Important Information

Investors should not base investment decisions on this website alone. Please refer to the Prospectus for details including the product features and the risk factors. Investment involves risks. There is no guarantee of the repayment of the principal. Investors should note:

- Global X Asia Semiconductor ETF’s (the “Fund’s”) investment in equity securities is subject to general market risks, whose value may fluctuate due to various factors, such as changes in investment sentiment, political and economic conditions and issuer-specific factors.

- Semiconductor industry may be affected by particular economic or market events, such as domestic and international competition pressures, rapid obsolescence of products, the economic performance of the customers of semiconductor companies and capital equipment expenditures. These companies rely on significant spending on research and development that may cause the value of securities of all companies within this sector of the market to deteriorate.

- Some Asian securities exchanges (including Mainland China) may have the right to suspend or limit trading in any security traded on the relevant exchange. The government or the regulators may also implement policies that may affect the financial markets. Some Asian markets may have higher entry barrier for investments as identification number or certificate may have to be obtained for securities trading. All these may have a negative impact on the Fund.

- The Fund invests in emerging markets which may involve increased risks and special considerations not typically associated with investment in more developed markets, such as liquidity risks, currency risks/control, political and economic uncertainties, legal and taxation risks, settlement risks, custody risk, currency devaluation, inflation and the likelihood of a high degree of volatility.

- The trading price of the Fund’s unit (the “Unit”) on the Stock Exchange of Hong Kong is driven by market factors such as demand and supply of the Unit. Therefore, the Units may trade at a substantial premium or discount to the Fund’s net asset value.

- The Fund’s synthetic replication strategy will involve investing up to 50% of its net asset value in financial derivative instruments (“FDIs”), mainly funded total return swap transaction(s) through one or more counterparty(ies). Risks associated with FDIs include counterparty/credit risk, liquidity risk, valuation risk, volatility risk and over-the-counter transaction risk. FDIs are susceptible to price fluctuations and higher volatility, and may have large bid and offer spreads and no active secondary markets. The leverage element/component of an FDI can result in a loss significantly greater than the amount invested in the FDI by the Sub-Fund.

- As part of the securities lending transactions, there is a risk of shortfall of collateral value due to inaccurate pricing of the securities lent or change of value of securities lent. This may cause significant losses to the Fund. The borrower may fail to return the securities in a timely manner or at all. The Fund may suffer from a loss or delay when recovering the securities lent out. This may restrict the Fund’s ability in meeting delivery or payment obligations from realisation requests.

