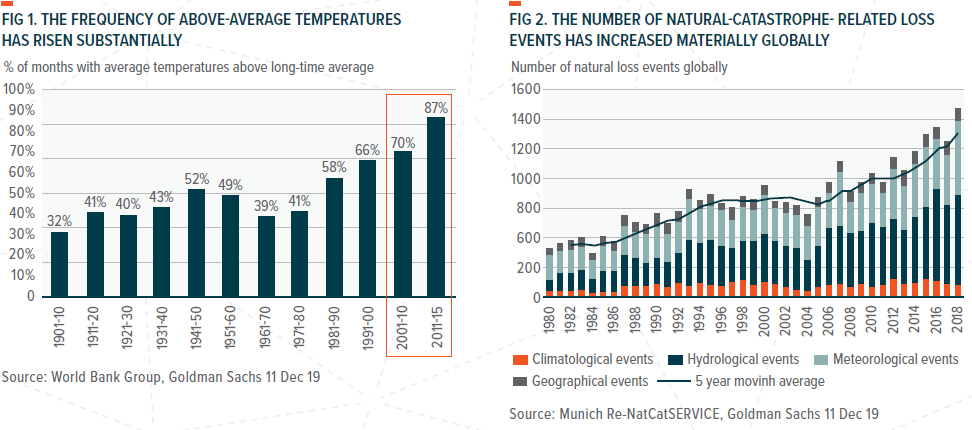

There has been a particular focus on the persistently high temperatures and the frequency of natural disasters across the globe, particularly in the past decade. While there is still debate on whether we can attribute an increase in the number and severity of natural catastrophes directly to climate change, there is a general acceptance that the frequency of at least some of these events, such as extreme heatwaves, flooding and wildfires, correlate with global warming.

Various academic studies on the effect of climate change have tried to quantify the impact it has on world economies. This research has utilized multiple approaches, with a recent report suggesting that changing temperatures could reduce global GDP by 3–7% over the longer-term (with most of these forecasts up to Year 2100).

Temperature Change and Sea Levels

Earlier research pointed toward variations of the impact of climate change on different countries, with developed economies seemingly less exposed to the effects of global warming, while emerging nations appeared more vulnerable. However, recent studies have found that this is no longer the case. The new analysis is based on current assessments of either temperature change or a rise in sea levels, which itself could be understating the effect our changing climate has on economies because estimates have risen over time. A recent United Nation climate report highlighted that escalations in global temperatures mean that extreme and rare oceanic events could become more commonplace by year 2100, with low lying cities and coastal areas particularly at risk.

A Rise in Incidents

Natural-loss-related events are typically classified into four categories:

- Geophysical: earthquakes, dry mass movements and volcanic eruptions

- Weather-related: flooding and storm surges

- Climatological: heatwaves, droughts and wildfires

- Meteorological: tropical storms and windstorms

Our research data suggests that the number of natural-loss incidents is rising by around 5%–6% per annum, compared with the ten-year historical average of 2%–4%. Weather-related events are an essential driver: in 2018, these accounted for approximately 90% of both the total number of natural hazards and the financial losses from such incidents. Moreover, weather-related damage has reached roughly USD $2.8 trillion in the past decade, which is more than 30% above the cumulative losses seen in the previous ten years.

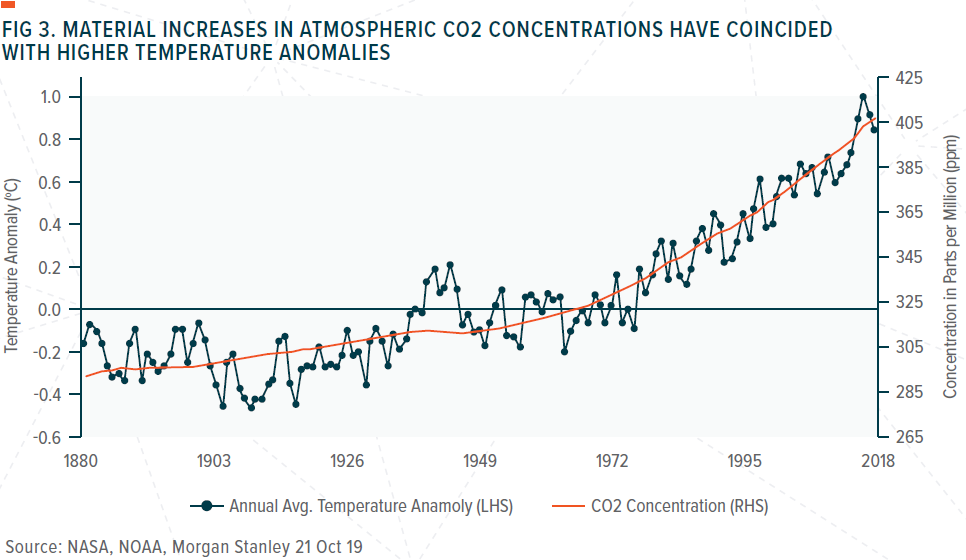

CO2 emissions are at their highest levels in human history, reaching 53.5 gigatons (Gt) in 2017. This increase is being driven by several man-made factors, broader industrialization and the burning of fossil fuels, which have resulted in steadily rising global temperatures. Based on average readings over the period 1951 to 1980, 18 out of the 19 warmest years on record have occurred since 2001, with 2018’s temperature 0.8°C (1.44° F) above average.

