Important Information

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. There is no guarantee of the repayment of the principal. Investors should note:

- Global X Asia Semiconductor ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Semiconductor industry may be affected by particular economic or market events, such as domestic and international competition pressures, rapid obsolescence of products, the economic performance of the customers of semiconductor companies and capital equipment expenditures. These companies rely on significant spending on research and development that may cause the value of securities of all companies within this sector of the market to deteriorate.

- Some Asian securities exchanges (including Mainland China) may have the right to suspend or limit trading in any security traded on the relevant exchange. The government or the regulators may also implement policies that may affect the financial markets. Some Asian markets may have higher entry barrier for investments as identification number or certificate may have to be obtained for securities trading. All these may have a negative impact on the Fund.

- The Fund invests in emerging markets which may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risks, currency risks/control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk, currency devaluation, inflation and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

Why Asia Semiconductor Stocks Are Decoupling from the US Software Crisis?

The Growing Divergence of the US Software and Asia Semiconductor

For years, software and semiconductor stocks were the twin engines of the global tech stock rally, moving in a virtuous cycle. Successful software sales fuelled demand for the hardware needed to run them, while advancements in silicon led to more powerful applications.

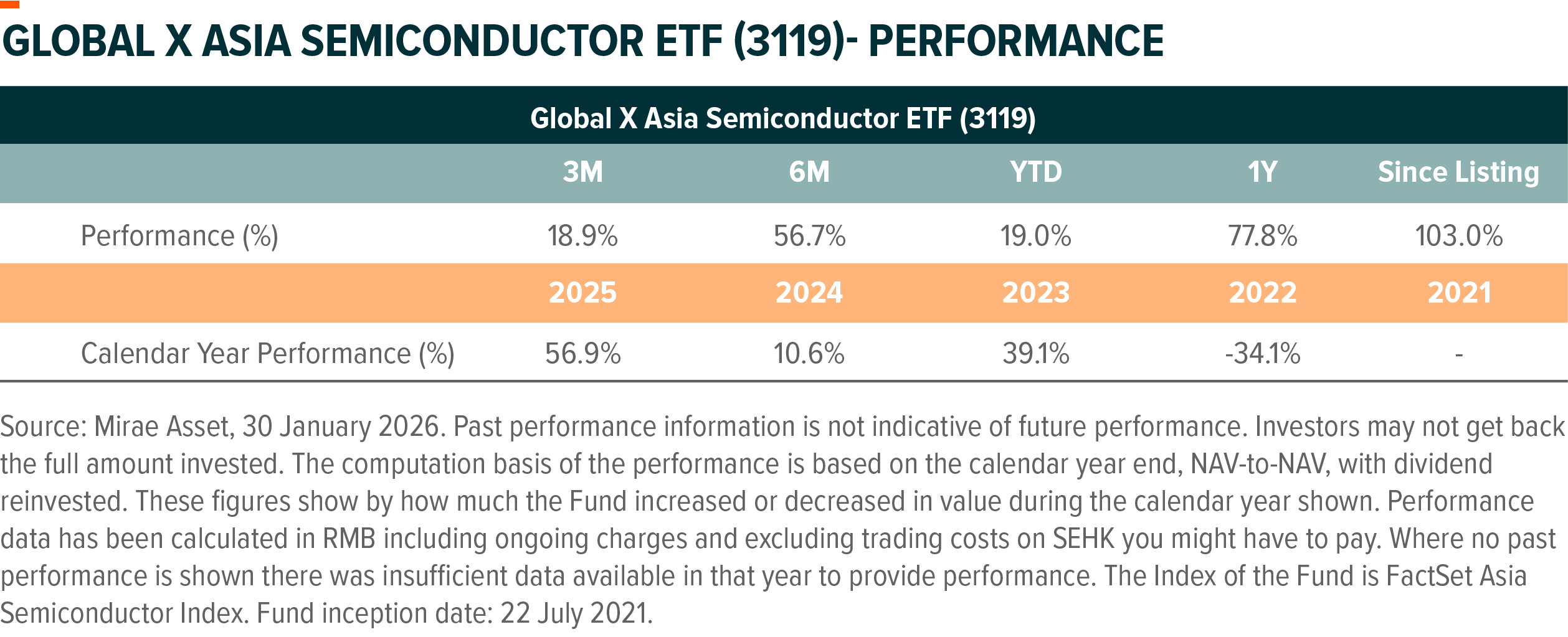

However, as of February 2026, big cracks have emerged in this relationship. While US software indices continue to plummet, Global X Asia Semiconductor ETF (3119) is hitting historic highs. The market is now abandoning the broad “Tech” umbrella, distinguishing between AI’s cost-heavy adopters (Software) and its essential enablers (Asian Semiconductors).

The Software Crisis

The crisis facing the US software market—specifically the SaaS (Software as a Service)— is not a cyclical blip; it is structural.

- Cannibalization by AI Agents: In the past, enterprises paid premium subscriptions for CRM, coding, and accounting tools. Today, autonomous AI models from firms like Anthropic and OpenAI are increasingly performing these functions directly to replace software companies. The need for a fragmented stack of expensive software is likely evaporating.

- Eroding Barriers to Entry: AI has democratized software development, dramatically reducing the “time-to-market.” This is bad for incumbents. New entrants are leveraging AI to offer legacy functionalities at a fraction of the cost, turning yesterday’s monopolies into today’s commodities.

- The Monetization Paradox: Cloud service providers are bearing the brunt of astronomical infrastructure costs to implement AI. However, they lack the pricing power to pass these costs onto customers who are used to fixed subscription fees. They have entered a period of “Margin Squeeze,” where R&D costs are surging while top-line revenue stagnates.

Why Asian Semiconductor stocks are better positioned

While the US software stocks are suffering, the Asian semiconductor stocks are building ever-deeper moats. The investment thesis for the Global X Asia Semiconductor ETF remains robust for three reasons:

- The Irreplaceable Manufacturing Moat: Software can be disrupted by a better algorithm, but a 3nm process fab cannot be replicated with money alone. TSMC’s sub-3nm nodes represent a “deep moat” built on decades of knowhow and hidden knowledge. No matter what AI software wins the war, it cannot reach the world without passing through Asian semiconductor fabs.

- The HBM Bottleneck: AI performance is no longer just about computation; it is about data transfer speed. High Bandwidth Memory (HBM), dominated by Korea’s SK Hynix and Samsung, is the oxygen of the AI accelerator. Paradoxically, the fiercer the competition becomes in software, the higher the demand (and pricing power) for these memory components.

- The Rise of Custom AI chip: Big Tech firms (Google, Amazon, Meta) are aggressively designing custom AI chips to bypass NVIDIA. This is a massive tailwind for Asian foundries. Whether a chip is designed by NVIDIA or by a software giant, the “Silicon Toll” is ultimately paid to Asia for production.

AI Strategy

The current divergence in the tech market marks a shift from digital services to physical necessity. While software applications face fierce competition and shrinking margins, the Asian semiconductor belt remains the sole provider of the hardware that makes AI possible.

By investing in Global X Asian Semiconductor ETF (3119), you are not betting on which software will win, but on the undeniable reality that every winner must use the same essential chips to survive.