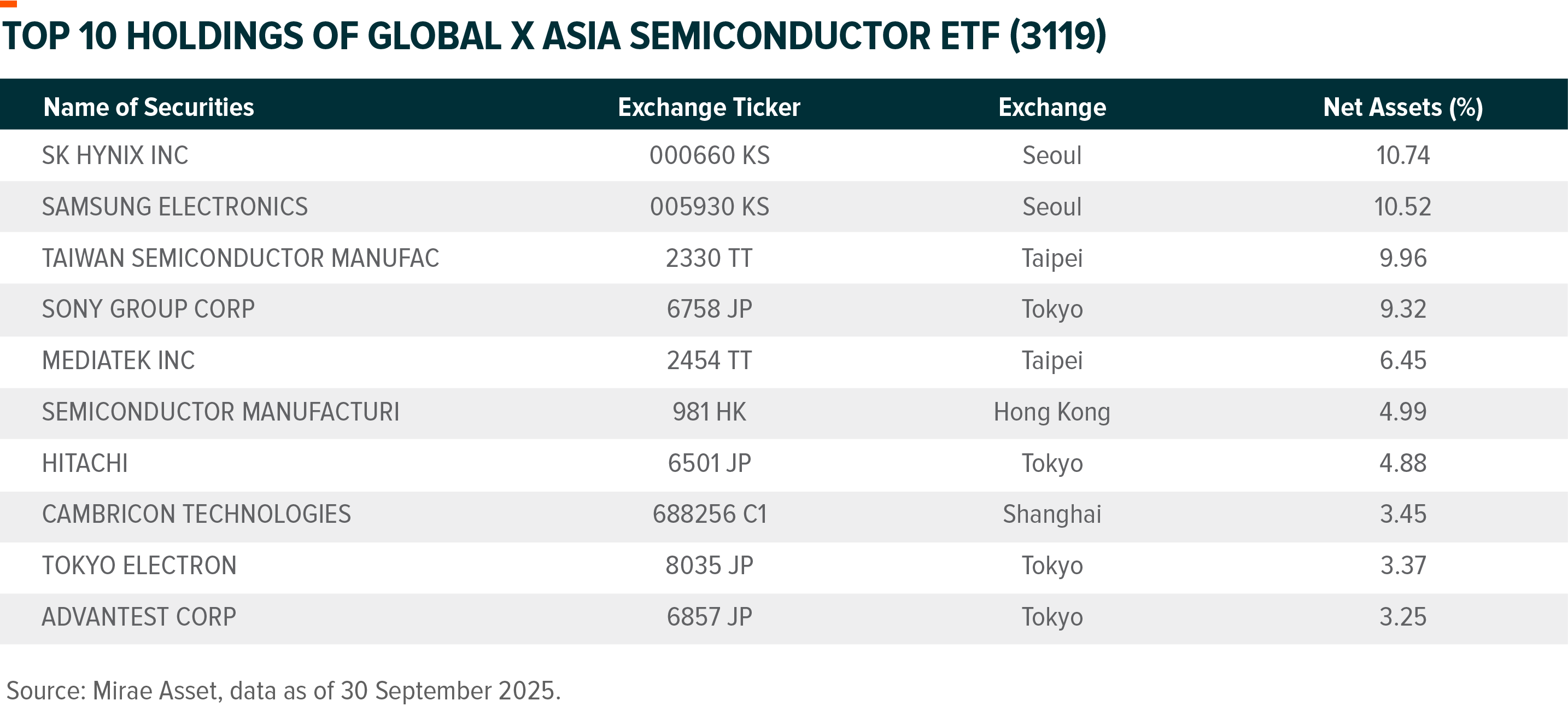

Accessing Top Quality Asian Semiconductor Leaders with 3119

Asian semiconductor stocks have markedly outshined US semiconductor names in 2025, with the FactSet Asia Semiconductor Index soaring by an impressive 39% YTD as of 30 September compared to the Nasdaq 100 Index’s 17% increase and the Philadelphia Semiconductor Sector Index’s 28% climb. (FactSet, Nasdaq, Philadelphia, 30 September 2025)

This performance differential underscores a fundamental market realization: Asia has established itself as the undisputed center of the global semiconductor ecosystem, particularly for AI enabler. The AI boom massive investments in hardware, where Asia demonstrates a marked edge. Industry leaders like TSMC, the backbone of global chip production, and SK Hynix, a key figure in memory supply, are major components of this growth. While US hyperscalers have certainly been key contributors in global AI capex, Asian nations like China have escalated its AI investments, betting on self-reliance to bolster its domestic semiconductor industry.

When looking at the market dynamics, China semiconductor industry has displayed remarkable performance this year driven by growth in domestic AI names such as Cambricon and structural localisation demand. China semiconductor self-sufficiency trend is accelerating and gaining traction. Recent developments have intensified market sentiment on this trend. It started with reports that Nvidia had asked its suppliers to halt H20-related production, followed by DeepSeek’s new V3.1 model optimized for next-gen domestic AI chips, China’s ban on tech firms buying Nvidia’s AI chips, Huawei’s unveiling of an ambitious three-year AI chip roadmap, and SMIC’s testing of a Chinese-developed DUV lithography tool, underscoring the urgency and concerted effort to achieve technological self-reliance. We believe China’s journey toward semiconductor localization is a long-term structural trend.

Meanwhile, Korean semi stocks also rallied year to date driven by a memory super cycle due to capacity shortage as lots of memory supply is occupied by AI level memory upgrading. Korea semiconductor stocks performance is highly correlated to the memory industry, Samsung and SK Hynix are two of the largest memory suppliers globally. First, demand for HBM (high bandwidth memory) used in AI chips is growing at a rapid pace, while the bit density of HBM in next generation AI platforms continue to move higher. HBM chips have larger die size and lower yield per wafer which consumes more wafer i.e. DRAM capacity compared to standard DRAM. This results in tight supply in DRAM supporting DRAM price. Second, top memory makers scheduled to phase out DDR4 rapidly, however many products such as a portion of the smartphone market still relies on DDR4, the demand supply mismatch drove DDR4 price to rally meaningfully YTD. Third, prudent supply strategy in NAND globally combined with demand for eSSD driven by hyperscalers provide support to NAND pricing.

Japanese semiconductor stocks also have delivered steady gains in 2025, supported by resilient demand for equipment and power semiconductors tied to automotive and industrial applications. Semiconductor front end equipment names have been volatile but rebounded recently due to improved outlook in DRAM capacity expansion in 2026. On the other hand, AI related semiconductor equipment name such as Advantest benefits from strong Nvidia orders for testing equipment saw strong YTD performance. (TrendForce, Mirae Asset, 1 October 2025)