Paris Agreement Goals

An additional 1.5 billion people will inhabit the planet by 2040 – some 20% more than in 2018 – nearly a third higher than today. This will bring unparalleled disruption. Studies suggest we could see the mass migration of up to 200 million people globally over the first half of this century, an additional one billion people could be at risk of infectious diseases, and 20–30% of species may face extinction.

The Paris Agreement’s long-term temperature goal is to keep the increase in average global temperatures to within 2°C above pre-industrial levels; and pursue efforts to limit the rise to 1.5°C, recognizing that this would substantially reduce the risks and impact of climate change. Global greenhouse gas emissions need to be at or around net-zero by year 2050 to halt climate change and achieve the goals outlined in the Paris Agreement. This means we must move from 53.5 gigatone (Gt) of CO2 to zero by balancing the amount released into the atmosphere with that taken out. It is more realistic than a gross-zero target but still extremely ambitious. Clear opportunities to reduce emissions do exist, such as a rise in renewable power generation, the transition to electric vehicles, carbon capture and storage (carbon sequestration), hydrogen, and the development of biofuels.

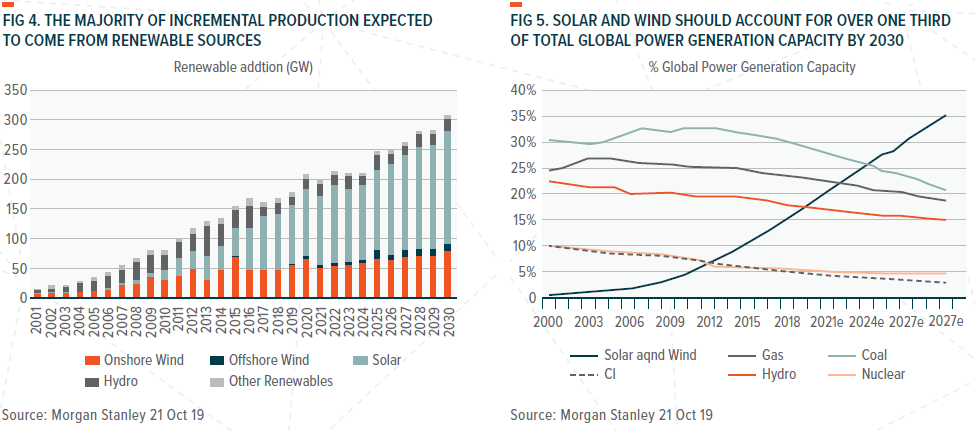

Power Generation

Morgan Stanley estimates that global power generation capacity will expand by 3,900 gigawatts (GW) between 2017 and 2030, with almost all of this expected to come from renewable sources. The carbon intensity of power generation should fall from 0.53 megatons (Mt) per terawatt hour (TWh) in 2017 to 0.35Mt per TWh in 2030. Total global carbon emissions from power production are expected to fall by nearly 3Gt over the next decade, with the mix shift enough to offset the growth in overall demand for electricity.

Zero-emission Transport

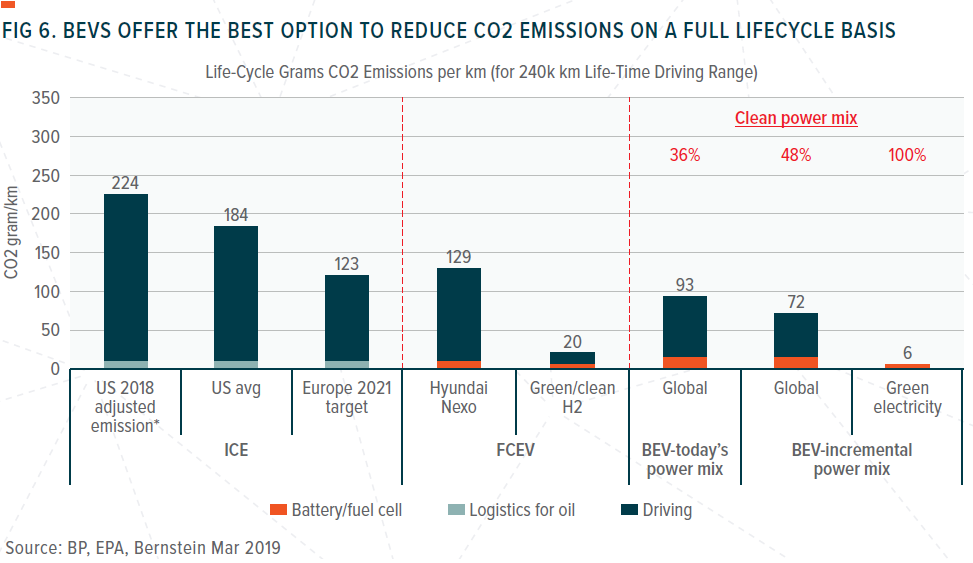

Decarbonizing transport, which is responsible for 24% of global CO2 emissions (29% in the US), is critical on the path to net-zero emissions. Furthermore, batteries and fuel-cells also play a crucial role in the decarbonization of power generation (responsible for another 42% of CO2 emissions). Although electric vehicles – both battery electric vehicles (BEVs) and fuel cell electric vehicles (FCEVs) – generate zero tailpipe emissions, there are still emissions from well to wheel, which take into account the emissions from the power source. Battery manufacturing and the battery supply chain are now in focus, so original equipment manufacturers need to pay attention to where and how the battery (and components) are made.

Take the UK, for example, where the annual driving range of 12,000 km consumed 1.7 megawatt hours (MWh) of electricity in 2018 (including over 55% that came from clean energy), which resulted in 380kg of CO2 emissions. This compares with 1.8 tons of CO2 per year for traditional vehicles when using the 119 gram/km emission target for 2017 in Europe and another 7.5 gram/km from oil extraction, refining and delivery. With improvements in the efficiency of the battery supply chain and an incremental power mix that is considerably greener than the existing combination, lifecycle CO2 emissions from electric vehicles will continue to fall. We estimate that there will be an 8–56% reduction in CO2 emissions in battery pack production, making BEVs better than traditional vehicles through the lifecycle in all regions.

Solving the Puzzle

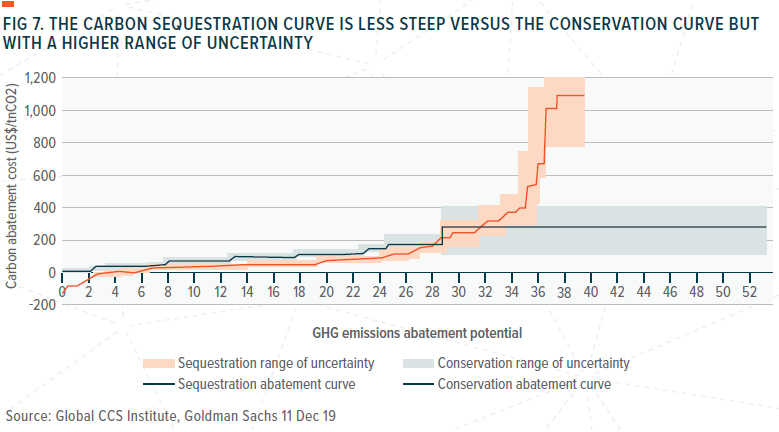

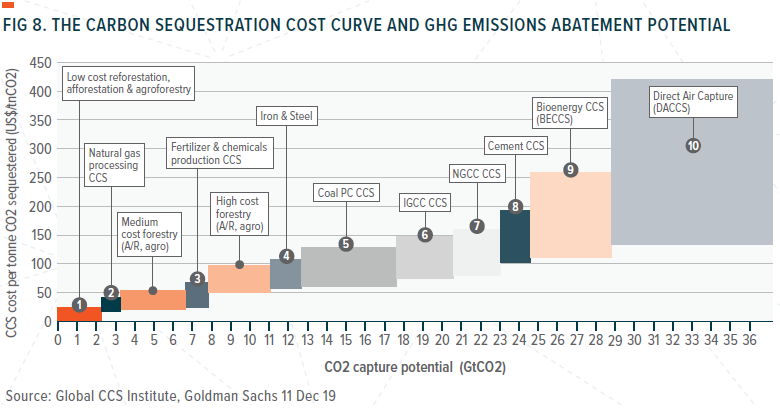

Two complementary paths will enable the world to reach net-zero emissions: conservation and sequestration. Sequestration is critical to solving the climate change puzzle and achieving net-zero carbon emissions. The conservation cost curve has a broader scope for low-cost decarbonization opportunities and a smaller range of uncertainty but steepens exponentially beyond the mid-point. The sequestration cost curve, on the other hand, offers fewer low-cost solutions and is more uncertain, but provides tremendous long-term potential if an economic solution for direct-air carbon capture is developed.

While it is generally accepted that carbon sequestration is vital to achieving net-zero carbon emissions, the rate of carbon sequestration technology deployment remains, to-date, sub-scale. Carbon sequestration efforts can be classified into two main categories; natural sinks (natural carbon reservoirs that can remove carbon dioxide by, for example, reforestation, afforestation and agroforestry), carbon capture, utilisation, and storage technologies (CCUS).

Although carbon sequestration has seen a revival in recent years, it has not yet reached large-scale adoption and the economies of scale that traditionally lead to a breakthrough in cost competitiveness, especially when compared with other CO2-reducing technologies, such as renewables. Despite the vital role sequestration plays in any scenario of net carbon neutrality, investment in carbon capture and storage (CCS) facilities over the past decade has been less than 1% of funds allocated to renewable power. Although we see a definite upswing in CCS pilot plants after this ‘lost decade’, we do not know where costs could settle if CCS attracts the similar economies of scale as solar and wind. Most of the cost of carbon capture and storage comes from the process of sequestration and is inversely related to the CO2 concentration in the air stream from which CO2 is sequestered. The cost curve of CCS, therefore, follows the availability of CO2 streams from industrial processes and reaches its highest cost with direct-air carbon capture and storage (DACCS), where the economics are highly uncertain (most estimates are between USD 40 to USD 400 per ton), and only small pilot plants are currently operating. The importance of DACCS lies in its potential to be almost infinitely scalable and standardized, therefore setting the price of carbon in a net-zero emission scenario.

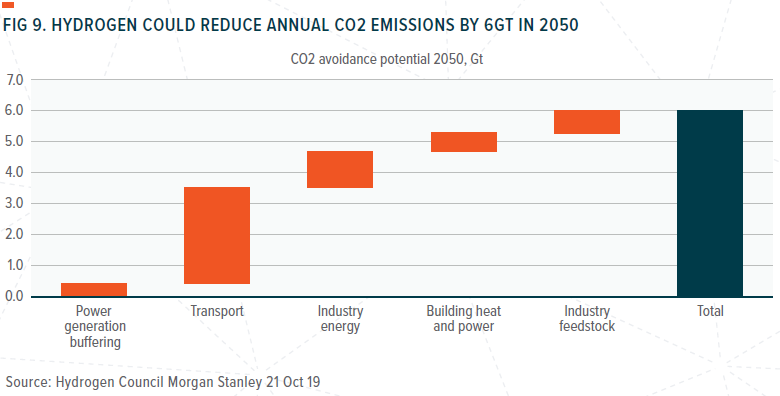

Hydrogen will Play a Key Role

Clean hydrogen is not a commercial technology that contributes to decarbonization. However, it offers a material opportunity to reduce carbon emissions in industrial processes, mobility, and utilities. The Hydrogen Council, an independent industry association, was launched in 2017 by a group of energy, transport and industry companies (including Air Liquide, Alstom, Engie, Daimler, GM, Honda, Shell, Statoil, and Linde) to help hydrogen facilitate the energy transition. The Council’s vision is for hydrogen to account for 18% of final energy demand by 2050, which would imply a tenfold increase in demand (to 550 million tons per year) and the creation of an industry with $2.5 trillion of global revenue (from hydrogen and related equipment).

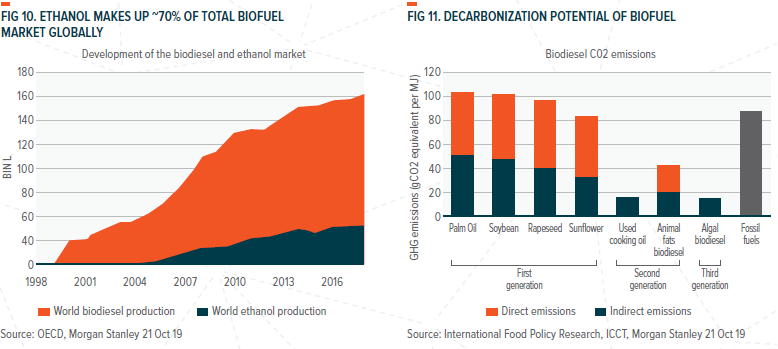

Viable Biofuels

Biofuels currently represent around 3% of global transport fuel demand and provide a low carbon solution for the continued use of the combustion engine. They are made from biomass materials, most commonly in the form of liquid fuels, such as ethanol and biodiesel, and are usually blended with petroleum fuels (gasoline, diesel and jet fuel), but are sometimes used on their own. Biofuels are generally considered both renewable (they depend on renewable feedstock sources) and sustainable (they burn cleaner than fossil fuels). Currently, they are the only viable replacement for petroleum transportation fuels as they can be utilized within legacy internal combustion engines. Biofuels are also technically feasible for use in the aviation and marine markets, but the availability of suitable fuels is still low.